YCC CAPITAL

U.S. Themes & Strategy

June 26, 2026

Executive Summary

Every economic expansion eventually reveals its true engine. During the 1990s it was the internet. In the decade following the Global Financial Crisis, ultra-low interest rates and abundant liquidity became the dominant force behind asset appreciation. Today, the United States appears to be entering another defining chapter. Artificial intelligence is no longer merely a technological breakthrough—it has become an increasingly important macroeconomic driver.

This shift explains why traditional indicators often appear contradictory. Manufacturing remains uneven, housing continues to struggle under elevated financing costs, consumers are becoming more selective in their spending, and fiscal deficits remain historically large. Yet economic growth has proven remarkably resilient. The missing piece is a historic wave of AI-related capital expenditure that is reshaping corporate investment behavior and offsetting weakness elsewhere in the economy.

From YCC Capital’s perspective, the United States is transitioning from a consumer-led recovery toward an investment-led expansion centered on digital infrastructure, advanced computing, software, semiconductors, and industrial modernization. This transformation is unlikely to be linear. Inflation pressures generated by energy markets and fiscal stimulus continue to complicate monetary policy, forcing the Federal Reserve into an increasingly difficult balancing act. Nevertheless, the underlying structure of the U.S. economy remains considerably healthier than many investors appreciate.

The coming twelve months are therefore unlikely to resemble either the rapid post-pandemic rebound or a conventional late-cycle slowdown. Instead, investors should prepare for an economy characterized by uneven sectoral performance, structurally elevated capital spending, and monetary policy that remains considerably tighter than markets previously anticipated.

YCC Perspective

Economic transitions rarely announce themselves clearly. They often begin quietly, with investment patterns changing long before headline growth statistics capture the transformation.

The current U.S. cycle resembles this process. Consumers are no longer providing the overwhelming momentum they did immediately after the pandemic reopening. Instead, businesses have increasingly assumed the role of primary growth driver.

Much like the construction of America’s interstate highway system or the nationwide electrification projects of previous generations, today’s AI infrastructure buildout represents investment whose economic impact extends far beyond the companies making the initial expenditures. Every new hyperscale data center requires electricity, transmission networks, advanced cooling systems, industrial equipment, logistics services, specialized construction, networking hardware, and increasingly sophisticated software ecosystems.

What appears initially as technology investment gradually spreads across manufacturing, utilities, transportation, engineering, and professional services. The multiplier effect becomes increasingly visible across the broader economy.

For investors, this distinction matters enormously. Market participants continue debating whether the United States is approaching recession or achieving a soft landing. We believe this framing misses the more important structural development. The economy is not simply slowing or accelerating—it is changing its composition.

That composition increasingly favors productivity-enhancing investment over debt-fueled consumption.

