YCC CAPITAL

Global Strategy

June 21, 2026

Executive Perspective

International monetary systems rarely change overnight. They evolve gradually, often appearing stable until a series of political, economic, and geopolitical pressures suddenly expose deeper structural weaknesses.

The post-1971 international monetary order—commonly known as the Jamaica System—has survived for more than half a century. It has enabled globalization, supported unprecedented growth in international trade, and provided the world with a common reserve and settlement currency centered around the U.S. dollar. Yet the same system has also generated persistent global imbalances, concentrated extraordinary privileges in the United States, and increasingly raised questions about long-term sustainability.

Recent developments have accelerated this debate. Rising geopolitical fragmentation, sanctions, trade conflicts, reserve diversification, and unusually strong demand for gold all suggest that global confidence in the existing system is no longer as unquestioned as it once was.

At YCC Capital, we believe the critical question is not whether the dollar disappears. It will not. The more important question is whether the international monetary architecture gradually evolves toward a more diversified framework in which the dollar remains important but no longer occupies the singular position it has held since the collapse of Bretton Woods.

The answer carries profound implications for investors, policymakers, and corporations worldwide.

The Existing System: Powerful but Increasingly Strained

The international monetary system governs how countries settle trade, move capital, manage reserves, and coordinate financial relations.

Since the collapse of Bretton Woods in 1971 and the formal establishment of the Jamaica System in 1976, the world has operated under a fiat currency framework. Unlike previous eras, currencies are no longer backed by gold or any physical commodity. Their value rests primarily on confidence, institutional credibility, and macroeconomic management.

This framework has several defining characteristics:

1. Fiat Money Dominates

Modern currencies derive value not from gold convertibility but from public confidence and sovereign authority.

The United States, Europe, Japan, China, and virtually every major economy now operate under fiat systems. Monetary authorities possess significant flexibility in managing liquidity, interest rates, and economic cycles.

2. Unlimited Nominal Currency Creation

Once currencies were detached from gold, governments gained the ability to create money unconstrained by physical reserves.

This flexibility has allowed policymakers to respond aggressively to crises ranging from the 2008 Global Financial Crisis to the pandemic-era economic shock.

