Implications for Household Portfolio Rebalancing, JGB Market Stability, and Yen Dynamics in Japan’s Asset Management Nation Initiative.

YCC Perspective

At YCC Capital, our global macro value lens prioritizes capital-flow dynamics and gaps between prevailing policy narratives and underlying household realities. Japan’s ‘Asset Management Nation’ push and the expanded NISA framework have catalyzed a notable shift from savings to investment. Yet this transition has manifested asymmetrically: record flows into overseas equity funds and global ‘all-country’ products have amplified capital outflows and contributed to JPY pressure, even as domestic rates begin a long-awaited normalization. In this context, renewed attention on personal JGBs—retail-targeted, principal-protected Japanese government bonds—represents a pragmatic policy response aimed at diversifying household choices, anchoring a more resilient domestic investor base for JGBs amid elevated foreign participation metrics, and offering a low-volatility JPY ballast within increasingly globally exposed portfolios. This analysis examines the drivers behind the current discussion, the structural features of personal JGBs, potential design enhancements, and the broader implications for Japan’s macro-financial stability from our cross-border capital allocation perspective.

Key Takeways

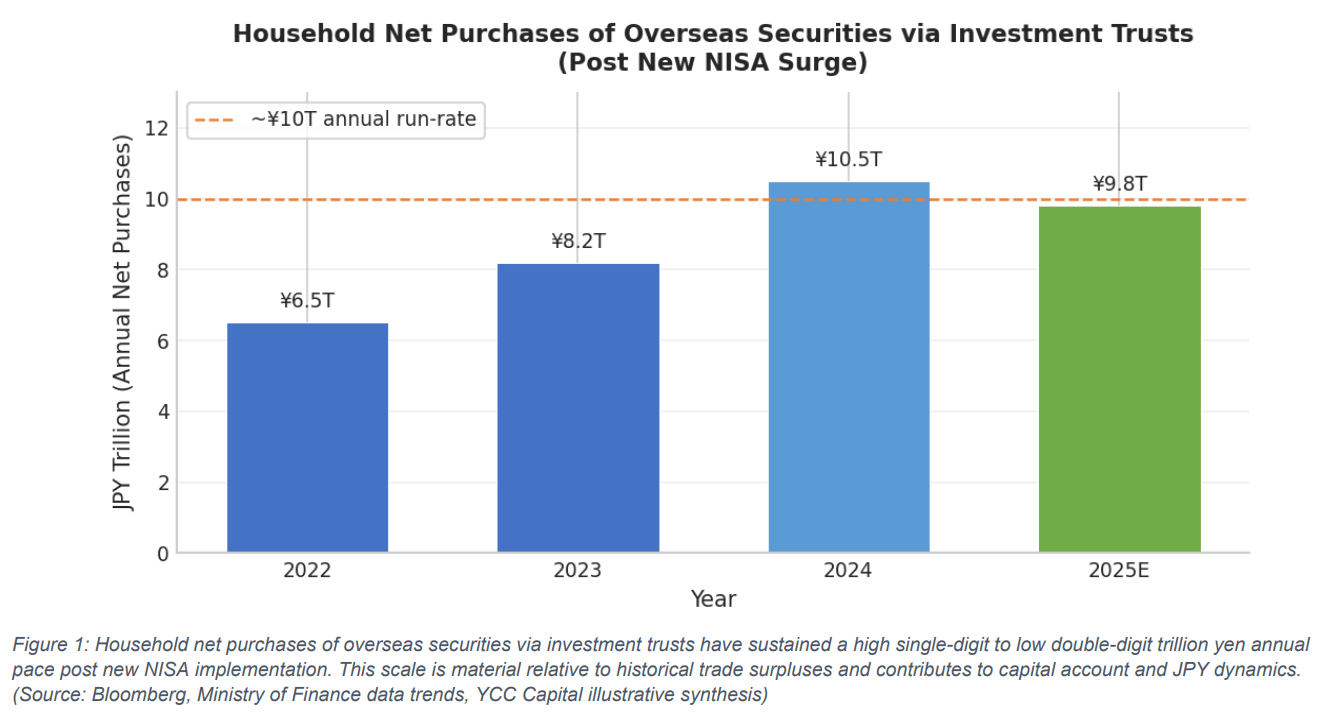

- Elevated foreign ownership of JGBs (certain measures now exceeding prior domestic-centric thresholds) and sustained household purchases of overseas securities via investment trusts—running at approximately ¥10 trillion annually since the new NISA launch—have intensified policy focus on expanding stable domestic holding layers, especially among households, to reduce concentration and outflow risks.

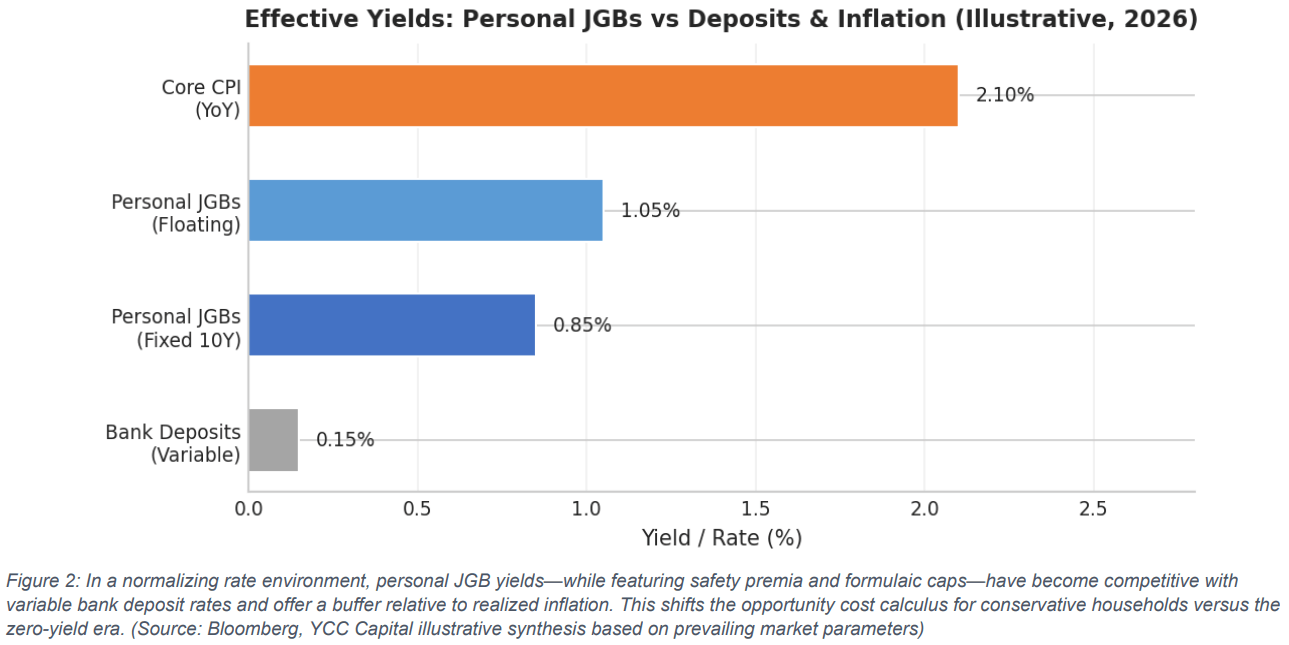

- Personal JGBs feature built-in principal guarantees and yields that have turned competitive following the exit from zero/negative rates, providing households with a simple, government-backed domestic fixed-income option that was structurally unappealing during the deflationary decades but now offers meaningful ballast versus bank deposits or concentrated global equity bets.

