YCC CAPITAL

Japan Investment Strategy

June 26, 2026

Executive Summary

For much of the past three decades, investors have viewed every sharp depreciation of the Japanese yen through a familiar lens. Monetary policy divergence widened, carry trades accelerated, speculative positioning increased, and eventually policymakers intervened before the currency stabilized. That framework has repeatedly explained major episodes of yen weakness since the Plaza Accord.

Today, however, the underlying story has evolved.

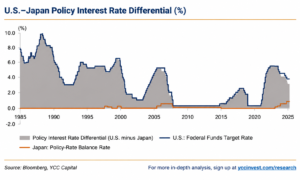

While the interest-rate differential between the United States and Japan remains the immediate driver of USD/JPY, it no longer tells the complete story. A deeper structural transition is taking place beneath the surface. Japan’s fiscal position, long considered manageable because of exceptionally low borrowing costs and deep domestic savings, is gradually becoming a source of macroeconomic vulnerability. Rising government financing costs, slowing domestic growth, demographic headwinds, and the diminishing effectiveness of foreign-exchange intervention are converging into a combination that markets have rarely needed to confront.

The consequence is that the yen is beginning to trade less like the world’s traditional safe-haven currency and more like the funding currency of an economy facing mounting fiscal constraints.

This distinction matters enormously.

Currency markets rarely move because of a single event. Instead, they reprice when investors collectively recognize that an old equilibrium is no longer sustainable. In our assessment, Japan is approaching precisely such an inflection point.

The catalyst for the latest depreciation has been renewed divergence between Federal Reserve and Bank of Japan policy expectations following stronger-than-expected U.S. economic data and persistent inflation pressures. Yet beneath that cyclical backdrop lies a more consequential structural reality: Japan’s ability to finance one of the largest sovereign debt burdens in the developed world increasingly depends on an environment of exceptionally low interest rates. As that environment gradually disappears, fiscal arithmetic—not merely monetary policy—will become progressively more important in determining the long-term direction of the yen.

At YCC Capital, we believe investors should begin thinking about the Japanese currency through a broader macro framework that incorporates sovereign balance-sheet sustainability, geopolitical constraints on reserve management, and the changing role of Japan within global capital flows.

The next major move in the yen may ultimately be driven less by what the Bank of Japan chooses to do and more by what the Japanese government’s balance sheet allows it to do.

The End of a Familiar Playbook

Imagine balancing a household budget with a mortgage fixed at almost zero interest for decades. The monthly payments feel manageable, allowing spending decisions that would otherwise appear aggressive. Then imagine interest rates gradually rising. The outstanding debt has not changed overnight, but the cost of servicing that debt steadily consumes a larger share of income. Eventually, even without increasing borrowing, financial flexibility begins to disappear.

Japan now faces a similar macroeconomic challenge.

For decades, the country’s extraordinary public debt burden attracted remarkably little concern because financing costs remained close to zero. Investors trusted the Bank of Japan’s commitment to accommodative monetary policy, domestic institutions absorbed the overwhelming majority of government bond issuance, and persistent deflation kept nominal yields exceptionally low.

That environment is changing.

Although Japanese interest rates remain modest by international standards, they have risen meaningfully from the ultra-low levels that prevailed throughout the era of quantitative and qualitative easing. Government bond yields have reached their highest levels in years, increasing the future refinancing costs associated with an enormous stock of outstanding debt.

Unlike previous episodes of yen weakness, therefore, today’s depreciation cannot be understood solely through the lens of interest-rate differentials.

Instead, it reflects the interaction of four powerful forces:

- Persistent monetary policy divergence between the Federal Reserve and the Bank of Japan.

- The continued attractiveness of global carry trades financed in yen.

- Increasing political and geopolitical constraints on Japan’s foreign-exchange intervention toolkit.

- A gradual reassessment of Japan’s long-term fiscal sustainability.

Each of these factors reinforces the others.

Higher U.S. yields encourage capital to flow toward dollar-denominated assets. Those flows weaken the yen. A weaker yen raises import prices and inflation in Japan, complicating monetary policy decisions. Meanwhile, higher Japanese yields increase government financing costs, limiting fiscal flexibility and making investors increasingly sensitive to sovereign risk.

What initially appears to be a currency story gradually evolves into a sovereign balance-sheet story.

History suggests that these transitions often occur slowly before accelerating rapidly.

A New Era for the Yen

Since the Plaza Accord in 1985, the yen has experienced several pronounced periods of depreciation. Although each episode unfolded under different economic circumstances, three recurring forces consistently emerged:

First, Japan’s domestic economy weakened relative to the United States.

Second, U.S. interest rates rose relative to Japanese rates, widening the incentive for capital to move abroad.

Third, Japan struggled to maintain technological leadership during periods of global industrial transformation, allowing the United States to attract a disproportionate share of international investment.

Those historical episodes provide useful perspective, but they do not fully explain today’s environment.

The current depreciation follows years of unprecedented monetary accommodation, extraordinary fiscal expansion, pandemic-era policy intervention, shifting global supply chains, and rising geopolitical fragmentation. These forces have fundamentally altered how international investors assess sovereign risk, reserve currencies, and global capital allocation.

Most importantly, the market is beginning to recognize that Japan’s debt dynamics matter not only for bond investors but also for currency markets.

As long as financing costs remained near zero, debt accumulation appeared sustainable. Once yields begin trending higher—even gradually—that assumption deserves renewed scrutiny.

The result is that the yen may increasingly respond to fiscal developments in addition to traditional monetary policy expectations.

For decades, Japan benefited from extraordinary policy credibility. Whether that credibility can be maintained in an environment of structurally higher global interest rates will become one of the defining macroeconomic questions of the coming decade.

Why This Yen Selloff Is Fundamentally Different

Every major currency cycle has a story that investors initially dismiss as temporary. In the early stages, markets often attribute exchange-rate moves to routine interest-rate fluctuations or positioning dynamics. Only later does it become apparent that a deeper structural transition has been underway all along.

We believe the current yen depreciation falls into the latter category.

The consensus explanation remains straightforward: the Federal Reserve has maintained a significantly tighter monetary stance than the Bank of Japan, widening interest-rate differentials and encouraging investors to fund purchases of higher-yielding assets with inexpensive yen borrowing. This explanation is directionally correct, but it is increasingly incomplete.

Our assessment is that the current cycle marks the beginning of a broader reassessment of Japan’s long-term macroeconomic equilibrium. Interest-rate divergence explains why the yen weakened. Fiscal sustainability, however, may determine how far it ultimately falls.

The distinction is subtle but critically important for investors.

Historically, exchange rates have tended to stabilize once policy expectations converged. Today, however, even if the Bank of Japan continues gradually normalizing policy, structural pressures arising from Japan’s fiscal position, demographic profile, and changing role within global capital markets may continue to weigh on the currency.

Markets are beginning to ask a fundamentally different question.

Rather than asking, “When will the Bank of Japan raise rates again?” investors are increasingly asking, “Can Japan afford substantially higher interest rates at all?”

Those are very different questions—and they produce very different investment conclusions.

