High Oil Prices, Inflationary Pulses, and the Risk of Transatlantic Policy Scissors

YCC Perspective: At YCC Capital, our global macro value lens prioritizes capital-flow dynamics and gaps between prevailing narratives and underlying realities. The protracted US-Iran stalemate and depressed shipping volumes through the Strait of Hormuz constitute a textbook geopolitical supply shock. Its transmission into global inflation, central bank policy paths, and cross-asset pricing is asymmetric across economies—particularly relevant for our positioning in Asia and RMB assets, where energy import diversification provides relative insulation compared with more vulnerable regional peers. This analysis dissects the inflationary impulse, the probability of a Fed-ECB policy scissors, and the resulting implications for bonds, equities, and currencies.

Key Takeways

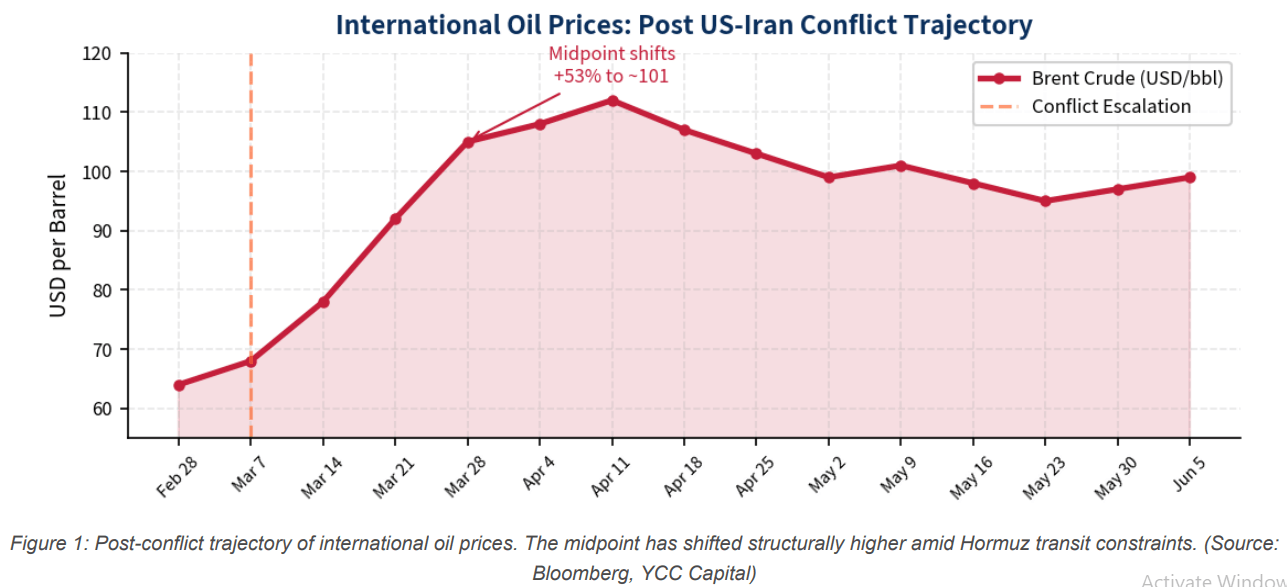

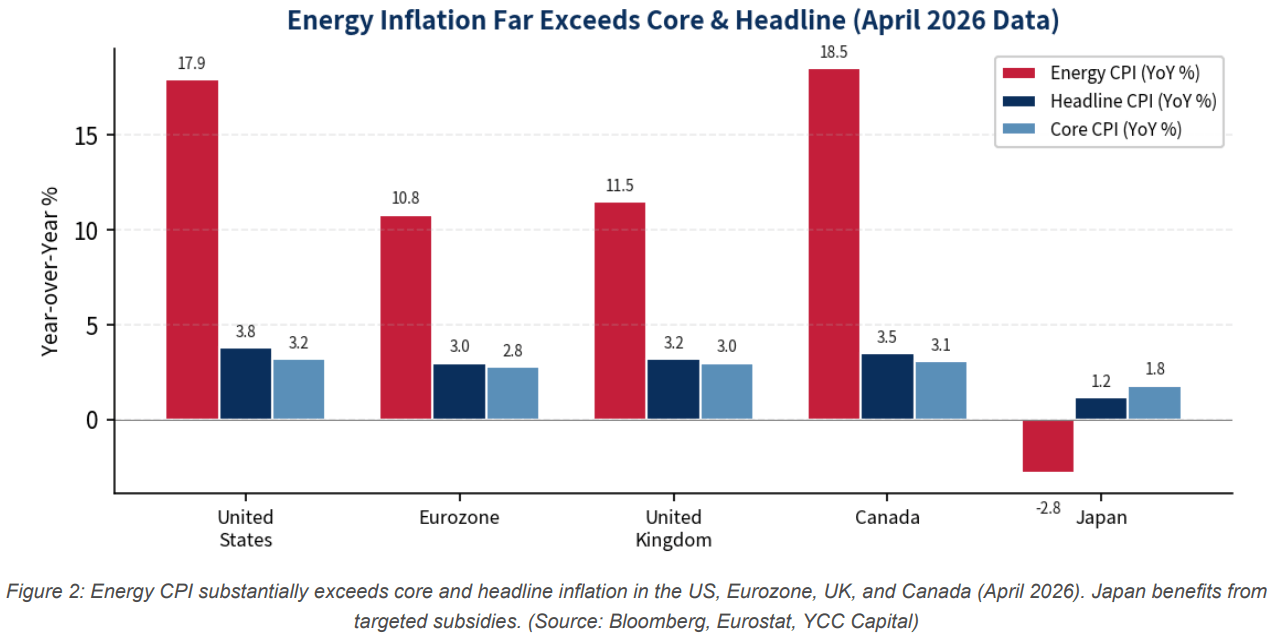

- High oil prices have elevated inflation across multiple economies. The US-Iran conflict has remained locked in a three-month stalemate as of early June. Hormuz Strait daily transit volumes have collapsed to single digits—approximately 5% of pre-conflict levels—with no meaningful recovery. Brent and WTI midpoints have shifted from ~66 USD to ~101 USD (+53%). Energy CPI now exceeds both core and headline inflation in the US (17.9%), Canada (~18%), Eurozone (10.8%), and UK, confirming a potent imported inflation pulse. Japan remains an outlier due to targeted energy subsidies.

- Energy inflation is likely to create a policy scissors between the Fed and ECB. Eurozone inflation pressures feel more binding: single mandate, higher energy dependence (non-exporter status), and inflation expectations that have spiked to 2022 highs. US dual mandate and resilient domestic energy production afford the Fed greater flexibility. Market pricing implies <1% probability of a June Fed hike versus >90% for an ECB hike. Should the ECB move first, the resulting narrowing of the USD-EUR rate differential would provide tactical support to the euro and cap the DXY.