- The post-NISA surge in global equity and ‘all-country’ fund allocations has added a material layer to Japan’s capital account outflows and JPY softness; thoughtfully designed domestic alternatives can partially rebalance these flows without restricting investor freedom, supporting more stable two-way capital dynamics.

- Ongoing deliberations—including potential yield adjustments to better compete with tax-advantaged equity upside, careful consideration of NISA eligibility (complicated by the product’s principal-protection nature), and ancillary features such as inheritance planning—signal constructive product evolution while preserving the core attributes of safety, simplicity, and broad accessibility.

- From YCC’s vantage point, revitalized personal JGBs can function as an effective portfolio diversifier and ‘balancer’ alongside global growth assets. This supports household financial resilience, dampens tail risks from over-concentration in equities or foreign currency exposure, and aligns with long-term compounding in a normalizing Japanese interest rate regime—without displacing higher-conviction international opportunities where narrative-reality gaps remain wide.

The Evolving JGB Holder Base and the Policy Push for Domestic Stability

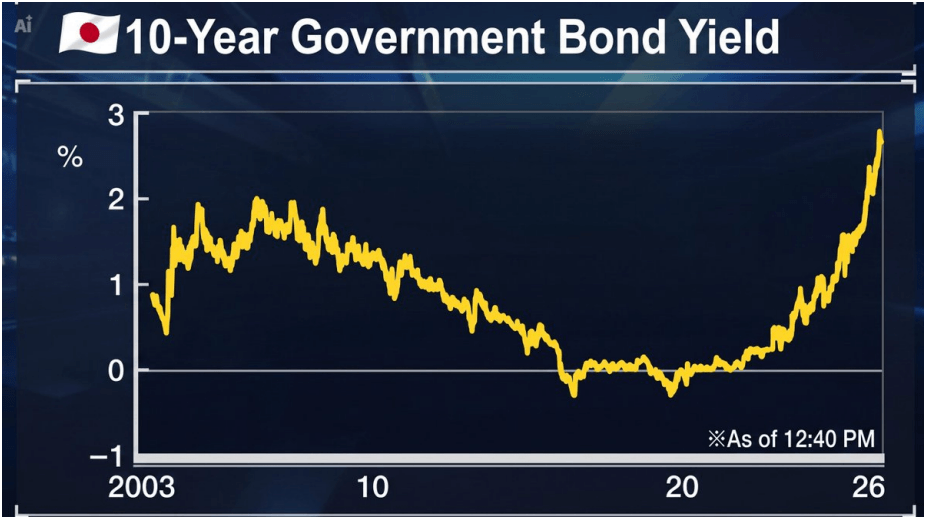

Japan’s JGB market has long benefited from a deep domestic investor base, historically dominated by banks, the Bank of Japan, and households. However, foreign participation has risen meaningfully over the past decade-plus, with certain visibility-adjusted or net metrics now reflecting elevated offshore holdings. While this globalization of the investor base brings liquidity benefits, it also introduces greater potential for volatility in response to global risk sentiment, interest rate differentials, and currency moves. Against this backdrop, recent policy discussions—spanning the Asset Management Nation Parliamentary League and public comments from figures such as Finance Minister Katayama—have emphasized the desirability of a broader, more stable domestic holding layer.

Households represent one of the more promising areas for incremental absorption. Unlike institutional players with strict mandates or mark-to-market sensitivities, retail investors can provide sticky, long-term demand when products are appropriately designed and communicated. The policy intuition is straightforward: if a larger share of Japan’s substantial household financial assets can be channeled into domestically issued, yen-denominated instruments with attractive risk-return profiles, the JGB market gains a more resilient core, reducing reliance on potentially flighty foreign flows during stress episodes.

This is not framed as a rejection of international capital or a ‘closed market’ impulse. Rather, it reflects a recognition that diversified holder composition—domestic retail alongside foreign institutions and domestic banks—enhances overall market stability. The discussion is therefore constructive and market-oriented: how to make personal JGBs a more compelling choice within a competitive menu of options available to Japanese savers and investors.