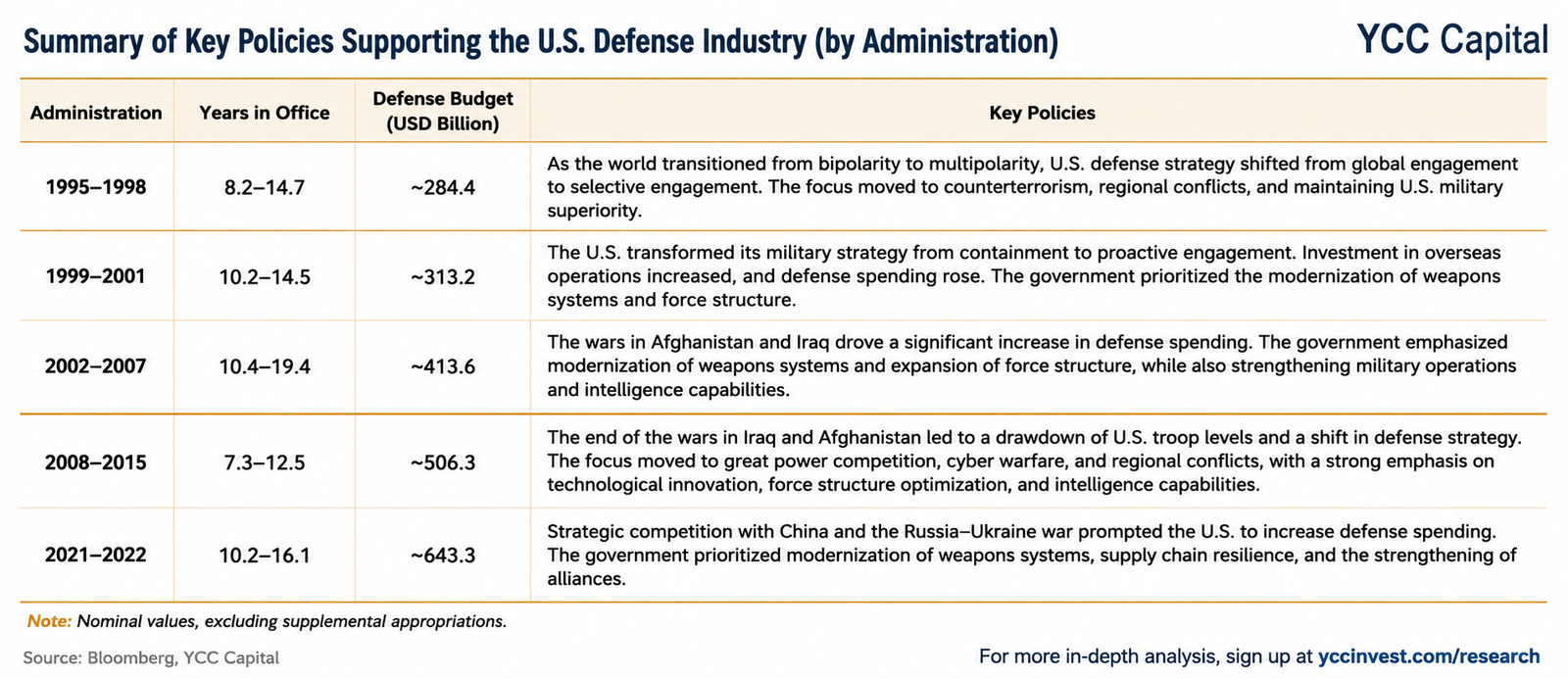

Revisiting the Five Major Yen Depreciation Cycles

Since the Plaza Accord of 1985, the yen has experienced five significant episodes of sustained depreciation against the U.S. dollar. Although each cycle emerged under unique circumstances, the underlying drivers reveal remarkably consistent patterns.

Understanding those episodes helps explain why the current cycle deserves greater attention than many investors appreciate.

1995–1998: America’s Technology Boom Meets Japan’s Banking Crisis

Following years of extraordinary yen strength, the mid-1990s marked the beginning of a powerful reversal.

The United States entered one of the most productive periods in modern economic history as advances in computing, software, and internet infrastructure dramatically accelerated productivity growth. Capital flowed aggressively toward American technology companies, equity valuations expanded rapidly, and the U.S. economy increasingly outperformed its developed-market peers.

Japan, by contrast, remained trapped in the aftermath of its asset-price collapse.

The banking sector continued struggling with non-performing loans accumulated during the bursting of the real estate and equity bubble. Financial institutions remained reluctant to extend credit, private investment stagnated, and domestic demand weakened considerably.

At the same time, the Federal Reserve tightened monetary policy while Japanese rates remained exceptionally low. The widening interest-rate differential reinforced capital flows toward the United States.

The Asian Financial Crisis of 1997 further amplified these pressures. As financial instability spread across the region, confidence in Japan’s economic outlook deteriorated alongside concerns regarding its banking system.

By the end of the cycle, USD/JPY had risen from approximately 80 to nearly 147, representing one of the largest depreciations in the post-war era.

The lesson was clear.

Currency weakness rarely reflected monetary policy alone. It emerged from the interaction of stronger U.S. growth, weaker Japanese fundamentals, and widening capital-return differentials.

1999–2002: Deflation Becomes Structural

The second major depreciation occurred under very different circumstances.

Japan had entered what would later be known as its “lost decade,” characterized by chronically weak inflation, stagnant wage growth, subdued productivity, and persistent economic pessimism.

Rather than tightening policy, the Bank of Japan pioneered zero interest rates and later quantitative easing years before such measures became common globally.

Ironically, even after the collapse of the U.S. technology bubble in 2000, the dollar remained relatively resilient. Global investors continued viewing American financial markets as the world’s deepest and most liquid destination for capital.

Japan, meanwhile, remained associated with deflation rather than growth.

The result was another sustained period of yen weakness despite deteriorating conditions in the United States.

This episode illustrated an important principle that remains relevant today:

Currencies are determined not only by relative growth rates but also by investor confidence regarding long-term policy credibility and future returns on capital.

2004–2007: The Golden Age of Carry Trades

By the mid-2000s, global growth accelerated sharply.

Commodity demand surged, emerging markets expanded rapidly, and risk appetite improved across international financial markets.

The Federal Reserve embarked upon one of the most aggressive tightening cycles in decades.

Japan, however, remained committed to extraordinarily accommodative monetary policy.

The result was an explosive expansion of global carry trades.

Institutional investors borrowed at extremely low Japanese interest rates before investing in higher-yielding assets across the United States, Australia, New Zealand, Brazil, and numerous emerging markets.

This process created persistent structural selling pressure on the yen.

Importantly, the depreciation was not driven primarily by deteriorating Japanese economic conditions.

Instead, it reflected Japan’s transformation into the world’s preferred funding currency.

That distinction remains highly relevant today.

Although many market participants expected the carry trade to diminish after the Bank of Japan began cautiously normalizing policy, the fundamental economics remain overwhelmingly attractive whenever U.S. yields significantly exceed Japanese yields.

2012–2015: Abenomics Changes the Rules

Perhaps no depreciation cycle was as intentional as the one initiated following Shinzo Abe’s return to office.

Abenomics fundamentally altered investor expectations.

The Bank of Japan embraced unprecedented quantitative and qualitative easing, adopted explicit inflation targets, expanded purchases of government bonds and exchange-traded funds, and later introduced Yield Curve Control.

Unlike previous cycles that reflected external developments, this depreciation represented a deliberate policy objective.

Japanese policymakers openly sought a weaker currency to improve export competitiveness, increase imported inflation, and help lift the economy out of chronic deflation.

Markets responded rapidly.

USD/JPY climbed from below 80 to approximately 125 within several years.

For international investors, the message was unmistakable.

The Bank of Japan had become one of the most aggressively accommodative central banks in modern history.

That perception continues influencing global currency markets today.

2021–2022: Inflation Returns—but Only to America

The most recent depreciation before the current cycle began after inflation surged globally following the pandemic.

The Federal Reserve responded with the fastest interest-rate tightening campaign in decades.

The Bank of Japan chose a markedly different path.

Rather than matching U.S. tightening, policymakers maintained Yield Curve Control and continued emphasizing financial stability.

Interest-rate differentials widened dramatically.

Once again, global investors borrowed in yen and purchased higher-yielding dollar assets.

Unlike earlier cycles, however, USD/JPY did not return toward previous equilibrium levels once markets adjusted.

Instead, the exchange rate stabilized at significantly weaker levels.

That development suggested something important had changed.