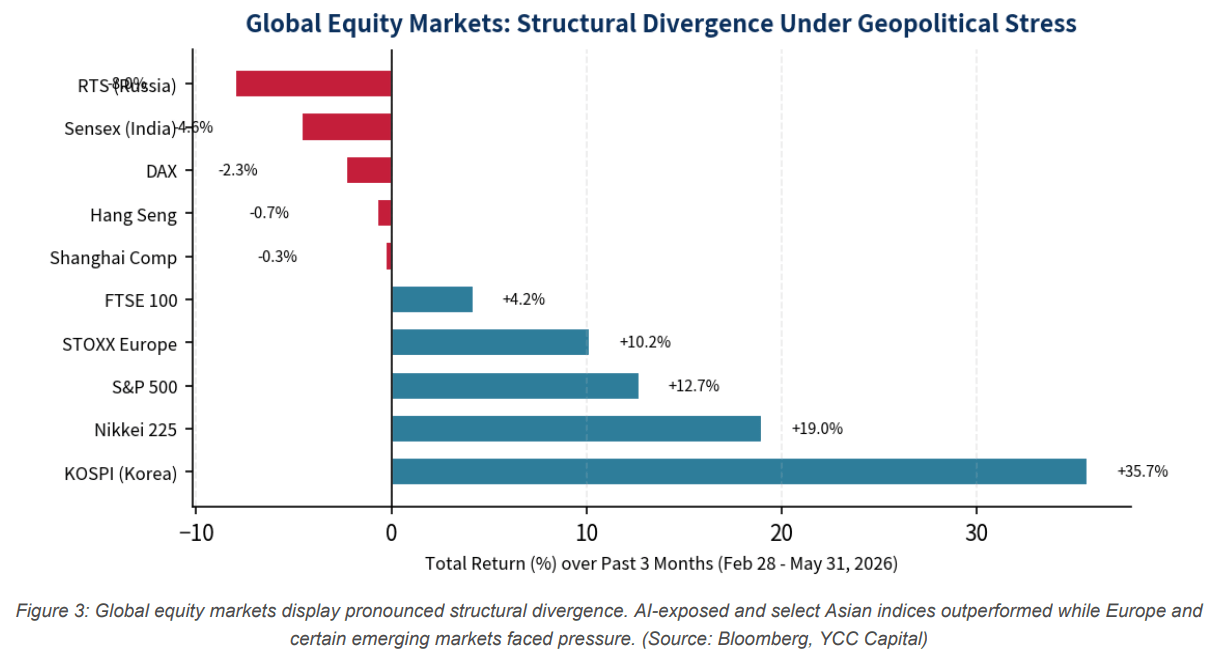

- Bond markets face more persistent pressure than equities; FX shows RMB resilience. Over the past three months, global bonds adjusted broadly higher in yield as rate-cut expectations were pared back. Equities exhibited clear bifurcation: Europe and energy-vulnerable markets underperformed while AI-exposed US indices and select Asian markets (e.g., Korea) proved more resilient. Looking forward, we expect the 10Y UST yield midpoint to grind higher. On FX, RMB has appreciated against the USD while JPY, CHF, and EUR depreciated—supported by China’s diversified energy sourcing and export outperformance amid regional supply-chain stress. A policy scissors would likely keep the USD in a wide trading range with mild RMB appreciation bias persisting.

- Risk factors remain elevated. Further escalation in the Middle East, an oil price spike beyond current levels, or an unexpectedly hawkish Fed reaction function could materially alter the base case.

Sources: Bloomberg, YCC Capital analysis. Data as of early June 2026 unless otherwise noted.

High Oil Prices Have Elevated Inflation Across Multiple Economies

The US-Iran conflict, which erupted earlier this year and entered a protracted stalemate by early June, has now persisted for approximately three months without a durable de-escalation agreement. Throughout this period, maritime transit volumes through the Strait of Hormuz—the critical chokepoint for roughly 20% of global oil trade—have remained severely depressed. Average daily transits have fallen into the single digits, representing roughly 5% of pre-conflict throughput. There are no clear signs of normalization.

Constrained supply has kept international crude prices elevated and structurally higher than the pre-conflict equilibrium of approximately 66 USD per barrel. The post-conflict midpoint has shifted to around 101 USD—a 53% increase. This

sustained deviation is transmitting directly into global inflation via higher energy input costs, creating a classic imported

inflation shock.

Energy Inflation Transmission: Cross-Country Evidence

In the three months since the conflict intensified, energy CPI has materially outpaced both core and headline measures in most major economies (April 2026 data). The United States recorded energy inflation of 17.9% against headline CPI of 3.8%. Canada saw similar extremes in the 17–20% range. The Eurozone and broader Europe registered energy inflation between 10% and 15%, well above their respective core and headline prints. The United Kingdom followed a comparable pattern.

Japan stands apart: its energy CPI remains in negative territory, though the pace of deflation has narrowed meaningfully versus the pre-conflict baseline. This divergence largely reflects Japan’s aggressive fiscal response—most notably the 3.11 trillion JPY supplemental budget that established a dedicated Middle East emergency energy reserve to cushion domestic price pass-through. Without such buffers, the inflationary impulse would likely have been more uniform globally.