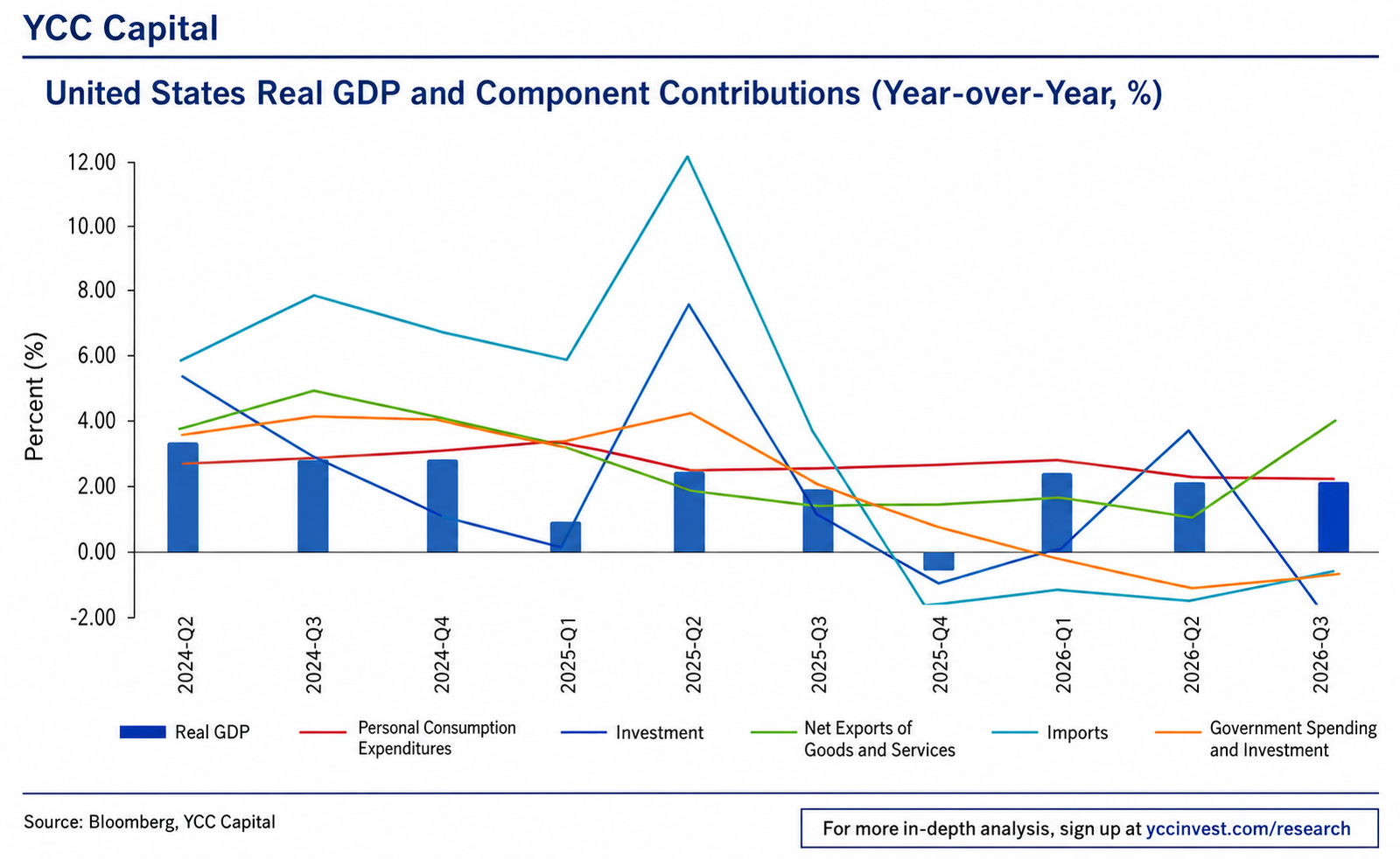

The U.S. Economy Is Becoming Increasingly Bifurcated

Headline GDP growth has moderated compared with the exceptionally strong expansion experienced during the post-pandemic recovery. Yet beneath the aggregate figures lies a much more nuanced story.

Traditional interest-rate-sensitive sectors continue to experience significant pressure. Residential construction remains constrained by elevated mortgage rates. Smaller businesses face tighter financing conditions. Conventional manufacturing outside technology-related industries continues to grow only modestly.

At the same time, investment linked to artificial intelligence has accelerated across multiple categories. Spending on equipment, software, intellectual property products, semiconductor manufacturing, cloud infrastructure, and digital communications continues expanding at a pace that more than offsets weakness elsewhere.

The result is effectively a two-speed economy.

One economy continues operating under the weight of restrictive monetary policy, elevated financing costs, and lingering trade uncertainties. The other benefits from one of the largest private investment cycles witnessed in decades.

This divergence explains why recession forecasts have repeatedly failed to materialize despite widespread expectations of slower growth. Aggregate activity has remained supported because AI-related investment possesses both exceptional scale and unusually broad supply-chain spillover effects.

Unlike speculative investment booms that primarily inflate financial assets, current AI expenditures increasingly translate into tangible physical infrastructure. New manufacturing facilities, energy infrastructure, data centers, industrial automation, and enterprise software deployment collectively generate sustained demand across multiple industries.

From a macroeconomic perspective, this distinction significantly improves the durability of the current expansion.

Consumption Is Losing Momentum—but Not Collapsing

Consumer spending remains the largest contributor to U.S. economic activity. Accordingly, any assessment of the business cycle must begin with household demand.

Recent data suggest that consumption continues to expand, albeit at a noticeably slower pace than during the previous year. Households have become increasingly selective regarding discretionary purchases, particularly goods affected by higher import costs and tariff-related price pressures. Services consumption remains comparatively resilient, supported by continued employment gains and healthy household balance sheets.