Markets no longer viewed a return to the pre-pandemic monetary environment as likely.

Three Constants Across Every Cycle

Although the historical backdrop differed substantially, every major depreciation shared three enduring characteristics.

The first was weakening Japanese relative growth.

Whenever U.S. productivity, investment, or innovation substantially outpaced Japan, international capital naturally migrated toward American assets.

The second was widening interest-rate differentials.

Higher U.S. yields consistently encouraged global investors to shift capital toward dollar-denominated securities while financing those positions in yen.

The third was technological leadership.

Each major period of sustained dollar strength coincided with transformative waves of American innovation—from the internet revolution of the 1990s to artificial intelligence and advanced semiconductor leadership today. Capital tends to follow productivity, and productivity tends to follow innovation.

This is one reason YCC Capital remains structurally constructive on U.S. assets over the long term. Innovation is not merely a sector story; it is a macroeconomic force that influences productivity growth, capital formation, corporate profitability, and ultimately exchange rates.

Why 2026 Represents a Structural Break

Yet despite these historical similarities, the present environment differs in one crucial respect.

Previous depreciation episodes were overwhelmingly driven by cyclical forces.

Today’s depreciation increasingly reflects structural constraints.

Japan is no longer simply managing monetary policy divergence. It is managing the interaction between monetary normalization and one of the largest sovereign debt burdens in the developed world.

That interaction fundamentally changes the policy calculus.

Every incremental increase in Japanese government bond yields raises future interest expenses on outstanding debt.

Every attempt to normalize policy therefore carries fiscal consequences.

This dynamic creates a feedback loop rarely encountered in previous decades.

Higher inflation encourages tighter policy.

Tighter policy raises government financing costs.

Rising financing costs constrain fiscal flexibility.

Reduced fiscal flexibility undermines investor confidence.

Weaker confidence places renewed pressure on the currency.

The cycle reinforces itself.

The question facing policymakers is therefore no longer whether higher interest rates are economically justified.

The more difficult question is whether the Japanese public balance sheet can comfortably absorb them over an extended period.

It is here that the current cycle departs most meaningfully from history—and where we believe investors should focus their attention.

Chapter 3 | The Interest Rate Gap: Why Monetary Policy Alone Can No Longer Explain the Yen

For nearly four years, one explanation has dominated virtually every discussion surrounding the Japanese yen: interest-rate differentials.

At first glance, the argument appears straightforward. The Federal Reserve has maintained policy rates at levels not seen in nearly two decades, while the Bank of Japan has only cautiously emerged from almost thirty years of ultra-accommodative monetary policy. The resulting yield differential has encouraged global investors to borrow in yen and invest in higher-yielding U.S. dollar assets, placing persistent downward pressure on the Japanese currency.

There is little disagreement with this basic framework.

However, many investors stop their analysis there.

At YCC Capital, we believe this approach increasingly overlooks the more important question. Monetary policy divergence explains the direction of the yen, but it no longer fully explains its valuation. To understand where USD/JPY could trade over the next several years, investors must examine not only policy rates but also the political and fiscal constraints shaping future central-bank decisions.

In other words, markets are gradually transitioning from pricing interest-rate differentials to pricing policy credibility.

That shift marks an important turning point.

The Federal Reserve Is Likely to Stay Restrictive for Longer Than Markets Once Expected

Throughout much of 2025, financial markets anticipated that the Federal Reserve would begin a steady easing cycle as inflation moderated and economic growth slowed. Investors expected multiple rate cuts, lower Treasury yields, and a narrowing of the interest-rate gap between the United States and Japan.

Instead, the U.S. economy once again demonstrated remarkable resilience.

Labor-market conditions remained considerably stronger than anticipated. Consumer spending continued to expand despite elevated borrowing costs. Productivity gains associated with artificial intelligence investment helped offset some of the drag from tighter financial conditions, while core inflation proved more persistent than policymakers had hoped.

As a result, Federal Reserve communication became progressively more hawkish.

Instead of debating the pace of future easing, policymakers increasingly emphasized the risks of reducing rates prematurely. Market expectations shifted accordingly. Treasury yields remained elevated, the U.S. dollar recovered, and investors significantly reduced expectations for aggressive monetary easing.

This evolution carries profound implications for the yen.

For much of the past decade, markets assumed that U.S. interest rates would eventually converge toward Japan’s extraordinarily low levels. Today, the opposite possibility deserves consideration: Japanese rates may rise only modestly while U.S. rates remain structurally higher than historical norms.

If that proves correct, interest-rate differentials could remain supportive of the dollar for considerably longer than previous currency cycles.

The Bank of Japan Faces a More Difficult Balancing Act

While the Federal Reserve primarily focuses on inflation and employment, the Bank of Japan confronts a far more complicated policy landscape.

On one hand, inflation has finally returned after decades of persistent deflation. Wage growth has improved, imported inflation has increased, and policymakers have gradually dismantled several components of their extraordinary monetary accommodation.

These developments argue in favor of continued normalization.

On the other hand, Japan’s economy remains vulnerable.

Household consumption has recovered only gradually. Population aging continues to constrain labor-force growth. Manufacturing faces increasing competition from regional producers, while elevated energy prices continue to pressure corporate margins and household purchasing power.

Most importantly, every increase in interest rates directly affects the government’s financing costs.

Unlike many advanced economies, Japan’s sovereign debt burden exceeds twice the size of annual economic output. Even modest increases in average borrowing costs eventually translate into materially higher interest expenditures.

Consequently, the Bank of Japan cannot evaluate monetary policy in isolation.

Every policy decision increasingly intersects with fiscal sustainability.

This reality distinguishes Japan from virtually every other major developed economy.

Carry Trades Remain One of the Strongest Structural Forces in Global Markets

To understand why the yen continues to weaken despite periodic interventions, one must appreciate the mechanics of the global carry trade.

Carry strategies are conceptually simple.

Investors borrow funds in currencies where financing costs are exceptionally low and invest those proceeds into assets denominated in currencies offering substantially higher yields.

For years, no currency has fulfilled the funding role more consistently than the Japanese yen.

Even after modest policy normalization, Japanese financing costs remain among the lowest in the developed world. When U.S. Treasury securities offer yields several percentage points above comparable Japanese government bonds, the economic incentive remains compelling.

For large institutional investors—including hedge funds, insurance companies, pension funds, and global macro managers—the arithmetic is difficult to ignore.

Borrow cheaply in yen.

Purchase higher-yielding U.S. assets.

Hedge selectively.

Repeat at scale.

As long as exchange-rate volatility remains manageable, these strategies can generate attractive risk-adjusted returns.

The cumulative effect is persistent selling pressure on the yen.

Importantly, these flows often become self-reinforcing.

A weaker yen improves carry-trade profitability, encouraging additional participation. Increased participation generates further yen weakness, reinforcing expectations that the trade will continue to succeed.

Breaking this cycle generally requires either a sharp narrowing of interest-rate differentials or a significant increase in currency volatility.

At present, neither condition appears imminent.

Why Verbal Intervention Has Lost Much of Its Influence

Japanese authorities have repeatedly expressed concern regarding excessive currency volatility.

Senior government officials have warned against speculative activity, reaffirmed their willingness to intervene when necessary, and emphasized the importance of exchange-rate stability.

These statements occasionally generate short-term appreciation.

However, the effects rarely persist.

The reason is straightforward.

Foreign-exchange markets ultimately respond to underlying capital flows rather than official rhetoric.

If interest-rate differentials remain wide and institutional investors continue reallocating capital toward higher-yielding assets, verbal intervention alone cannot permanently reverse market trends.

History demonstrates this repeatedly.

Currencies may stabilize temporarily following official comments.

Sustained trend reversals, however, require changes in macroeconomic fundamentals.

Markets increasingly recognize this distinction.

