YCC CAPITAL

Global Fixed Income & Currency Strategy

June 21, 2026

YCC Perspective

For much of the past two years, markets have been conditioned to ask a single question: When will the Federal Reserve cut rates? Following the June FOMC meeting, that question appears increasingly outdated.

The Federal Reserve has not merely held rates steady. It has fundamentally altered the framework through which investors should interpret monetary policy. The June meeting signaled a decisive shift away from forward guidance, a renewed emphasis on inflation control, and a willingness to tolerate slower growth if necessary to restore price stability.

In everyday life, this resembles a household that has spent years battling rising expenses. Rather than temporarily easing the budget to maintain comfort, the family decides to tighten spending despite short-term discomfort because inflation has become the larger long-term threat. The Fed increasingly appears to be making the same choice.

Based on the June policy statement, updated economic projections, and revised dot plot, we believe investors should begin preparing for a world in which higher rates persist longer than consensus expectations.

Executive Summary

Key Takeaways

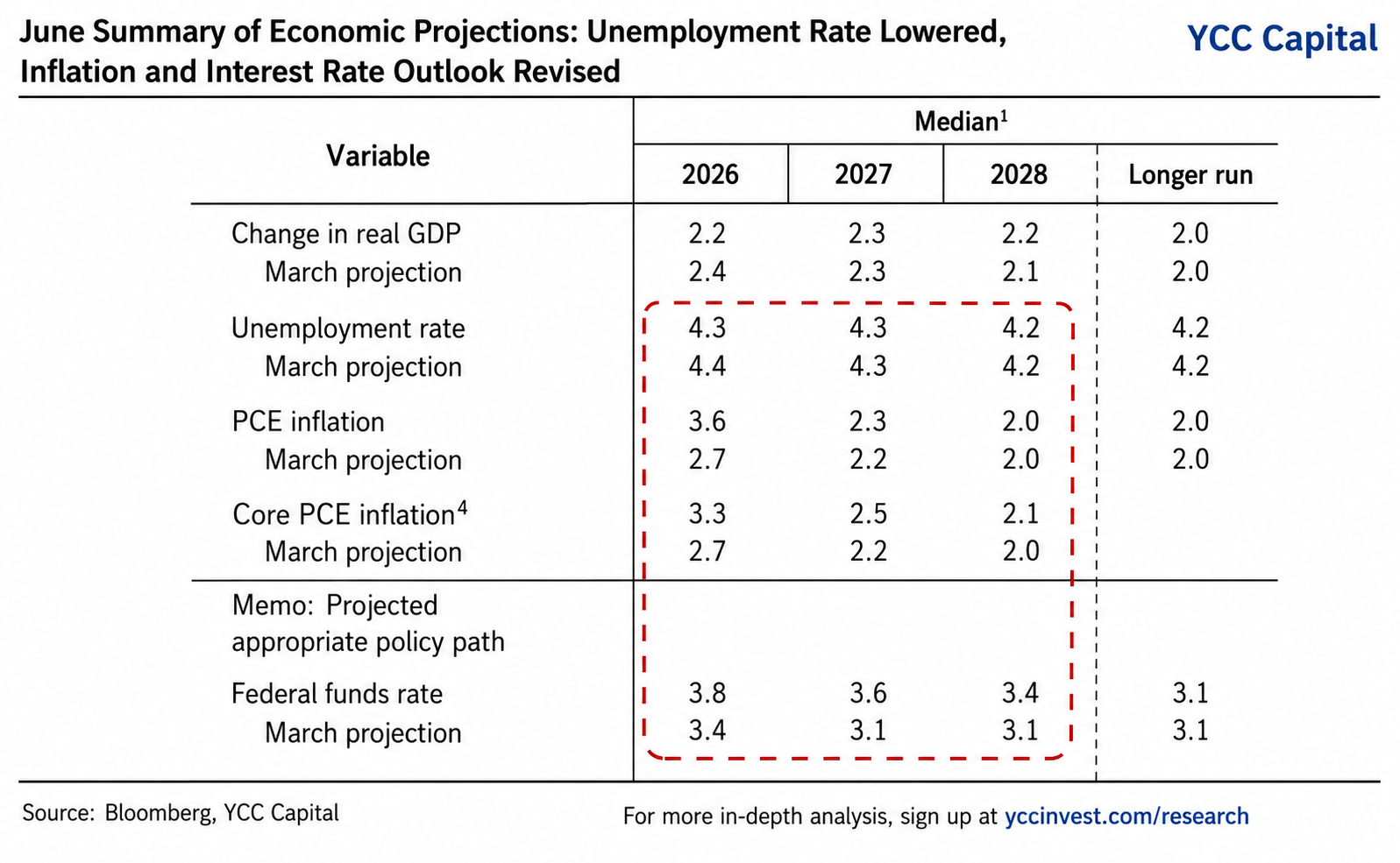

- The Federal Reserve left policy rates unchanged but significantly upgraded inflation projections and interest-rate expectations.