The key takeaway is that a geopolitically induced oil price regime shift—rather than a transitory spike—has already embedded a durable inflationary pulse into multiple large economies. This is not merely a headline effect; it is feeding into core inflation expectations and, critically, into central bank reaction functions. Markets are now pricing higher-for-longer policy rates in several jurisdictions, with the Euro area appearing particularly sensitive.

Energy Inflation and the Emerging US-Europe Policy Scissors

Negotiations between the US and Iran have continued in fits and starts. While markets briefly priced in the possibility of an extended ceasefire or de-escalation framework in late May, renewed mutual strikes quickly dispelled that optimism. Key uncertainties persist around any potential extension of the current pause, restoration of Hormuz transit, and the stance of Israel. June’s cluster of global central bank meetings will therefore occur against a highly fluid geopolitical backdrop, with oil prices and negotiation outcomes remaining live variables.

Relative to the United States, the European Central Bank faces a more acute inflation challenge. April data showed Eurozone energy inflation at 10.8% and headline CPI at 3.0%—already above the 2% target. US comparables were 17.9% energy and 3.8% headline. While the numerical gaps are not enormous, three structural factors tilt the balance toward greater ECB urgency:

- Energy dependence asymmetry: The United States is a net oil exporter with substantial domestic production flexibility. The Eurozone remains a large net importer with limited short-term substitution options.

- Inflation expectation dynamics: Eurozone long-term inflation expectations have surged to levels last seen during the 2022 energy crisis peak. US expectations, by contrast, have remained more contained—even below the levels observed during the 2025 tariff-related inflation scare.

- Institutional mandate differences: The ECB operates under a single, hard inflation target. The Federal Reserve balances inflation with maximum employment. When confronting a binding inflation constraint, the ECB’s reaction function exhibits greater rigidity and less tolerance for overshoots.

Market-implied probabilities reinforce this asymmetry. FedWatch currently assigns less than a 1% chance of a June rate hike by the Federal Reserve. ECBWatch places the probability of an ECB hike above 90%. Our base case therefore anticipates a June pause from the Fed and a hike from the ECB—setting the stage for a policy scissors.

Historically, across multiple policy cycles since 1990, the Federal Reserve has almost invariably led the ECB in major turning points—whether shifting from hiking to easing or vice versa. This leadership reflects both the US economy’s cyclical lead and the exchange-rate feedback loop: an overly dovish ECB relative to the Fed risks euro depreciation pressure. A reversal of this historical pattern in June—ECB hiking while the Fed holds—would constitute a genuine policy scissors. Mechanically, it narrows the interest-rate differential that has favored the USD, offering tactical support to the euro and placing downward pressure on the broad dollar index.

Impacts on Equities, Bonds, and Currencies Under Geopolitical Repetition

Bond Markets: More Persistent Adjustment Than Equities

Bond pricing is anchored directly to inflation and monetary policy expectations. The oil-driven inflation pulse and the associated withdrawal of rate-cut pricing have driven yields higher across major markets over the past three months. US Treasuries have seen the entire curve shift upward, with both 2-year and 10-year yields rising. Similar yield increases have occurred in JGBs, Gilts, and Bunds. Because the underlying drivers—elevated oil, sticky inflation expectations, and policy uncertainty—are likely to persist even if Hormuz transit partially recovers, we expect bond market pressure to remain more durable than the equity market response.

Equities: Clear Structural Divergence

Equity markets have not moved in lockstep. Over the February 28–May 31 window, performance has bifurcated sharply. Markets most directly exposed to European energy costs and geopolitical proximity (certain European indices) have lagged. In contrast, US indices—particularly those benefiting from AI-driven growth narratives—have demonstrated resilience, with the growth premium partially offsetting the macro headwinds. Select Asian markets have also shown strength, underscoring that not all risk assets respond uniformly to energy shocks when offset by domestic or thematic tailwinds.

Foreign Exchange: RMB Resilience Amid Broad Dollar Strength

In the same period, the dollar index strengthened as JPY, CHF, and EUR all depreciated meaningfully against the USD. The RMB, however, appreciated against the dollar on a net basis. Two primary factors underpin this outperformance. First, China’s energy import basket is far more diversified than that of many Asian peers heavily reliant on Middle East crude; the negative terms-of-trade shock is therefore attenuated. Second, China’s export growth has repeatedly surprised to the upside even as regional supply chains in other Asian economies have been stressed by energy costs—providing additional support to the currency.