Direct Market Intervention Faces New Geopolitical Constraints

Japan possesses one of the world’s largest foreign-exchange reserve portfolios, including substantial holdings of U.S. Treasury securities.

Historically, these reserves have provided policymakers with a powerful intervention mechanism.

By selling dollar-denominated assets and purchasing yen, authorities have occasionally succeeded in slowing episodes of rapid depreciation.

Yet today’s geopolitical environment complicates that strategy.

The United States currently faces elevated fiscal deficits alongside historically large Treasury issuance requirements. Maintaining stable demand for U.S. government debt has become increasingly important for global financial stability.

Large-scale liquidation of Treasury holdings by one of America’s closest allies would therefore carry broader implications extending well beyond currency markets.

Although coordinated policymaking between Washington and Tokyo remains strong, intervention decisions now occur within a far more interconnected geopolitical framework.

In practical terms, Japan almost certainly retains the technical capacity to intervene aggressively.

The question is no longer one of capability.

It is one of political feasibility.

This distinction significantly alters market expectations.

Investors increasingly believe that authorities possess less flexibility than in previous cycles, reducing the deterrent effect of potential intervention.

Why Currency Markets Are Beginning to Price Fiscal Credibility

Perhaps the most important development of the current cycle is that investors are gradually shifting their analytical framework.

Historically, markets evaluated the yen primarily through monetary policy.

Today, sovereign balance-sheet dynamics are attracting increasing attention.

The reasoning is intuitive.

Suppose Japanese government bond yields continue rising over several years.

Initially, this development appears positive for the currency because higher domestic yields should attract capital.

However, those same higher yields simultaneously increase government interest expenditures.

If investors conclude that fiscal sustainability is deteriorating faster than monetary normalization improves returns, higher yields may ultimately weaken rather than strengthen the currency.

This apparent contradiction lies at the heart of Japan’s current predicament.

Higher interest rates support the yen.

Higher interest expenses undermine confidence.

The net outcome depends upon which force dominates.

We believe markets are beginning to recognize this trade-off.

A Narrow Policy Path

Taken together, these dynamics leave Japanese policymakers navigating one of the narrowest policy paths among advanced economies.

Raise rates too slowly, and the interest-rate differential with the United States remains exceptionally wide, encouraging continued yen depreciation.

Raise rates too aggressively, and government financing costs rise more rapidly, increasing fiscal pressures and potentially unsettling bond markets.

Intervene heavily in foreign-exchange markets, and geopolitical considerations become increasingly important.

Avoid intervention altogether, and currency weakness risks feeding imported inflation and reducing household purchasing power.

None of these choices is costless.

Indeed, one of the defining characteristics of the current environment is that nearly every available policy option involves significant trade-offs.

That reality explains why financial markets have become increasingly skeptical that monetary policy alone can stabilize the yen.

The problem is no longer simply about setting the appropriate policy rate.

It is about managing an economy in which monetary policy, fiscal sustainability, demographic change, and geopolitical strategy have become inseparable.

YCC Capital Strategic Perspective

Our central conclusion is that investors should resist interpreting the current depreciation as merely another cyclical currency adjustment.

The widening policy gap between the Federal Reserve and the Bank of Japan remains an important driver, but it is no longer the only driver—and perhaps not even the most consequential one over the medium term.

The greater risk lies in the possibility that markets begin questioning Japan’s long-term fiscal flexibility at precisely the moment policymakers have the least room to respond. Currency markets often react gradually until confidence reaches an inflection point. When that occurs, repricing tends to be swift.

For institutional investors, this argues for viewing the yen not simply as a tactical trading instrument but as a barometer of Japan’s broader macroeconomic credibility. The evolution of government financing costs, sovereign debt dynamics, and policy coordination may ultimately prove more influential than incremental changes in the overnight policy rate.

Chapter 4 | Fiscal Arithmetic: Why Japan’s Sovereign Balance Sheet Could Become the Decisive Driver of the Yen

For most developed economies, monetary policy is the principal variable shaping exchange rates. Governments certainly matter, but central banks usually remain the dominant force because sovereign financing costs fluctuate within relatively manageable ranges.

Japan is different.

Today, the greatest long-term risk to the yen may not originate from the Bank of Japan at all. Instead, it could emerge from an increasingly uncomfortable reality confronting Japan’s Ministry of Finance: a sovereign balance sheet that has become extraordinarily sensitive to even modest increases in borrowing costs.

This distinction fundamentally changes how investors should think about Japanese assets.

For decades, Japan demonstrated that exceptionally high public debt could coexist with financial stability. That experience encouraged many investors to conclude that debt ratios, by themselves, were poor predictors of currency crises.

While that conclusion was broadly correct, it came with an important caveat.

Japan’s debt remained sustainable because interest rates remained extraordinarily low.

Debt levels alone were never the decisive variable.

Debt servicing costs were.

That difference now matters more than at any point since the collapse of Japan’s asset bubble in the early 1990s.

Japan’s Debt Burden Is No Longer an Abstract Statistic

Japan’s gross government debt exceeds 250% of GDP, making it the highest among major developed economies by a considerable margin.

For years, this figure generated surprisingly little market concern.

Critics repeatedly predicted fiscal crisis.

Instead, borrowing costs continued falling.

Investors eventually became accustomed to treating Japan as proof that high debt levels were largely irrelevant in an era of abundant liquidity and persistent deflation.

That interpretation overlooked an essential point.

Japan’s debt was affordable because the average interest rate paid on outstanding government bonds remained close to zero.

Imagine two homeowners each carrying a mortgage worth ten times their annual income.

One pays 0.4% interest.

The other pays 5%.

Although the debt burden appears identical on paper, the financial reality could hardly be more different.

Japan spent decades enjoying the first scenario.

The question investors must now confront is whether that era is gradually ending.

Refinancing Risk Develops Slowly—Then Accelerates

One reason fiscal deterioration has remained largely invisible is the structure of Japan’s government debt.

Unlike floating-rate liabilities, sovereign bonds mature gradually over many years.

Existing bonds issued during the period of ultra-low rates continue paying exceptionally low coupons until maturity.

Consequently, higher market yields do not immediately translate into sharply higher government interest expenses.

Instead, the adjustment occurs progressively.

Every year, a portion of outstanding debt matures.

New bonds must then be issued at prevailing market interest rates.

Initially, the additional expense appears modest.

Over time, however, the cumulative effect becomes increasingly significant.

This process resembles replacing inexpensive long-term fixed-rate mortgages with substantially more expensive refinancing.

The household budget remains stable initially.

Several years later, monthly payments begin consuming a much larger share of income.

National finances operate according to similar arithmetic.

Rising Bond Yields Carry Outsized Fiscal Consequences

Japanese government bond yields have already moved meaningfully higher from the extraordinary lows that prevailed throughout the era of Yield Curve Control.

While yields remain modest compared with those of many Western economies, the direction of travel matters more than the absolute level.

For a sovereign carrying debt measured in quadrillions of yen, even relatively small increases in average borrowing costs translate into substantial increases in annual interest expenditure.

An increase of merely one percentage point across refinanced issuance eventually adds tens of billions of dollars in recurring annual interest costs.

Unlike temporary stimulus spending, interest payments produce no additional economic output.

They simply represent the price of servicing yesterday’s borrowing.

As interest expenditure rises, fiscal flexibility inevitably declines.

Governments must either reduce discretionary spending, increase taxation, issue additional debt, or tolerate larger fiscal deficits.

None of these options is politically straightforward.

Fiscal Space Is Becoming Increasingly Valuable

Japan now finds itself confronting a challenge familiar to many advanced economies.

Public expectations regarding healthcare, pensions, defense spending, industrial policy, and disaster preparedness continue expanding.

Demographic change simultaneously increases demand for government support.

Population aging requires greater healthcare expenditure.

Retirement programs consume larger portions of public budgets.