- Language implying future rate cuts was removed.

- The Fed effectively abandoned traditional forward guidance.

- Inflation has re-emerged as the central policy objective.

- Internal discussions have shifted from the timing of rate cuts toward the possibility of additional rate hikes.

- Markets have begun pricing the possibility of another hike as early as October.

- Higher-for-longer rates create a more challenging environment for long-duration assets.

YCC View: The June meeting represents one of the most consequential communication shifts since the post-pandemic tightening cycle began. Investors should not underestimate the significance of this change.

Source: Bloomberg, YCC Capital

Event Overview

In the early hours of June 18, 2026 (Beijing time), the Federal Reserve released its June monetary policy decision.

The Committee:

- Kept the federal funds rate unchanged.

- Released updated quarterly economic projections.

- Published a revised dot plot showing higher expected future policy rates.

- Raised inflation forecasts.

- Lowered unemployment projections.

- Slightly reduced GDP growth expectations.

The combination of these changes sends a clear signal: inflation concerns now outweigh growth concerns within the Federal Reserve’s policy framework.

A New Era Under Governor Warsh

The Fed Turns More Hawkish

Although policy rates were unchanged, the message was anything but neutral.

Several notable changes emerged:

1. Removal of Dovish Language

The Federal Reserve eliminated language that suggested future rate cuts remained the base case.

This is more important than a simple wording adjustment. Markets have relied heavily on forward guidance for more than a decade. By removing such language, policymakers have reduced their commitment to signaling future moves in advance.

2. Simplified Policy Statement

The June statement was materially shorter and more streamlined than prior versions.

3. Reduced Transparency

The Fed departed from the customary practice of providing detailed voting disclosures.

4. Higher Inflation Forecasts

Officials significantly increased projections for:

- Headline PCE inflation

- Core PCE inflation

5. Higher Policy Rate Expectations

The median policy-rate path for the coming years moved higher, indicating officials now expect tighter monetary conditions to persist longer than previously anticipated.

6. Institutional Restructuring

Governor Warsh announced five new monetary-policy working groups and indicated a comprehensive review of Fed communication practices will be completed before year-end.

Taken together, these developments suggest the beginning of a broader institutional transformation rather than a routine policy update.

Inflation Is Back at the Center of the Policy Framework

The Fed’s revised forecasts reveal a significant shift in priorities.

The combination of:

- Higher inflation forecasts

- Lower unemployment forecasts

- Slightly weaker GDP forecasts

suggests a new policy hierarchy.

1. The End of the Traditional Employment-Inflation Tradeoff

Historically, the Federal Reserve balanced two competing mandates:

- Maximum employment

- Price stability

Governor Warsh’s comments imply policymakers no longer view the current labor market as requiring such tradeoffs.

The Fed appears to believe:

- Labor demand remains healthy.

- Labor supply is expanding.

- Employment conditions remain stable.

As a result, policymakers may no longer feel compelled to tolerate elevated inflation simply to support growth.

In practical terms, unless labor markets deteriorate dramatically, inflation control will likely remain the dominant objective.

2. Acknowledgment That Inflation Is More Persistent

The revised projections are effectively an admission that inflation has proven more durable than expected.

After years of repeated forecasts predicting a return to 2%, policymakers now appear increasingly skeptical that disinflation will proceed smoothly.

This is a crucial psychological shift.

For a central bank that has struggled for years to bring inflation back to target, credibility itself becomes an asset worth defending.

The Fed is increasingly tying its institutional reputation to its anti-inflation commitment.

3. A Hawkish Dot Plot

The updated dot plot represents one of the strongest hawkish signals from the meeting.

According to the report, roughly half of policymakers are now considering the possibility of additional rate hikes before year-end.

The policy conversation has therefore shifted from:

“When should we cut?”

to

“Do we need to hike again?”

That is a profound change in market narrative.

The Warsh Doctrine: Lower Transparency, Greater Flexibility

Rebuilding Central Bank Discretion

One of the most striking aspects of the June meeting was the apparent effort to reduce policy transparency.

Measures included:

- Shorter statements

- Less voting disclosure

- Elimination of forward guidance

Rather than guiding markets, the Fed appears to be reclaiming flexibility.

This approach resembles earlier eras of central banking when policymakers intentionally preserved uncertainty in order to maximize policy effectiveness.