This moderation should not be interpreted as a collapse in demand.

Rather, consumers appear to be adapting to a world where borrowing costs remain elevated and purchasing power faces renewed pressure from energy prices. Households are adjusting their spending patterns instead of dramatically reducing expenditures altogether.

A useful analogy is a family undertaking a long road trip. When fuel prices suddenly increase, few travelers abandon the journey entirely. Instead, they choose fewer unnecessary stops, dine out less frequently, and plan their route more carefully. The destination remains unchanged; only the pace of spending evolves.

The U.S. consumer is behaving in much the same way.

Higher energy prices effectively operate as an economy-wide tax, gradually absorbing disposable income that would otherwise support discretionary purchases. Consequently, wage growth that once comfortably exceeded inflation has narrowed considerably.

Although aggregate consumption remains positive, the composition of spending continues shifting toward essential services while discretionary categories recover more gradually.

This transition is consistent with an economy entering a more mature stage of expansion rather than approaching an imminent recession.

Household Balance Sheets Remain a Critical Source of Stability

One of the most overlooked characteristics of the current expansion is the remarkable strength of household balance sheets. While public discussion often centers on rising credit card balances or concerns surrounding consumer debt, the broader financial picture remains considerably healthier than headline narratives suggest.

Household leverage has gradually declined over the past two decades relative to national income. More importantly, millions of homeowners refinanced mortgages during the exceptionally low interest-rate environment of 2020 and 2021. As a result, a significant portion of U.S. households continue to finance their homes at mortgage rates that remain far below prevailing market levels.

This distinction has profound macroeconomic implications.

Unlike previous tightening cycles, higher policy rates have not translated into an immediate surge in mortgage servicing costs for existing homeowners. Consequently, debt-service ratios remain historically manageable despite the Federal Reserve maintaining a restrictive monetary stance.

Credit conditions have certainly tightened for new borrowers, but existing homeowners continue benefiting from financing terms that effectively insulate them from much of today’s interest-rate environment.

The resilience of household balance sheets helps explain why consumer demand has slowed without triggering a more severe contraction.

Income Growth Is Beginning to Lag Inflation

Although household finances remain fundamentally healthy, the direction of income growth deserves close attention.

For much of the post-pandemic recovery, wage gains consistently outpaced inflation. Rising nominal incomes allowed consumers to absorb higher prices without materially reducing spending.

That dynamic has begun to shift.

Recent increases in energy prices have interrupted the disinflation process, pushing headline inflation higher while wage growth has moderated. Average weekly earnings are no longer expanding comfortably above consumer price inflation, reducing the purchasing power available for discretionary expenditures.

The consequence is not an immediate collapse in consumption but a gradual erosion of spending flexibility.

Savings rates have edged lower as households increasingly rely on accumulated wealth to maintain consumption. Asset appreciation across equities and residential real estate continues to provide an important cushion, particularly for middle- and higher-income households. Nevertheless, this support cannot fully substitute for sustained real income growth indefinitely.

Interestingly, wage deceleration has become most visible among higher-income workers.

During earlier stages of the recovery, professionals employed in technology, finance, consulting, and other high-skilled industries experienced exceptionally rapid compensation growth. As labor markets normalize, those gains have moderated considerably.

Lower-income workers continue benefiting from structural labor shortages in many service industries, narrowing wage differentials across income groups.

While this development supports income equality at the margin, it also removes one of the strongest drivers of discretionary consumer spending that characterized the previous two years.

From YCC Capital’s perspective, this represents a gradual normalization rather than an outright deterioration of household fundamentals.

Labor Markets Are Cooling Without Breaking

The labor market remains the single most important variable for assessing recession risk.

Historically, meaningful recessions have almost always been preceded by sustained deterioration in employment conditions. That pattern has yet to emerge.

Payroll growth has stabilized following the moderation observed during the previous year. More importantly, improvements have become increasingly visible across sectors directly benefiting from higher capital expenditure.

Construction employment linked to industrial facilities continues expanding.

Durable goods manufacturing has recorded improving hiring trends.

Professional and business services have begun recovering after a period of relative softness.

Healthcare remains a consistent source of employment creation, while government hiring has ceased acting as a drag on aggregate payroll growth.