Labor-force contraction reduces the tax base supporting these commitments.

Meanwhile, geopolitical developments have encouraged substantial increases in defense spending.

Taken individually, each policy objective appears reasonable.

Collectively, however, they compete for increasingly limited fiscal resources.

Every additional yen allocated toward interest payments is one less available for productive investment.

This is how sovereign debt gradually influences economic growth.

Not through dramatic crisis.

Through the steady erosion of fiscal flexibility.

Markets Rarely Panic About Debt Until They Suddenly Do

Financial history demonstrates a recurring pattern.

Debt sustainability rarely deteriorates in a straight line.

Instead, markets often tolerate increasingly elevated debt burdens for extended periods before abruptly reassessing sovereign risk.

This dynamic reflects investor psychology rather than mathematics.

As long as confidence remains intact, refinancing proceeds smoothly.

Bond auctions remain well subscribed.

Currency markets remain relatively stable.

However, if investors begin questioning the government’s future ability to stabilize debt dynamics, financing conditions can deteriorate much faster than policymakers anticipate.

The transition from confidence to caution often unfolds gradually.

The transition from caution to concern can occur remarkably quickly.

Importantly, this does not imply Japan faces an imminent sovereign debt crisis.

Rather, it suggests that markets may become progressively more sensitive to fiscal developments than they have been over the past twenty years.

That sensitivity alone has implications for the currency.

Why the Yen’s Safe-Haven Status Is No Longer Guaranteed

One of the most enduring characteristics of the Japanese yen has been its reputation as a safe-haven currency.

During periods of global financial stress, investors frequently purchased yen despite Japan’s weak domestic growth.

At first glance, this behavior appeared counterintuitive.

The explanation lay in Japan’s position as one of the world’s largest net international creditors.

Japanese households, pension funds, insurers, and corporations accumulated enormous overseas investments over several decades.

When global uncertainty increased, markets expected portions of those foreign assets to be repatriated.

Capital inflows supported the yen.

This mechanism became deeply embedded in market psychology.

However, safe-haven status ultimately depends upon confidence.

If investors increasingly perceive Japan itself as a source of fiscal uncertainty, the traditional repatriation narrative becomes less compelling.

In that environment, the yen could gradually lose part of the structural premium it has historically enjoyed during periods of global volatility.

This possibility remains underappreciated.

Reserve currencies derive their strength not only from liquidity but also from institutional credibility.

Once questions surrounding fiscal sustainability become central to investment decisions, currency dynamics can evolve in unexpected ways.

Lessons from Other Sovereign Episodes

Japan’s circumstances differ materially from those of previous sovereign crises.

Its debt is overwhelmingly denominated in domestic currency.

Domestic institutions continue holding substantial portions of outstanding government bonds.

The country maintains considerable external assets.

These characteristics reduce immediate refinancing risk.

Nevertheless, international experience offers useful lessons.

Countries rarely encounter fiscal stress because investors suddenly discover high debt ratios.

Those debt ratios are usually well known.

Instead, stress emerges when markets conclude that the trajectory of debt has become increasingly difficult to stabilize.

The distinction between stock and trend is essential.

Markets tolerate large debt burdens if they believe future policy remains credible.

They become considerably less patient once confidence regarding future adjustment begins eroding.

Japan is not approaching a classic emerging-market debt crisis.

However, it may be approaching a period during which sovereign credibility exerts greater influence over asset prices than it has in decades.

The Currency Market’s New Focus

Traditionally, currency traders monitored inflation releases, employment reports, and central-bank communications.

Increasingly, they may also monitor fiscal developments.

Budget projections.

Debt issuance calendars.

Government bond auctions.

Interest expenditure.

Tax revenue.

Primary deficits.

These variables have historically belonged primarily to fixed-income analysis.

Today, they increasingly influence foreign-exchange markets as well.

The reason is straightforward.

If fiscal deterioration constrains monetary policy, then fiscal policy indirectly becomes currency policy.

This represents one of the most significant structural changes in Japan’s macroeconomic landscape.

YCC Capital Strategic Perspective

Our assessment is not that Japan faces an imminent fiscal crisis. Such conclusions underestimate the country’s institutional strength, deep domestic savings base, and substantial external assets.

Rather, we believe investors should recognize that the balance of risks has shifted.

For three decades, declining interest rates repeatedly solved fiscal challenges by lowering debt-servicing costs. That tailwind can no longer be assumed. Even a gradual normalization of yields alters the long-term arithmetic of public finance, reducing policymakers’ room for maneuver and increasing the importance of credible fiscal management.

Currency markets rarely wait for definitive evidence before repricing structural risks. They move when probabilities change.

In our view, the evolution of Japan’s fiscal trajectory over the coming decade may prove every bit as important for the yen as the next decision taken by the Bank of Japan.

Chapter 5 | The Limits of Currency Intervention: Why Selling U.S. Treasuries Is No Longer a Simple Solution

Every time the yen approaches psychologically important levels, financial markets begin asking the same question:

Will Japan intervene?

For decades, the answer has often been yes.

Japanese authorities have periodically entered foreign-exchange markets to slow rapid currency depreciation, either through direct purchases of yen or by signaling their willingness to act. On several occasions, intervention temporarily stabilized exchange rates and discouraged speculative positioning.

Yet today’s environment is fundamentally different from previous intervention cycles.

Japan still possesses one of the world’s largest foreign-exchange reserve portfolios. Its financial resources remain substantial. Its technical ability to intervene is unquestioned.

What has changed is the geopolitical and financial environment in which those interventions occur.

Increasingly, the question is no longer whether Japan can intervene.

It is how much freedom it has to do so without creating broader consequences for global financial markets.

Foreign Exchange Reserves Remain Enormous—but They Are Not Unlimited

Japan holds approximately $1.3 trillion in foreign-exchange reserves, making it one of the world’s largest reserve holders.

A significant portion of those reserves consists of U.S. Treasury securities accumulated over decades through trade surpluses and reserve management operations.

These reserves have traditionally served three purposes.

First, they provide confidence that Japan can meet international payment obligations under virtually any circumstance.

Second, they allow policymakers to stabilize disorderly currency markets during periods of exceptional volatility.

Third, they reinforce Japan’s credibility as one of the world’s most financially resilient economies.

On paper, therefore, Japan possesses extraordinary firepower.

However, reserves should not be confused with unlimited policy flexibility.

Every dollar sold to purchase yen alters the composition of Japan’s national balance sheet.

Every intervention carries opportunity costs.

Most importantly, every sale of U.S. Treasuries now occurs within a financial system facing unprecedented financing requirements.

Treasury Markets Have Become More Important Than Ever

To appreciate why intervention has become more complicated, one must first understand the evolving role of the U.S. Treasury market.

Treasuries are no longer simply government bonds.

They represent the foundation of the global financial system.

Banks use them as collateral.

Central banks hold them as reserve assets.

Money-market funds depend upon them for liquidity management.

Pension funds rely upon them to hedge liabilities.

Virtually every major financial institution interacts with the Treasury market on a daily basis.

Consequently, significant disruptions extend far beyond the United States.

They affect global financing conditions.

Today, this importance has become even greater.

Large fiscal deficits require Washington to issue enormous quantities of new debt each year.

At the same time, quantitative tightening has reduced Federal Reserve demand for Treasuries.

The result is a market increasingly dependent upon private-sector and foreign investors to absorb new issuance.

Under these conditions, large-scale Treasury sales by major reserve holders attract considerably more attention than they once did.

Japan’s Intervention Tool Has Become Politically More Complex

Technically, foreign-exchange intervention remains straightforward.

The Ministry of Finance instructs the Bank of Japan to sell dollars and purchase yen.

Operationally, the process can be executed rapidly.

Economically, however, the implications are becoming increasingly complicated.