While markets may dislike reduced visibility, policymakers may view it as necessary to regain strategic flexibility.

Challenging Traditional Economic Data

Governor Warsh also questioned the usefulness of traditional government economic statistics.

He highlighted:

- Frequent revisions

- Reporting lags

- Historical bias

Instead, he expressed greater confidence in:

- Market pricing

- Private-sector data

- Real-time indicators

This is potentially a major shift.

For decades, investors built macroeconomic frameworks around government releases such as payrolls, CPI, and GDP.

If policymakers increasingly prioritize alternative data sources, traditional macro forecasting models may become less reliable.

A More Unified Fed Than Headlines Suggest

Although the dot plot reveals disagreement over future hikes, the actual decision to leave rates unchanged received unanimous support.

Combined with:

- Communication reforms

- New policy working groups

- Institutional restructuring

the evidence suggests a Federal Reserve becoming more centralized rather than more fragmented.

The significance should not be underestimated. Monetary policy outcomes often depend as much on institutional design as on economic forecasts.

The Core Debate Ahead

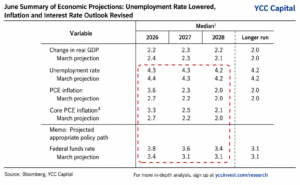

Markets are increasingly pricing the possibility of another rate hike later this year.

The central question now becomes:

Scenario A: Growth Deteriorates

- Demand weakens sharply.

- Recession fears intensify.

- Inflation falls rapidly.

- The Fed eventually pivots.

Scenario B: Inflation Remains Structural

- Growth slows but avoids recession.

- Inflation remains sticky.

- The Fed tolerates weaker activity.

- Rates stay elevated or move higher.

Based on Governor Warsh’s remarks, the Federal Reserve currently appears far more aligned with Scenario B.

The institution seems willing to accept slower growth if doing so increases the probability of restoring price stability.

Asset Allocation Implications

U.S. Treasuries

Short Duration

Short-dated Treasuries remain attractive.

Investors continue to receive meaningful real yields while assuming relatively limited duration risk.

Long Duration

Long-term Treasuries face competing forces:

Bullish

- Slower growth

- Potential recession risks

Bearish

- Persistent inflation

- Higher term premiums

YCC View:

Expect range-bound trading with structurally elevated yields rather than a sustained bond rally.

Source: Bloomberg, YCC Capital

Gold

Short-Term Outlook

Gold faces meaningful pressure.

The combination of:

- Hawkish Fed rhetoric

- Rising real yields

- Higher rate expectations

creates a difficult environment.

Medium-to-Long-Term Outlook

The strategic case remains intact.

Fed institutional changes may increase policy uncertainty over time.

Meanwhile:

- Geopolitical fragmentation

- Reserve diversification

- De-dollarization pressures

continue to support long-term demand.

YCC View:

Short-term vulnerability does not invalidate gold’s strategic role as portfolio insurance.

Source: Bloomberg, YCC Capital

U.S. Equities

Equities face pressure from two directions:

Valuation Headwinds

Higher discount rates reduce support for elevated multiples.

Policy Uncertainty

The possibility of renewed tightening increases volatility.

YCC View:

The medium-term outlook for the U.S. economy remains more resilient than many global peers, but tactical positioning should remain selective and quality-focused until policy visibility improves.

Source: Bloomberg, YCC Capital

Japanese Yen

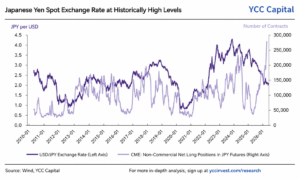

The yen remains vulnerable.

If U.S. rate expectations move higher while the Bank of Japan fails to match that hawkishness, interest-rate differentials could widen further.

The report highlights that speculative short positioning in the yen remains near historically elevated levels, illustrating the market’s continuing bearish bias toward the currency.

YCC View:

Absent a significantly more aggressive BOJ response, further episodes of yen weakness remain possible.

Strategic Conclusion

The June 2026 Federal Reserve meeting may ultimately be remembered less for what it did and more for what it revealed.

The Fed did not raise rates.

But it did something arguably more important:

- It re-centered inflation.

- It reduced reliance on forward guidance.

- It signaled openness to further tightening.

- It challenged traditional macroeconomic frameworks.

For investors, the message is clear:

The era of automatic expectations for rate cuts has ended.

Markets now face a more complex environment in which inflation—not growth—is once again the dominant policy variable.

In that world, discipline, liquidity, and selectivity become increasingly valuable.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

Sign up for our free daily market insights and research updates at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com