YCC CAPITAL

Global Strategy

June 22, 2026

YCC Perspective

Financial markets often move not on certainty, but on the belief that uncertainty is fading.

Last week offered a powerful example. As investors began to price a reduced probability of a prolonged Middle East conflict and a reopening of critical shipping routes through the Strait of Hormuz, oil prices fell sharply and global risk appetite improved. Yet beneath the market relief lies a more complicated reality: neither the geopolitical situation nor monetary policy has become substantially clearer.

Instead, investors are now confronting two new forms of ambiguity.

The first is geopolitical: a U.S.–Iran memorandum that pauses conflict but leaves the hardest disputes unresolved.

The second is monetary: a Federal Reserve increasingly shaped by Chairman Kevin Warsh’s preference for less forward guidance and greater policy discretion.

Markets celebrated peace and stability. The underlying documents suggest investors should remain more cautious.

Executive Summary

Key Conclusions

- Oil prices experienced one of their sharpest weekly declines of the year as markets priced in a lower probability of prolonged disruption in the Middle East.

- Global equities broadly advanced, led by technology-heavy markets including South Korea and Japan.

- The June FOMC meeting delivered a more hawkish message than markets anticipated.

- Chairman Warsh’s first major press conference signaled potentially significant changes to the Fed’s operating framework.

- The U.S.–Iran Memorandum of Understanding (MoU) represents a temporary 60-day framework rather than a permanent peace settlement.

- Major disputes surrounding Iran’s nuclear program, uranium stockpiles, missile development, and governance of the Strait of Hormuz remain unresolved.

- While immediate geopolitical risks have moderated, structural risks remain elevated.