Taken together, these developments suggest that labor demand remains sufficiently strong to support continued economic expansion despite restrictive monetary policy.

Labor markets are no longer overheating, but neither are they exhibiting characteristics typically associated with recessionary contractions.

Labor Market Liquidity Is Quietly Improving

Employment dynamics extend beyond headline payroll figures.

Measures of labor market fluidity—including job openings, hiring rates, voluntary resignations, and layoffs—provide valuable insight into underlying economic momentum.

Recent evidence suggests stabilization across several of these indicators.

Job openings have begun recovering after declining throughout much of the previous tightening cycle. Layoff rates remain exceptionally low by historical standards, while initial unemployment claims continue signaling limited labor market stress.

Perhaps most encouraging is the improvement among younger workers.

Historically, unemployment among individuals aged 20 to 24 has often served as an early warning indicator for broader labor market deterioration. During previous recessions, weakness among younger workers emerged well before aggregate unemployment increased materially.

Current trends point in the opposite direction.

Youth unemployment has improved noticeably, reducing the probability that broader labor market weakness is about to emerge.

Voluntary job switching has also normalized after reaching exceptionally elevated levels during the pandemic recovery. Rather than reflecting deteriorating confidence, lower quit rates increasingly indicate a labor market transitioning from extraordinary tightness toward sustainable equilibrium.

The result is an employment environment that appears healthier than many recession forecasts imply.

Artificial Intelligence Has Become America’s Primary Investment Cycle

The defining feature of the current expansion is not consumer resilience.

It is investment.

Specifically, investment directed toward artificial intelligence infrastructure has evolved into the dominant source of incremental economic growth.

Capital expenditures on computing hardware, semiconductor fabrication, networking equipment, cloud infrastructure, enterprise software, industrial automation, and intellectual property continue expanding at extraordinary rates.

Unlike many previous technology cycles, today’s AI investment extends far beyond Silicon Valley.

Electric utilities are expanding transmission capacity to meet surging electricity demand from hyperscale data centers.

Engineering firms are experiencing elevated project pipelines.

Industrial equipment manufacturers are increasing production.

Construction companies specializing in advanced manufacturing facilities report historically strong order books.

Software developers continue benefiting from enterprise-wide digital transformation.

Each investment dollar therefore generates multiplier effects across multiple industries rather than remaining concentrated within technology alone.

This broad economic diffusion significantly enhances the durability of the investment cycle.

AI has evolved beyond an industry.

It is increasingly becoming national economic infrastructure.

From our perspective, this distinction represents one of the most important macroeconomic developments of the decade.

Corporate America Is Entering the Strongest Investment Cycle Since the Internet Revolution

The resilience of AI investment would be far less convincing if it were financed primarily through excessive leverage. That, however, is not what the data suggest.

Corporate balance sheets remain broadly healthy. While non-financial corporate debt remains elevated in absolute terms, leverage has gradually stabilized relative to economic output. More importantly, profitability has improved alongside investment rather than deteriorating under the weight of higher financing costs.

This represents an important departure from many previous business cycles.

Historically, rapid capital expenditure booms often coincided with shrinking profit margins and deteriorating balance sheets, leaving companies vulnerable once financing conditions tightened. Today’s environment looks fundamentally different. Large corporations continue generating robust cash flow, allowing many firms to finance a significant portion of AI-related investment internally rather than relying excessively on debt markets.

The result is a healthier investment cycle—one supported by earnings rather than financial engineering.

This distinction significantly reduces the probability that current capital expenditure will unwind abruptly.

AI Spending Is Spreading Across the Entire Economy

Perhaps the greatest misconception surrounding artificial intelligence is that it benefits only technology companies.

In reality, the investment wave increasingly resembles the construction of America’s interstate highway system. Once the roads are built, nearly every sector of the economy benefits from the improved infrastructure.

Today’s AI ecosystem operates similarly.

Every large-scale data center requires vast quantities of electricity, advanced cooling systems, fiber-optic networks, backup power generation, industrial construction, specialized engineering, logistics support, cybersecurity solutions, and increasingly sophisticated software.

Consequently, AI investment has begun stimulating industries that, at first glance, appear only loosely connected to artificial intelligence.