Household Overseas Investment Surge and Macro Implications

Parallel to the JGB holder discussion has been the well-documented acceleration of household capital outflows via investment trusts. Following the 2024 expansion of NISA (Nippon Individual Savings Account) tax-advantaged frameworks, annual net purchases of overseas securities through such vehicles have settled into a roughly ¥9.5–11 trillion run-rate. Products such as global all-country equity funds and S&P; 500 trackers have captured the lion’s share of these flows.

While multiple factors influence the JPY—including corporate hedging behavior, trade balances, and global USD strength—the household channel is no longer negligible. In years when the current account surplus was itself only in the low-20 trillion yen range, sustained double-digit trillion yen outflows via retail investment vehicles represent a meaningful swing factor. This does not imply that overseas investment should be curtailed; on the contrary, greater international diversification is healthy for Japanese households long starved of yield. However, the asymmetry—strong one-way flows into global equities with limited counterbalancing domestic fixed-income uptake—creates excess pressure on the currency and complicates the BOJ’s normalization path.

A natural policy and market response is therefore to ensure that the domestic menu includes compelling, easy-to-understand options that can attract a portion of these flows on their own merits. Personal JGBs, if properly positioned and modestly enhanced, can play exactly this ‘balancer’ role without requiring any investor to forgo global opportunities.

Design Features of Personal JGBs: Why They Merit Fresh Consideration

Personal JGBs have existed for years but suffered from chronically low uptake during the zero- and negative-rate era. Their core architecture, however, is well-suited to the current environment:

Principal Protection: After a minimum holding period (typically one year for certain series), the government stands ready to repurchase at par, providing a hard floor that bank deposits and equity funds lack. Modest penalties or opportunity costs may apply for early exit, but the downside is capped in nominal terms.

Yield Mechanics: Fixed-rate variants offer predictable coupons. Floating-rate versions are periodically reset (often semi-annually) based on market yields with a formula that includes a multiplier (historically around 0.66x) reflecting an embedded option cost. Importantly, there is a floor; rates will not go negative even if market yields briefly dip. This provides asymmetric upside in a rising-rate world while protecting against the deflationary trap that prevailed for three decades.

Simplicity and Accessibility: Minimum denominations are retail-friendly, purchase channels include banks and post offices, and the product is explicitly designed with individual investors in mind—avoiding the complexity of auction bidding or large-lot settlement that institutional JGBs entail.

The historical lack of uptake was therefore not a design flaw but a reflection of the macroeconomic regime: when risk-free rates were zero or negative and inflation expectations anchored near zero, the marginal investor rationally preferred the liquidity of bank deposits. As Japan transitions toward a world of positive real and nominal rates, that calculus changes. Personal JGBs now offer a genuine alternative that combines nominal safety with non-zero yield—attributes that were absent for a generation.

Policy Options and Product Evolution Under Discussion

Recent commentary has floated several avenues for increasing the appeal of personal JGBs without compromising their foundational safety:

Yield Enhancement: Modest upward adjustments to the formula or spread could better position the product against the upside available in tax-advantaged equity products. References to ‘20%’ in policy discourse likely allude to aligning with NISA contribution limits or framing competitive total returns rather than a literal 20% coupon—recognizing that excessive yield chasing could undermine the low-risk character that defines the instrument’s value proposition.

Tax Treatment and NISA Interaction: Including principal-protected products within NISA raises conceptual questions because NISA is explicitly a framework for supplying risk capital. While technically feasible via legislative adjustment, many view it as inconsistent with the program’s intent. A more pragmatic path may lie in ensuring that personal JGB interest is taxed at favorable rates or that holding incentives (e.g., via tax-advantaged accounts outside NISA) are clarified.