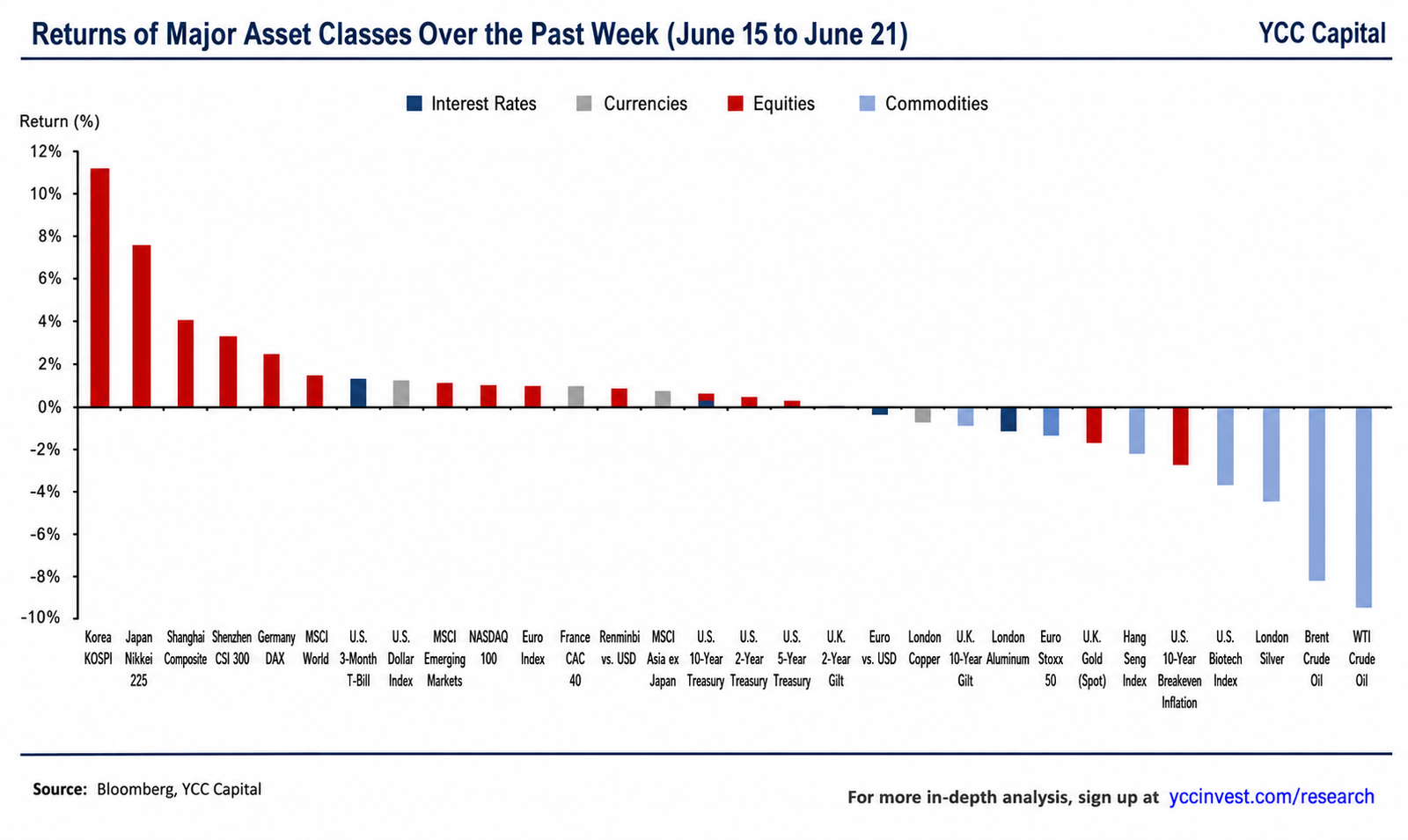

Global Asset Allocation Review

Risk Assets Recover as Oil Collapses

Markets entered last week positioned for escalation.

They exited the week positioning for negotiation.

As military confrontation between the United States and Iran shifted toward a diplomatic process, investors rapidly unwound energy risk premiums. The expectation of resumed maritime traffic through the Strait of Hormuz became a dominant market theme.

The result was a dramatic repricing:

- WTI crude declined approximately 9.8% during the week.

- Brent crude fell roughly 7.7%.

- Precious metals weakened.

- The U.S. dollar strengthened.

- Global equity markets advanced despite a hawkish Federal Reserve meeting.

Among major equity markets:

- South Korea’s KOSPI led gains.

- Japan’s Nikkei 225 continued its strong advance.

- Emerging-market equities outperformed.

- Technology-related sectors remained the primary leadership group.

The resilience of semiconductor stocks and the Magnificent Seven was particularly notable given the simultaneous rise in interest-rate expectations.

This is an important signal.

Markets increasingly view artificial intelligence investment, semiconductor demand, and digital infrastructure spending as structural growth stories capable of overcoming moderate increases in financing costs.

U.S. Economy: Resilient Consumer, Weak Housing

Mixed Economic Signals Continue

Recent U.S. economic releases painted a picture of an economy that remains resilient but uneven.

Retail sales in May exceeded consensus expectations, suggesting consumers continue spending despite elevated interest rates and higher energy costs.

However, housing data told a different story.

Housing starts fell significantly below expectations and dropped to levels not seen since the aftermath of the Global Financial Crisis, underscoring the sensitivity of the housing sector to elevated borrowing costs.

This divergence captures the central challenge facing policymakers:

Consumers remain active.

Interest-rate-sensitive sectors remain weak.

One useful real-world analogy is a family budget during a period of higher gasoline prices. The family may continue traveling and spending overall, but discretionary purchases become increasingly selective.

That appears to be occurring within the U.S. economy.

Although aggregate consumption remains healthy, higher fuel expenditures are crowding out portions of other spending categories. Credit-card data suggest overall consumer activity remains strong, but spending composition has become less favorable.

Federal Reserve: Hawkish Dots, Ambiguous Leadership

Understanding the Warsh Framework

The June FOMC meeting surprised markets with a more hawkish policy outlook than expected. While rates remained unchanged, the updated projections reinforced expectations that monetary policy could remain restrictive for longer.

More important than the rate decision itself was Chairman Kevin Warsh’s broader philosophical approach.

Our interpretation is that Warsh may pursue reform across three dimensions.

1. Less Communication, More Market Volatility

Since the Bernanke era, the Federal Reserve has increasingly relied on forward guidance.

Press conferences, Summary of Economic Projections (SEP), and the dot plot have become essential tools for shaping market expectations.

Warsh appears skeptical of this framework. During his remarks, he emphasized that markets should derive policy expectations from economic fundamentals rather than from extensive Fed signaling.

If implemented fully, this approach would represent one of the largest communication shifts in modern Federal Reserve history.