Manufacturing investment remains particularly strong in advanced machinery, semiconductor equipment, automation technologies, and electrical infrastructure. Spending on software and intellectual property products continues accelerating, reflecting businesses’ growing emphasis on productivity enhancement rather than labor expansion alone.

Utilities have emerged as unexpected beneficiaries. Electricity demand associated with AI infrastructure has materially altered long-term capital expenditure plans for power generation, transmission networks, and grid modernization.

Industrial companies are similarly benefiting from rising demand for specialized equipment, construction services, and automation technologies.

The broader implication is clear: AI is no longer a narrow technology theme. It has evolved into a nationwide investment cycle with increasingly diversified beneficiaries.

Productivity May Become the Economy’s Next Tailwind

One of the most encouraging aspects of sustained AI investment is its potential effect on productivity.

For much of the past fifteen years, U.S. economic growth relied heavily on expanding employment and accommodative monetary policy. Productivity growth remained comparatively modest, limiting the economy’s long-term potential.

Artificial intelligence offers a different pathway.

Rather than simply increasing employment, businesses are increasingly investing in technologies capable of enhancing the productivity of existing workers. Software automation, predictive analytics, machine learning, and intelligent manufacturing systems allow firms to produce more output with the same—or even fewer—resources.

Historically, sustained productivity improvements have been among the healthiest drivers of economic expansion.

They support higher corporate profitability.

They create room for rising real wages.

They reduce inflationary pressure by increasing supply capacity.

And they ultimately allow central banks greater flexibility in balancing growth with price stability.

Although the full productivity gains from AI will likely unfold over many years, early signs are becoming increasingly visible across corporate investment decisions.

For long-term investors, this may ultimately prove to be the most important consequence of the current AI cycle.

Why the Federal Reserve Is Becoming More Concerned About Inflation Again

While economic growth remains supported by investment, monetary policymakers face an increasingly complex challenge.

Earlier expectations centered on multiple interest-rate reductions as inflation gradually retreated toward the Federal Reserve’s target.

That narrative has weakened considerably.

Higher energy prices have interrupted the disinflation process, keeping headline inflation elevated even as core inflation has shown greater stability. Although underlying price pressures have not accelerated dramatically, policymakers have become increasingly cautious about declaring victory over inflation.

The Federal Reserve therefore finds itself confronting a familiar dilemma.

Economic activity remains sufficiently resilient that aggressive policy easing no longer appears necessary.

At the same time, inflation has not slowed decisively enough to justify rapid monetary accommodation.

This combination shifts the balance of risks.

Rather than focusing primarily on protecting employment, policymakers are once again placing greater emphasis on preserving price stability.

From YCC Capital’s perspective, this marks one of the most important changes in the macroeconomic outlook compared with expectations earlier in the year.

Financial markets have progressively moved away from anticipating multiple rate cuts and toward pricing a prolonged period of restrictive policy.

This repricing has significant implications across asset classes.

Quantitative Tightening Returns to the Policy Discussion

Interest rates are only one component of monetary policy.

The Federal Reserve’s balance sheet has become an increasingly important instrument influencing financial conditions.

As inflation risks remain elevated and labor markets continue demonstrating resilience, balance sheet reduction is gradually returning to the policy agenda.

Quantitative tightening provides policymakers with an additional mechanism for withdrawing liquidity without necessarily relying exclusively on higher policy rates.

For investors, this distinction matters.

Liquidity conditions influence risk assets through channels that extend well beyond short-term interest rates. Reduced central bank balance sheets generally translate into tighter financial conditions, higher term premiums in bond markets, and greater market volatility.

Although any future balance sheet normalization is likely to proceed cautiously, investors should not underestimate its potential impact on valuations.

The era of abundant excess liquidity continues to fade.

Markets are increasingly transitioning toward an environment where earnings quality, cash flow generation, and capital discipline matter more than multiple expansion driven by central bank accommodation.

Fiscal Policy Is Supporting Growth—But at an Increasing Cost

While monetary policy has remained restrictive, fiscal policy continues to provide an important counterbalance.

The extension of tax reductions and new fiscal initiatives has prevented government spending from becoming a significant drag on economic activity. Businesses continue benefiting from investment incentives, while many households retain meaningful tax relief that supports disposable income.

In the short run, this combination provides additional momentum for economic growth.