Ancillary Benefits (Inheritance & Planning): Features that facilitate smooth intergenerational transfer or integrate with retirement/inheritance planning could broaden appeal among Japan’s aging population. However, layering too many policy objectives risks complicating the product’s simplicity and raising fairness concerns; targeted, transparent enhancements are preferable to omnibus redesigns.

Crucially, the overarching communication frame should emphasize choice expansion and portfolio diversification rather than any implicit discouragement of overseas investment. Japanese households benefit from global exposure; the goal is to ensure they also have access to high-quality domestic instruments so that allocation decisions reflect genuine risk-return preferences rather than a binary between ‘deposits or foreign equities.’

YCC Strategic View: Implications for Macro Stability and Portfolio Construction

This policy moment reinforces several tenets of our concentrated global macro value approach. First, capital flow asymmetries matter: Japan’s household sector has accumulated enormous financial assets, yet the post-NISA reallocation has been heavily one-directional toward overseas risk assets. A successful revitalization of personal JGB demand would introduce a counter-flow that dampens JPY volatility and provides the BOJ with greater room to normalize policy without excessive financial conditions tightening via the exchange rate.

Second, product design and narrative framing are powerful. The zero-rate regime created a generation of households for whom ‘JGBs equal no yield.’ Reintroducing these instruments in a positive-rate world, with clear communication around principal protection and competitive positioning versus deposits, can unlock latent demand. This is not about financial repression or forcing domestic holdings; it is about correcting an information and choice asymmetry that persisted for too long.

Third, for investors and advisors constructing Japanese or JPY-exposed portfolios, personal JGBs (or funds holding them) can serve as a core defensive sleeve—particularly valuable for older households, conservative mandates, or as a complement to higher-beta global equity and alternative exposures. In our own framework, we view such instruments as part of the ‘safe’ allocation within multi-asset mandates, allowing greater conviction deployment elsewhere where mispricings are more pronounced.

Investors should monitor uptake statistics, any announced design changes, and BOJ communication around collateral and yield curve control adjustments as leading indicators of whether this policy impulse translates into durable demand shifts. In the meantime, the structural themes we track for Japan—demographics, productivity trends, fiscal trajectory, and corporate governance evolution—remain the dominant drivers of long-term capital allocation outcomes. Enhanced personal JGBs are a helpful tactical and structural stabilizer, not a substitute for addressing those deeper dynamics.

Risk Factors

- Slower-than-expected household uptake if perceived real yields remain insufficient relative to inflation or equity upside narratives persist unchallenged.

- Unintended market signaling if aggressive yield or tax tweaks are interpreted as fiscal distress rather than product optimization.

- Over-complication of product features that erodes the simplicity and trust that are central to retail adoption.

- External shocks (global risk-off, rapid USD strength, or commodity spikes) that overwhelm domestic allocation preferences and re-trigger one-way outflows.

- Policy inconsistency or frequent rule changes that undermine long-term investor confidence in the instrument class.

Sources: Bloomberg, Ministry of Finance Japan, Bank of Japan, YCC Capital analysis and synthesis. Data and market conditions as of early June 2026 unless otherwise noted.

Editorial Board

Ken Cao, Chief Strategist, Global Investment Strategy

Founder, Portfolio Manager & Chief Investment Officer, YCC Capital Management

Akiko Ikezawa, Managing Analyst

Focus: Japan macro, monetary policy transmission, and Asia capital flows

Yui Nabeshima, Strategist

Focus: FX, rates, and cross-asset implications of geopolitical shocks

Mai Ikeda, Research Analyst

Focus: China policy analysis, energy markets, and inflation dynamics

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. This report is intended solely for qualified investors and institutional clients who possess the knowledge and experience to evaluate the risks involved. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.

Contact Us

For questions, subscription inquiries, or to receive our free daily market insight newsletter, please contact ir@yccinvest.com or visit www.yccinvest.com. We welcome feedback from sophisticated investors and family offices aligned with our long-term, truth-seeking approach to global capital allocation.