The likely consequence:

Higher volatility.

Investors would receive fewer policy clues before meetings and would need to infer policy decisions directly from incoming economic data.

The era of the “Fed Put” could become significantly weaker.

2. Trend Dependence Rather Than Data Dependence

Warsh repeatedly emphasized that policymakers should focus on trends rather than isolated economic releases.

Three-month and six-month averages appear likely to receive greater weight than single-month surprises.

This may sound subtle.

In practice, it could materially alter market behavior.

Investors have become conditioned to react aggressively to each inflation print, payroll release, or CPI surprise.

A trend-focused Fed would be less responsive to individual data points and more concerned with persistent directional movements.

Warsh also signaled interest in utilizing broader and more real-time private-sector datasets rather than relying exclusively on traditional government surveys.

3. Balance-Sheet Reduction Combined with Regulatory Easing

Perhaps the most overlooked aspect of the June meeting was discussion surrounding quantitative tightening.

The Fed reaffirmed its commitment to an “ample reserves” framework.

This matters because maintaining ample reserves limits how aggressively the central bank can shrink its balance sheet without causing funding-market disruptions.

Warsh’s apparent objective is not simply to reduce the Fed’s Treasury holdings.

Instead, he appears interested in shifting Treasury ownership from the Federal Reserve back toward commercial banks.

Achieving that outcome would likely require:

- Reduced regulatory burdens.

- Lower liquidity constraints.

- Adjustments to banking supervision.

- Coordination across multiple regulatory agencies.

This implies a slower and more gradual balance-sheet reduction process than some investors fear.

The ultimate effect could resemble a form of reserve requirement easing rather than pure monetary tightening.

Geopolitics: The Reality Behind the U.S.–Iran Memorandum

A Pause, Not a Settlement

The most significant geopolitical development of the week was the signing of a Memorandum of Understanding between the United States and Iran.

Markets interpreted the agreement as a major de-escalation.

That interpretation is directionally correct.

But it is incomplete.

The agreement functions primarily as a 60-day transitional framework designed to:

- Halt immediate military operations.

- Restore maritime activity through the Strait of Hormuz.

- Restart nuclear negotiations.

- Create time for a broader settlement.

Critically, the most contentious issues remain unresolved.

Questions surrounding:

- Uranium enrichment.

- Nuclear infrastructure.

- Missile programs.

- Long-term security arrangements.

have all effectively been deferred into future negotiations.

The Strait of Hormuz Remains the Core Risk

The most important unresolved issue concerns governance of the Strait of Hormuz.

Language within the memorandum refers to future discussions among Iran, Oman, and Gulf states regarding management of the waterway.

However, the United States and Iran continue to hold fundamentally different interpretations of maritime rights.

Iran maintains that it possesses broad authority to regulate traffic when national security concerns arise.

The United States argues that international norms require uninterrupted transit rights for commercial shipping.

These positions are not merely legal disagreements.

They are competing strategic visions.

As a result, the memorandum should be viewed as a framework for future negotiation rather than a resolution of existing disputes.

In practical terms:

The shooting may have paused.

The argument has not ended.

Strategic Investment Implications

Equities

We remain constructive on U.S. technology leadership and broader developed-market equities.

The continued strength of semiconductors and AI-related investment themes suggests structural growth drivers remain intact despite restrictive monetary policy.

Fixed Income

A more opaque Federal Reserve may increase rate volatility.

Investors should prepare for larger market reactions around major economic releases.

Energy

The sharp decline in crude prices reflects reduced geopolitical risk premiums.

However, unresolved Strait of Hormuz issues suggest energy markets remain vulnerable to renewed volatility.

Emerging Markets

Technology-oriented Asian markets continue benefiting from global AI capital expenditure trends.

China remains the relative weak spot within emerging markets due to structural growth challenges, weak private-sector confidence, and continuing balance-sheet pressures.

Risks

- Middle East tensions re-escalate unexpectedly.

- U.S.–Iran negotiations break down during the 60-day framework period.

- Federal Reserve policy remains restrictive longer than anticipated.

- Financial-market liquidity deteriorates under prolonged high interest rates.

- Unexpected policy actions from the Trump administration alter market expectations.

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For free daily market insights and macro research, sign up at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com