The longer-term picture, however, is considerably more complicated.

Federal debt has expanded to levels that make interest expenses an increasingly important component of government expenditures. Unlike previous decades, when historically low interest rates allowed Washington to finance deficits relatively painlessly, today’s borrowing environment carries a much higher cost.

Interest payments are becoming one of the fastest-growing categories of federal spending.

This creates an uncomfortable policy reality.

Every percentage point increase in borrowing costs now has a substantially larger fiscal impact than in previous economic cycles.

Consequently, inflation has evolved from a purely monetary concern into a fiscal one as well.

Persistently elevated inflation would likely require higher interest rates for longer, further increasing the government’s debt servicing burden. In that sense, maintaining price stability is no longer solely the Federal Reserve’s responsibility—it has become increasingly important for long-term fiscal sustainability.

Energy Prices Remain the Wild Card

If artificial intelligence represents the economy’s strongest tailwind, energy prices remain its greatest source of uncertainty.

Oil price shocks possess a unique ability to influence nearly every corner of the economy simultaneously.

Higher fuel costs reduce household purchasing power.

Transportation expenses increase across supply chains.

Corporate operating margins face additional pressure.

Inflation expectations become more difficult for central banks to anchor.

Unlike shortages confined to a single industry, energy inflation functions as a broad tax on economic activity.

Fortunately, recent inflation pressures remain significantly more contained than those experienced during earlier energy crises.

Core inflation has demonstrated greater resilience than headline measures suggest, indicating that higher oil prices have not yet generated widespread second-round inflation effects across wages and services.

This distinction is crucial.

Should geopolitical tensions ease and energy markets stabilize, headline inflation could resume its downward trajectory without requiring a sharp deterioration in economic growth.

Conversely, a sustained increase in oil prices would significantly complicate the Federal Reserve’s policy outlook, delaying monetary easing and tightening financial conditions further.

Energy therefore remains one of the most important variables investors should monitor over the coming year.

Global Implications: Why U.S. Leadership Continues to Matter

The consequences of America’s investment cycle extend well beyond its own borders.

The United States increasingly occupies a unique position among major developed economies.

Europe continues confronting structural productivity challenges and fragmented fiscal coordination.

China faces persistent weakness in property markets, declining demographic momentum, subdued private-sector confidence, and slowing productivity growth. Although policymakers retain significant fiscal and monetary tools, the economy continues to struggle with structural headwinds that are unlikely to be resolved through cyclical stimulus alone. From YCC Capital’s perspective, these constraints suggest China’s medium-term growth trajectory will remain under pressure despite periodic policy support.

Japan presents a more balanced picture.

While inflation, demographics, and labor shortages remain meaningful challenges, corporate governance reforms, stronger shareholder returns, rising capital expenditure, and gradual wage growth continue supporting the country’s long-term investment outlook. Rather than representing structural decline, Japan’s current adjustments appear more cyclical and should strengthen its medium-term competitiveness.

Against this backdrop, the United States continues attracting a disproportionate share of global capital.

Investors are not simply buying higher economic growth—they are allocating capital toward the world’s deepest capital markets, strongest innovation ecosystem, and most dynamic corporate sector.

This leadership position reinforces demand for U.S. financial assets, particularly during periods of global uncertainty.

Investment Strategy

From an asset allocation perspective, the current macroeconomic environment argues for selectivity rather than broad risk-taking.

U.S. Equities

We remain cautiously constructive on U.S. equities, particularly companies benefiting directly from AI infrastructure, enterprise software, semiconductor ecosystems, industrial automation, power infrastructure, and digital communications.

Valuations across parts of the technology sector are demanding, but earnings growth continues to justify premium multiples for many market leaders. More importantly, investment spending appears increasingly durable rather than speculative.

Investors should also monitor opportunities emerging in industrials, engineering, electrical equipment, utilities, and advanced manufacturing—areas likely to benefit from the second-order effects of AI deployment.

Fixed Income

Treasury yields are likely to remain elevated relative to the ultra-low-rate era.

While outright rate hikes are not our base case, markets may continue adjusting toward fewer rate cuts and a longer period of restrictive monetary policy.

Duration exposure should therefore be accumulated gradually rather than aggressively.

Credit markets remain fundamentally healthy, supported by robust corporate profitability and manageable default risks among investment-grade issuers.