Large Treasury sales could contribute to upward pressure on U.S. government borrowing costs.

Higher Treasury yields increase financing expenses for Washington.

Those higher yields ripple throughout global credit markets, influencing mortgage rates, corporate borrowing costs, and equity valuations.

Given the strategic alliance between Japan and the United States, policymakers on both sides recognize these broader consequences.

This does not imply that intervention has become impossible.

Rather, it suggests intervention is more likely to be carefully calibrated than overwhelmingly aggressive.

Markets understand this.

Speculators therefore attach less weight to intervention threats than they did during previous decades.

Currency Markets Can Overpower Governments

History offers a humbling lesson for policymakers.

Governments possess considerable resources.

Currency markets possess considerably more.

Daily foreign-exchange turnover exceeds $7 trillion, dwarfing the resources that any single central bank can deploy over extended periods.

Intervention therefore succeeds only under specific conditions.

If markets believe policymakers are defending fundamentally reasonable exchange-rate levels, intervention can alter expectations.

If intervention merely attempts to resist powerful macroeconomic forces, its effectiveness tends to diminish rapidly.

The distinction is critical.

Intervention works best when reinforcing economic fundamentals.

It works poorly when attempting to replace them.

Today’s environment increasingly resembles the latter.

Interest-rate differentials remain substantial.

Carry trades remain profitable.

Capital continues flowing toward higher-yielding U.S. assets.

Against these structural forces, intervention alone becomes progressively less effective.

The Signaling Effect May Matter More Than the Transactions

Ironically, the most valuable aspect of intervention may no longer be the direct purchase of yen.

It may instead be the signal that intervention sends regarding policymakers’ willingness to defend financial stability.

Markets constantly evaluate not only economic variables but also political commitment.

Occasional intervention demonstrates vigilance.

It reminds investors that authorities continue monitoring excessive volatility.

It discourages one-way speculative positioning.

Yet signaling has limits.

If markets repeatedly observe interventions producing only temporary appreciation before depreciation resumes, confidence in the intervention mechanism gradually weakens.

Eventually, markets begin viewing intervention not as a reversal tool but merely as a source of temporary volatility.

That evolution appears increasingly visible today.

Geopolitics Is Reshaping Reserve Management

The global reserve system itself has evolved considerably over the past decade.

Great-power competition has intensified.

Economic security has become intertwined with national security.

Trade policy increasingly influences investment policy.

Financial sanctions have become an important geopolitical instrument.

Within this environment, reserve management decisions carry strategic implications extending beyond portfolio optimization.

Japan must therefore balance several objectives simultaneously.

Maintaining currency stability.

Supporting domestic financial conditions.

Preserving alliance coordination with the United States.

Protecting the long-term value of national reserves.

Each objective is individually reasonable.

Collectively, however, they complicate intervention decisions.

The Ministry of Finance now operates within a policy environment considerably more interconnected than during earlier yen cycles.

Why Markets Care More About Credibility Than Capacity

One misconception frequently appears during discussions of foreign-exchange intervention.

Analysts often ask whether Japan has sufficient reserves to defend the currency.

This question misses the central issue.

Markets already know Japan possesses substantial reserves.

The more relevant question concerns willingness rather than ability.

Would policymakers commit hundreds of billions of dollars if necessary?

Would repeated intervention continue despite limited effectiveness?

Would authorities tolerate higher Treasury yields resulting from reserve liquidation?

These questions cannot be answered through balance-sheet analysis alone.

They involve political judgment.

Markets therefore increasingly evaluate intervention through the lens of policy credibility rather than financial capacity.

A Coordinated Intervention Is Far More Powerful

One important distinction deserves emphasis.

History demonstrates that multilateral intervention is dramatically more effective than unilateral intervention.

When the United States, Japan, and other major central banks coordinate their actions, markets receive a powerful signal that policymakers share common objectives.

Such coordination fundamentally changes investor expectations.

Conversely, unilateral intervention often struggles to overcome persistent macroeconomic trends.

At present, large-scale coordinated intervention appears unlikely unless exchange-rate movements become genuinely disorderly rather than merely unfavorable.

This distinction matters.

A gradual depreciation, even if uncomfortable politically, does not necessarily justify extraordinary international coordination.

Markets recognize this threshold.

Why Policymakers May Tolerate More Weakness Than Investors Expect

Another frequently overlooked consideration is that a weaker yen is not entirely negative for Japan.

Export-oriented manufacturers benefit from improved international competitiveness.

Overseas earnings become more valuable when converted into yen.

Tourism becomes increasingly attractive.

Corporate profits for multinational firms often improve.

The costs, however, have become increasingly visible.

Imported food.

Imported energy.

Consumer purchasing power.

Real household incomes.

Small businesses dependent upon imported inputs.

These competing effects explain why policymakers often tolerate gradual depreciation while resisting abrupt depreciation.

The pace matters as much as the level.

This nuance helps explain why intervention has historically focused on reducing volatility rather than defending a specific exchange rate.

YCC Capital Strategic Perspective

The era when foreign-exchange intervention alone could meaningfully alter the long-term trajectory of the yen is gradually drawing to a close.

That does not diminish the importance of intervention as a stabilizing tool. Rather, it changes its role. Intervention is increasingly becoming a mechanism for smoothing excessive volatility rather than reversing structural trends.

Ultimately, exchange rates follow macroeconomic fundamentals.

If the United States continues offering superior growth, higher real yields, stronger productivity, and greater technological leadership while Japan simultaneously confronts mounting fiscal constraints, even repeated intervention will struggle to produce durable appreciation.

Investors should therefore avoid overreacting to short-term spikes following official action. Such rallies may provide tactical trading opportunities, but they are unlikely to alter the broader structural outlook unless accompanied by meaningful changes in monetary policy, fiscal credibility, or global capital flows.

From our perspective, the market’s focus is gradually shifting away from “Will Japan intervene?” toward “Can intervention still change the long-term narrative?”

That is a much more consequential question.

Chapter 6 | From Safe Haven to Funding Currency: Has the Yen Permanently Changed Its Global Role?

Few currencies have undergone a transformation as profound as the Japanese yen.

For much of the post-war era, the yen symbolized stability. During episodes of geopolitical uncertainty, financial crises, or sharp declines in global equity markets, investors instinctively sought refuge in Japanese assets. Whether the catalyst was the Asian Financial Crisis, the Global Financial Crisis, the European sovereign debt crisis, or the early stages of the COVID-19 pandemic, the yen frequently appreciated even when Japan’s own economic fundamentals appeared relatively weak.

To many market participants, this seemed paradoxical.

Why would capital flow into one of the world’s slowest-growing developed economies during periods of global stress?

The answer lay not in Japan’s domestic growth prospects, but in its position within the global financial architecture.

That architecture, however, is changing.

Today, the yen increasingly behaves less like a defensive reserve currency and more like the world’s preferred funding currency. While this transition has been gradual, its implications for long-term investors are profound. It suggests that future periods of market stress may not produce the same degree of yen appreciation that investors have historically relied upon.

The change is subtle—but potentially structural.

The Original Safe-Haven Narrative

Japan earned its safe-haven status through decades of persistent current account surpluses and disciplined private-sector savings.

Unlike many advanced economies, Japan accumulated enormous net foreign assets over several decades. Households saved aggressively. Pension funds expanded internationally. Insurance companies invested abroad. Japanese corporations built manufacturing networks across North America, Europe, and Asia.

Collectively, these investments made Japan the world’s largest net international creditor.

During periods of financial turmoil, investors assumed that some of these overseas assets would be repatriated.

This expectation alone often generated substantial demand for the yen.

Importantly, actual capital repatriation was sometimes smaller than headlines suggested.

The expectation of repatriation often proved sufficient.

Currency markets frequently move on anticipated flows rather than realized transactions.

As a result, the yen became deeply embedded within global portfolio construction as a defensive asset.