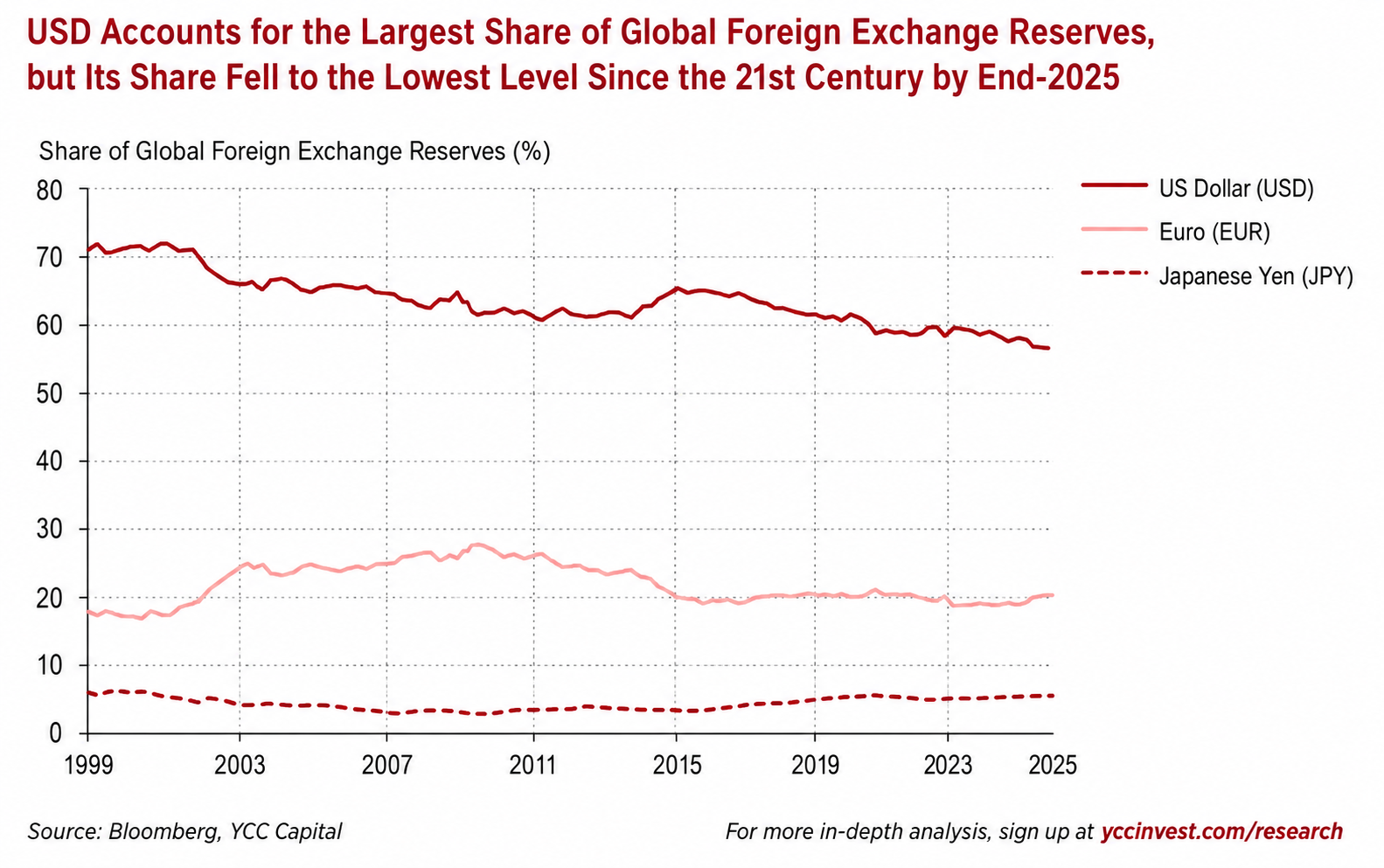

3. Dollar Centrality

Despite decades of predictions regarding its decline, the dollar remains the dominant reserve asset, settlement currency, and global funding vehicle.

The depth of U.S. financial markets, the liquidity of Treasury securities, and the network effects embedded in global commerce continue to reinforce dollar dominance.

4. Flexible Exchange Rates

Most major economies now allow exchange rates to fluctuate, providing an important shock absorber that was unavailable under fixed exchange-rate regimes.

The Structural Problems of Dollar Dominance

The current system has delivered enormous benefits. Yet its weaknesses have become increasingly visible.

Persistent Global Imbalances

One of the most significant flaws is the persistence of large and durable trade imbalances.

For decades, the United States has functioned as the world’s primary deficit country while export-oriented economies—including parts of East Asia and major commodity exporters—have generated sustained surpluses.

This arrangement has enabled globalization but has also created structural distortions that never fully self-correct.

The Dollar’s “Exorbitant Privilege”

Former French officials famously described America’s position as an “exorbitant privilege.”

Because the world demands dollars, the United States can finance deficits at exceptionally favorable terms. It can effectively exchange financial claims denominated in its own currency for real goods, services, and assets produced elsewhere.

This privilege has underpinned decades of American consumption and financial expansion.

The Sustainability Problem

Every reserve currency system contains an inherent tension.

The world requires increasing quantities of reserve assets. Yet supplying those assets typically requires the issuing country to run deficits. Over time, persistent deficits may weaken confidence in the very assets that the world depends upon.

This contradiction remains one of the most important long-term vulnerabilities of the current order.

Why Gold Is Unlikely to Return

Periods of uncertainty often revive calls for a return to gold-backed money.

History suggests otherwise.

The gold standard provided a clear anchor for confidence. Citizens trusted money because it could be exchanged for gold at fixed rates.

However, that stability came at a significant cost.

Governments surrendered monetary flexibility.

Economic shocks had to be absorbed by real economies rather than central banks.

Deflationary pressures became common.

Financial crises often proved deeper and more prolonged because policymakers lacked the tools needed to stabilize demand.

The Great Depression remains one of the strongest historical examples of these limitations.

Returning to gold would require societies to abandon many of the stabilization mechanisms they now consider essential.

That outcome appears highly unlikely.

The Great Monetary Transformation

The most important monetary development of the past two centuries was not the rise of the dollar.

It was the transition from “anchored money” to “confidence-based money.”

This shift delivered several major benefits:

Greater Economic Stability

Flexible monetary policy has reduced the volatility of both inflation and economic growth.

Enhanced Crisis Management

Modern central banks can inject liquidity during financial panics, helping prevent systemic collapse.

Flexible Exchange Rates

Countries can use currency adjustments to absorb external shocks instead of relying entirely on painful domestic deflation.

Support for Globalization

The modern system enabled large-scale international trade imbalances that facilitated export-led growth models across much of Asia.

This last point is particularly important.