U.S. Dollar

The U.S. dollar should remain structurally supported by relatively higher interest rates, continued capital inflows, and America’s superior growth profile.

Although periodic corrections are inevitable, we see little evidence suggesting a sustained structural decline in the dollar over the medium term.

Commodities

Energy markets remain the principal upside inflation risk.

Gold continues serving as an effective portfolio diversifier against geopolitical uncertainty and fiscal risks, although higher real yields may periodically limit upside momentum.

Industrial metals linked to electrification and digital infrastructure should continue benefiting from long-term capital expenditure trends.

Strategic Takeaways

The defining feature of the next stage of the U.S. expansion is unlikely to be rapid consumer spending or aggressive monetary easing.

Instead, it will be sustained investment.

Artificial intelligence has evolved beyond a technological innovation into a macroeconomic force capable of reshaping productivity, corporate profitability, and long-term economic potential.

That transformation does not eliminate cyclical risks.

Consumers remain vulnerable to energy price shocks.

Inflation has not yet been fully defeated.

Fiscal deficits continue expanding.

Monetary policy is likely to remain restrictive for longer than markets previously expected.

Yet these challenges coexist with one of the strongest structural investment cycles witnessed in decades.

From YCC Capital’s perspective, investors should avoid viewing today’s economy through the traditional lens of recession versus expansion. The more important question is how capital is being reallocated.

Increasingly, capital is flowing toward businesses capable of enhancing productivity, expanding digital infrastructure, modernizing industrial capacity, and supporting the next generation of artificial intelligence.

Those secular forces are unlikely to disappear simply because the business cycle becomes more volatile.

In many respects, the United States is not merely experiencing another recovery.

It is laying the foundations for the next era of economic leadership.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such.

The views, opinions, forecasts, and strategic assessments expressed in this publication represent those of YCC Capital Management as of the publication date and are subject to change without notice as market conditions evolve. Economic forecasts and forward-looking statements inherently involve uncertainty and should not be interpreted as guarantees of future outcomes. Past performance is not indicative of future results.

The analysis contained herein is based upon publicly available information believed to be reliable, including market data, government publications, corporate disclosures, and third-party research. While every reasonable effort has been made to ensure accuracy, YCC Capital Management makes no representation or warranty, express or implied, regarding the completeness, reliability, accuracy, or timeliness of the information presented. Errors and omissions may occur despite careful review.

Any investment strategy discussed in this report may not be suitable for every investor. Market prices, interest rates, exchange rates, geopolitical developments, regulatory changes, technological innovation, and macroeconomic conditions may materially affect investment outcomes. Readers should conduct their own independent due diligence and consult qualified financial, legal, accounting, and tax professionals before making any investment decisions.

YCC Capital Management, its affiliates, principals, directors, employees, research analysts, and associated investment vehicles may from time to time hold long or short positions in securities, currencies, commodities, derivatives, exchange-traded funds, private investments, or other financial instruments discussed in this report. Such positions may change without notice and may differ from the views expressed in this publication.

This report may include forward-looking statements relating to economic conditions, financial markets, monetary policy, technological developments, or geopolitical events. Actual outcomes may differ materially from those anticipated due to risks that cannot be fully predicted or controlled, including policy changes, market volatility, unforeseen economic shocks, and international developments.

No portion of this publication should be reproduced, redistributed, quoted for commercial purposes, republished, or transmitted in any form without the prior written permission of YCC Capital Management.

© 2026 YCC Capital. All rights reserved.

YCC Capital’s flagship investment vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy focused on identifying capital-flow-driven market dislocations, asymmetric investment opportunities, and long-duration structural themes. The Fund is registered in the State of Delaware, United States, and is structured as a Rule 506(c) private investment vehicle. Where performance information is referenced, such information has been independently verified by third-party fund administrators, including NAV Consulting; however, individual investor results may differ depending on subscription timing, fees, and account-specific circumstances.

Contact Us

YCC Capital Management

Sign up for free daily macroeconomic insights, market strategy, investment research, and portfolio commentary by visiting www.yccinvest.com.

We welcome inquiries from institutional investors, family offices, investment professionals, financial advisors, corporate executives, and members of the media interested in YCC Capital’s global macro research and investment perspectives.

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com