Low Interest Rates Created a Second Identity

Ironically, the very policies that strengthened Japan’s reputation as a stable economy also created a second, very different role for the yen.

Beginning in the late 1990s, Japan entered a prolonged period of near-zero interest rates.

Deflation persisted.

Economic growth slowed.

The Bank of Japan pioneered unconventional monetary policy years before other central banks embraced similar approaches.

Ultra-low financing costs created an attractive opportunity for global investors.

Borrow in yen.

Convert those funds into dollars or other currencies.

Purchase higher-yielding assets.

Capture the yield differential.

Thus, while conservative investors regarded the yen as a safe-haven currency, hedge funds increasingly viewed it as the cheapest source of leverage available anywhere in developed markets.

The same currency acquired two very different identities.

During periods of optimism, investors sold yen to finance carry trades.

During crises, they bought yen as positions unwound.

For many years, these opposing forces coexisted comfortably.

Why That Balance Is Beginning to Shift

The current cycle suggests the historical balance may be changing.

The reason is not simply that U.S. interest rates have increased.

It is that Japan’s domestic vulnerabilities have become more visible.

Higher government debt.

Persistent demographic decline.

Rising fiscal costs.

Slower productivity growth.

Increasing dependence on imported energy.

Collectively, these factors encourage investors to evaluate Japan differently than they did a decade ago.

Instead of viewing the country primarily through the lens of financial stability, markets increasingly evaluate its long-term economic flexibility.

This does not imply Japan has become fundamentally unstable.

Far from it.

Japan remains one of the world’s most sophisticated economies, possessing world-class institutions, substantial household wealth, deep capital markets, and considerable external assets.

Nevertheless, the source of confidence is evolving.

And currency markets are extraordinarily sensitive to changes in perception.

Global Capital Now Has More Attractive Alternatives

Another structural development deserves attention.

For much of the 2000s and early 2010s, many developed economies offered similarly low interest rates.

The difference between borrowing in yen and borrowing in euros or Swiss francs was relatively modest.

Today, however, the landscape looks very different.

The United States offers comparatively high real yields.

Artificial intelligence investment has revitalized productivity expectations.

Corporate earnings remain resilient.

Capital expenditure has accelerated.

Foreign direct investment continues flowing toward advanced manufacturing, semiconductors, energy infrastructure, and digital technologies.

For global investors seeking long-term returns, the opportunity cost of holding low-yielding Japanese assets has therefore increased materially.

Capital increasingly follows productivity.

And productivity increasingly follows innovation.

This is one reason we maintain a cautiously optimistic long-term outlook on the United States while expecting Japan to face greater challenges sustaining capital inflows.

Demographics Matter More Than Markets Sometimes Admit

Demographic trends rarely dominate daily financial headlines.

Yet over long horizons, few variables exert greater influence on economic potential.

Japan’s population continues to age rapidly.

The working-age population has been shrinking for years.

Labor shortages are becoming increasingly widespread.

Healthcare expenditures continue rising.

Pension obligations continue expanding.

These demographic realities influence virtually every component of macroeconomic policy.

Fiscal sustainability.

Tax revenues.

Household consumption.

Housing demand.

Labor productivity.

Potential GDP growth.

No single demographic statistic determines exchange rates.

Collectively, however, demographics influence the long-run attractiveness of an economy.

Investors increasingly recognize that monetary policy cannot permanently offset structural population trends.

Technology Leadership Has Become a Currency Story

One lesson consistently emerges from every major depreciation cycle examined earlier in this report.

The United States has repeatedly strengthened when it has led major technological revolutions.

The internet.

Cloud computing.

Mobile software.

Artificial intelligence.

Advanced semiconductor design.

Biotechnology.

Each wave of innovation has attracted enormous volumes of global capital.

Technology leadership improves productivity.

Higher productivity supports stronger earnings.

Higher earnings encourage investment.

Investment supports currency appreciation.

Japan remains a global leader in precision manufacturing, industrial automation, robotics, advanced materials, and specialized engineering.

These strengths should not be underestimated.

However, many of today’s highest-growth digital ecosystems continue to be concentrated in the United States.

This divergence has meaningful implications for long-term capital allocation.

Could the Yen Lose Its Safe-Haven Premium?

This question deserves careful treatment.

We are not arguing that the yen will suddenly cease functioning as a defensive currency.

Periods of global panic will likely continue generating episodes of yen appreciation as leveraged positions unwind.

However, the magnitude of those rallies may become progressively smaller if investors increasingly associate Japan itself with fiscal challenges.

Safe-haven currencies ultimately derive their strength from confidence.

Confidence in institutions.

Confidence in policy.

Confidence in long-term economic resilience.

Should those foundations weaken—even gradually—the currency’s defensive characteristics may evolve.

Rather than disappearing entirely, the safe-haven premium may simply become less reliable.

For portfolio managers accustomed to treating the yen as an automatic hedge against risk assets, this possibility deserves careful consideration.

Implications for Institutional Asset Allocation

The changing role of the yen carries implications extending well beyond foreign-exchange markets.

Global pension funds may gradually reduce strategic currency hedges.

Insurance companies could reconsider reserve allocations.

Macro hedge funds may assign greater weight to sovereign fiscal indicators when evaluating Japanese positions.

Central banks may increasingly diversify reserve holdings across a broader range of currencies.

Perhaps most importantly, portfolio diversification strategies built upon historical correlations deserve periodic reassessment.

One of the greatest risks in investing is assuming that yesterday’s relationships will remain unchanged indefinitely.

Markets evolve.

Institutions evolve.

Currencies evolve.

Investment frameworks must evolve with them.

YCC Capital Strategic Perspective

The yen is unlikely to lose its importance within the global financial system. Japan remains the world’s fourth-largest economy, one of the largest external creditors, and a cornerstone of international capital markets.

However, we believe its role is changing.

Over the coming decade, investors may increasingly view the yen through two separate lenses.

As a funding currency, it will likely remain attractive so long as Japanese interest rates stay well below those of the United States and other major economies.

As a safe-haven currency, however, its premium may gradually erode if fiscal constraints become more central to the investment narrative.

This distinction matters because it alters the assumptions underlying global portfolio construction. Investors who continue relying exclusively on historical relationships risk overlooking the structural changes already underway.

At YCC Capital, we believe the yen’s transformation represents one of the most important, yet underappreciated, macro developments of this decade. It is not simply a story about exchange rates. It is a story about how shifts in monetary policy, fiscal sustainability, demographics, technological leadership, and geopolitical alignment collectively reshape the foundations of a reserve currency.

The implications extend far beyond Japan.

Chapter 7 | Scenario Analysis: Three Possible Paths for the Yen Through 2028

Forecasting exchange rates with precision is one of the most difficult exercises in macroeconomics. Currency markets incorporate thousands of variables simultaneously, including monetary policy, fiscal dynamics, geopolitical developments, commodity prices, investor sentiment, capital flows, and positioning.

Rather than presenting a single point forecast, YCC Capital believes investors are better served by evaluating multiple plausible paths and assigning probabilities to each. Such an approach recognizes uncertainty while still providing a practical framework for portfolio construction.

Our analysis suggests that the next two years will be defined less by short-term economic data and more by whether Japan can maintain confidence in its fiscal trajectory while navigating a gradually changing global interest-rate environment.

Base Case (Probability: 60%)

Gradual Weakness, but No Disorderly Crisis

Our central scenario assumes that the Federal Reserve maintains a relatively restrictive monetary stance while gradually easing policy only as inflation convincingly moderates. The Bank of Japan continues normalizing cautiously but remains reluctant to tighten aggressively because of concerns surrounding economic growth and rising government financing costs.

Under this scenario, interest-rate differentials narrow only modestly.

Carry trades remain attractive.

Foreign capital continues favoring U.S. assets.