Countries such as China benefited enormously from access to external demand generated by deficit economies, particularly the United States.

Scenarios We Can Largely Rule Out

As investors consider the future of the international monetary system, several commonly discussed outcomes appear improbable.

A Single Global Currency

The euro experience demonstrates the difficulty of maintaining a monetary union without political and fiscal integration.

If relatively similar European economies struggle with monetary union, a global version appears even less realistic.

A Return to Commodity-Backed Money

Gold, commodity baskets, and similar proposals would sacrifice monetary flexibility while introducing substantial price volatility.

The economic costs would likely outweigh the benefits.

Sovereignless Cryptocurrencies as Primary Global Money

Bitcoin and other decentralized cryptocurrencies represent important technological innovations.

However, they face significant obstacles:

- Limited scalability

- Extreme price volatility

- Regulatory resistance

- Competition from sovereign monetary authorities

These constraints make it difficult to envision them becoming the dominant medium of international settlement.

The Most Plausible Long-Term Alternative

After eliminating less likely possibilities, one scenario emerges as the most credible.

A Supranational Currency Supported by Multiple Sovereign Currencies

Rather than replacing national currencies, a future international system could gradually develop around a supranational settlement asset backed by a basket of major sovereign currencies.

The closest existing example is the IMF’s Special Drawing Rights (SDR).

Today SDRs remain limited in scale and use. However, the concept illustrates how a basket-based reserve asset could function.

Such a framework offers several advantages:

- Reduced dependence on any single nation

- Greater geopolitical neutrality

- More balanced distribution of monetary influence

- Enhanced resilience against unilateral policy actions

Over time, expanded versions of these mechanisms could become increasingly attractive.

Why Replacing the Dollar Is So Difficult

Many observers assume that a rising power automatically produces a rising reserve currency.

History suggests otherwise.

Reserve currency status benefits from powerful network effects.

The more people use a currency, the more useful it becomes.

This creates a self-reinforcing cycle.

Even if another economy eventually rivals or surpasses the United States in size, overcoming decades of accumulated financial infrastructure, legal trust, institutional credibility, and market liquidity remains extraordinarily difficult.

This explains why dollar dominance has proven so durable despite repeated predictions of its decline.

China’s Strategic Choices

From YCC Capital’s perspective, China faces several important strategic decisions.

1. Avoid Actively Destabilizing the Existing System

China has benefited substantially from the dollar-centered order through trade integration and export-led growth.

A sudden collapse of the current framework would likely create significant instability.

2. Avoid Pursuing Dollar Replacement as a Primary Objective

Becoming the world’s dominant reserve issuer carries substantial hidden costs.

The United States itself demonstrates how reserve currency status can contribute to financialization, structural deficits, and long-term economic distortions.

3. Expand RMB Settlement Infrastructure

China’s priority should be building resilient payment channels and cross-border settlement systems rather than seeking reserve currency supremacy.

Systems such as CIPS serve this purpose.

4. Support Diversified Global Monetary Architecture

China may find greater strategic advantage in supporting broader multilateral settlement frameworks rather than attempting to elevate the renminbi into a singular dominant role.

5. Strengthen Domestic Demand

China’s most important challenge remains domestic.

The country’s long-term growth outlook continues to face structural headwinds including demographics, debt burdens, property-market weakness, and diminishing returns from investment-led growth.

Sustainable consumption growth remains critical.

Investment Implications

For investors, the key lesson is not that the dollar is about to disappear.

It is that the international monetary system is entering a period of gradual diversification.

We expect:

- Continued reserve diversification into gold

- Greater use of regional settlement arrangements

- Expansion of digital payment infrastructure

- Increased experimentation with basket-based reserve mechanisms

- A slower but persistent reduction in the dollar’s relative dominance

However, none of these developments imply an imminent collapse of dollar leadership.

The transition—if it occurs—will likely unfold over decades rather than years.

Like tectonic plates beneath the ocean, monetary systems often move slowly until the accumulated pressure becomes impossible to ignore.

YCC Capital Strategic View

The future international monetary system is unlikely to resemble either the gold standard of the past or the cryptocurrency visions of the most enthusiastic technologists.

Instead, the most plausible destination is a more diversified framework in which multiple sovereign currencies collectively support a broader supranational settlement architecture.

The dollar will remain central for years to come, but its monopoly on trust is gradually weakening.

The world is not yet abandoning the dollar.

It is beginning to prepare for a future in which it may no longer stand alone.

Sources: Bloomberg, YCC Capital

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

Sign up for free daily market insights and macro research at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com