Looking ahead, the potential emergence of a US-Europe policy scissors introduces additional two-way volatility for the dollar. We expect the USD to trade in a wide range rather than a one-directional trend. For the RMB, the combination of relative energy resilience, export momentum, and a narrowing (or at least less widening) rate differential versus the euro should sustain a mild appreciation bias, though punctuated by geopolitical headline risk.

10Y UST Yield Midpoint Likely to Rise Further

Even if Hormuz transit volumes recover modestly, the structural supply gap and elevated price midpoint are unlikely to reverse quickly. Inflation concerns will therefore linger. At the same time, the Federal Reserve faces a genuine policy dilemma: higher inflation midpoints colliding with still-resilient US growth. Internal hawkish commentary has already surfaced, and markets are beginning to price the possibility of future hikes rather than cuts. Both factors exert upward pressure on longer-dated yields. We therefore expect the 10Y UST yield midpoint to continue drifting higher over the coming quarters, with episodic volatility around geopolitical headlines.

YCC Strategic View: Positioning in an Asymmetric Shock Environment

From YCC Capital’s vantage point, this episode reinforces several core tenets of our concentrated global macro value approach. First, geopolitical supply shocks are inherently asymmetric: they penalize energy-intensive, import-dependent economies more severely while creating relative winners among diversified importers or net exporters. China’s position in the latter category—bolstered by diversified sourcing and export competitiveness—helps explain RMB resilience and suggests that broad “risk-off China” narratives may overgeneralize in the current setting.

Second, policy scissors episodes historically create tactical opportunities in FX and rates. A materialization of ECB hiking ahead of the Fed would favor EUR/USD upside and could support selective European duration or equity exposure on a tactical basis—though we remain mindful of Europe’s deeper structural growth challenges. Conversely, any hawkish Fed

surprise would reinforce USD strength and pressure risk assets globally.

Third, and most importantly for our mandate, these global cross-currents do not alter the dominant structural drivers we monitor for China and broader Asia: demographic headwinds, property sector overhang, capital allocation distortions, and the long-term trajectory of productivity and return on capital. Our asymmetric hedging framework continues to emphasize downside protection against these China-specific risks while selectively harvesting global opportunities where narrative-reality gaps are widest.

Investors should treat Hormuz developments and central bank divergence signals as swing factors for near-term risk sentiment and commodity-linked exposures, but should avoid allowing them to overshadow the higher-conviction, longer-horizon structural themes that define our strategy.

Risk Factors

Geopolitical escalation in the Middle East beyond current levels; oil prices rising materially above the current elevated midpoint; an unexpectedly hawkish Federal Reserve reaction function that tightens financial conditions faster than anticipated; faster-than-expected recovery in Hormuz transit volumes that reverses the inflationary impulse; or secondary sanctions/regulatory responses that further fragment global energy trade.

Editorial Board

Ken Cao, Chief Strategist, Global Investment Strategy

Founder, Portfolio Manager & Chief Investment Officer, YCC Capital Management

Akiko Ikezawa, Managing Analyst

Focus: Japan macro, monetary policy transmission, and Asia capital flows

Yui Nabeshima, Strategist

Focus: FX, rates, and cross-asset implications of geopolitical shocks

Mai Ikeda, Research Analyst

Focus: China policy analysis, energy markets, and inflation dynamics

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results. YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected. Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. This report is intended solely for qualified investors and institutional clients who possess the knowledge and experience to evaluate the risks involved. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents. This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.

Contact Us

For questions, subscription inquiries, or to receive our free daily market insight newsletter, please contact ir@yccinvest.com or visit www.yccinvest.com. We welcome feedback from sophisticated investors and family offices aligned with our long-term, truth-seeking approach to global capital allocation. YCC Capital Research — Understanding the Universe, One Capital Flow at a Time.

YCC Capital Research — Understanding the Universe, One Capital Flow at a Time.