Japanese authorities intervene periodically to reduce excessive volatility but avoid sustained, large-scale market operations.

Meanwhile, Japan’s fiscal position deteriorates gradually rather than abruptly.

Government debt remains manageable because refinancing occurs progressively over time, allowing policymakers to absorb higher borrowing costs without triggering market panic.

However, investor confidence slowly shifts.

Rather than expecting a return toward historical exchange-rate averages, markets increasingly accept a structurally weaker equilibrium for the yen.

Expected USD/JPY Range

160–170

Episodes below 160 remain possible following intervention or temporary shifts in market sentiment, but sustained appreciation appears unlikely without a meaningful narrowing of policy divergence.

Bull Case (Probability: 20%)

Policy Convergence Supports a Stronger Yen

The optimistic scenario requires several developments to occur simultaneously.

First, U.S. inflation declines more rapidly than expected, allowing the Federal Reserve to begin a more substantial easing cycle.

Second, Japanese wage growth becomes increasingly sustainable, enabling the Bank of Japan to continue gradually raising interest rates without undermining domestic demand.

Third, global investors regain confidence that Japan can normalize policy while maintaining fiscal stability.

In this environment, carry trades become less attractive.

Capital outflows moderate.

Japanese government bond markets remain orderly despite higher yields.

The Ministry of Finance needs only limited intervention as market fundamentals begin supporting the currency naturally.

Improved global risk sentiment also encourages renewed foreign investment into selected Japanese sectors, particularly industrial automation, advanced manufacturing, robotics, and semiconductor equipment.

Expected USD/JPY Range

145–155

Although this scenario represents a meaningful appreciation from current levels, we consider a return below 140 unlikely without an unexpectedly severe U.S. economic slowdown.

Bear Case (Probability: 20%)

Fiscal Concerns Trigger a Structural Repricing

The downside scenario does not require a financial crisis.

Instead, it assumes investors gradually conclude that Japan’s fiscal adjustment has become increasingly difficult.

Several developments could contribute.

Long-term government bond yields continue rising.

Debt-servicing costs increase faster than anticipated.

Economic growth remains sluggish.

Political pressure limits fiscal reform.

Markets begin demanding higher compensation for holding long-duration Japanese government debt.

The resulting increase in yields places additional pressure on government finances.

At the same time, the Federal Reserve maintains relatively high policy rates because inflation proves persistent.

Interest-rate differentials remain historically wide.

Carry trades expand further.

Foreign-exchange intervention temporarily slows depreciation but fails to alter the broader trend.

Rather than viewing intervention as a turning point, investors increasingly treat it as an opportunity to rebuild short-yen positions.

Confidence gradually deteriorates.

The currency weakens beyond previous psychological thresholds.

Expected USD/JPY Range

170–180

Although such levels would attract considerable political attention, they cannot be dismissed if markets begin pricing sovereign balance-sheet concerns alongside monetary policy divergence.

What Could Change Our Outlook?

Several developments would materially alter our assessment.

A decisive Federal Reserve easing cycle would narrow interest-rate differentials more rapidly than currently anticipated.

Unexpectedly strong productivity growth in Japan could improve long-term economic expectations.

Meaningful fiscal reform designed to stabilize public finances would strengthen policy credibility.

Conversely, persistent inflation accompanied by weak economic growth—a stagflationary environment—would complicate policy choices significantly.

Similarly, a sharp rise in global energy prices would disproportionately affect Japan because of its dependence on imported fuel, further pressuring the trade balance and domestic purchasing power.

Geopolitical shocks also remain important wildcard risks.

Escalating tensions in East Asia or disruptions to global shipping routes could generate significant short-term currency volatility, although their long-term effects would depend on the policy responses that followed.

Investment Implications

Scenario analysis is valuable only if it informs investment decisions.

In our view, the implications extend well beyond foreign-exchange markets.

Japanese Equities

A weaker yen continues benefiting globally competitive exporters, particularly companies with substantial overseas revenue.

Automobile manufacturers, industrial machinery firms, precision equipment producers, and robotics companies remain relatively well positioned.

However, purely domestic businesses dependent upon imported inputs face increasing margin pressure.

Retailers, airlines, utilities, and food distributors remain particularly exposed to imported inflation.

The distinction between internationally diversified corporations and domestically oriented businesses is likely to become increasingly important.

Japanese Financial Institutions

Banks present a more nuanced picture.

Moderately higher interest rates improve lending margins.

Yet significantly higher government bond yields also reduce the market value of existing bond portfolios.

The interaction between improving profitability and balance-sheet valuation risk will increasingly differentiate stronger institutions from weaker ones.

Investors should therefore evaluate balance-sheet composition rather than relying solely on sector-wide assumptions.

Global Fixed Income

Japan remains one of the world’s largest holders of overseas bonds.

Any meaningful adjustment in domestic yields influences global capital allocation.

If Japanese institutional investors begin repatriating portions of their foreign bond portfolios, international fixed-income markets could experience gradual upward pressure on yields.

While such shifts are unlikely to occur abruptly, they represent an important medium-term consideration for global bond investors.

U.S. Treasury Markets

The relationship between Japan and U.S. Treasuries deserves close attention.

Japan remains a critical participant in the Treasury market.

Large-scale reserve adjustments, changes in currency-hedging costs, or evolving domestic investment opportunities could all influence future demand for U.S. government debt.

Although we do not expect sudden reserve liquidation, even modest changes in Japanese investment behavior could contribute to broader shifts in Treasury market dynamics over time.

Global Asset Allocation

The most significant implication may concern portfolio construction itself.

For years, investors relied on several assumptions.

The yen would strengthen during crises.

Japanese government bonds would remain exceptionally stable.

Interest-rate volatility would remain minimal.

Those assumptions deserve periodic reassessment.

Markets evolve.

Successful investment frameworks evolve with them.

Risk Factors

No macroeconomic forecast is without uncertainty.

Several developments could materially alter the outlook presented in this report:

- A significantly weaker U.S. economy leading to aggressive Federal Reserve easing.

- Faster-than-expected productivity gains within Japan.

- Structural fiscal reforms that improve confidence in long-term debt sustainability.

- Sustained declines in global energy prices, improving Japan’s external balance.

- Unexpected geopolitical agreements reducing global uncertainty.

- Coordinated international currency intervention involving multiple major central banks.

Investors should continually update assumptions as new information becomes available.

YCC Capital Strategic View

The current depreciation of the Japanese yen should not be viewed simply as another cyclical adjustment driven by temporary interest-rate differentials. While monetary policy divergence remains an important catalyst, it increasingly operates alongside deeper structural forces that are reshaping Japan’s macroeconomic landscape.

The defining challenge is no longer whether the Bank of Japan can raise interest rates. It is whether Japan can normalize monetary policy without materially increasing the fiscal burden associated with one of the largest sovereign debt stocks in the developed world.

That distinction changes everything.

For much of the past thirty years, exceptionally low interest rates acted as a powerful stabilizer, masking the long-term implications of an expanding public balance sheet. As yields gradually normalize, that stabilizing force weakens. Fiscal sustainability, government financing costs, and policy credibility become progressively more influential in determining investor confidence.

This does not imply that Japan faces an imminent crisis. On the contrary, the country retains exceptional institutional strength, deep domestic capital markets, world-leading industrial capabilities, and one of the largest net international investment positions in the world.

Nevertheless, structural advantages should not be confused with immunity from changing macroeconomic realities.

At YCC Capital, we believe the next chapter of the yen will be written not only by central bankers but equally by fiscal policymakers, demographic trends, technological competitiveness, and the evolving architecture of global capital flows.

The yen remains one of the world’s most important reserve currencies.

Its future, however, may look meaningfully different from its past.

For long-term investors, recognizing that transition early may prove to be one of the defining macro investment opportunities of the decade.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.