YCC CAPITAL

Innovation Themes & Strategy

A Strategic Framework for Investing Along the AI Theme in the Second Half of 2026

Date: June 26, 2026

Executive Summary

YCC Perspective

Every transformative technology creates two parallel stories. One is the story of genuine innovation that reshapes productivity and society. The other is the story of capital markets racing ahead of reality, pricing in tomorrow’s possibilities long before they fully materialize. Artificial intelligence has now become both stories simultaneously.

The first half of 2026 demonstrated that AI is no longer merely another fast-growing technology sector—it has become the dominant force driving global capital allocation. Investors are increasingly rewarding companies with meaningful exposure to AI infrastructure, semiconductor manufacturing, advanced packaging, cloud computing, and large language models, while sectors lacking direct AI participation have largely been left behind.

History reminds us that every technological revolution—from railroads to electricity to the Internet—experienced periods of excessive optimism. Yet history also teaches that bubbles often finance the infrastructure necessary for decades of subsequent economic expansion. The central question facing investors today is therefore not simply whether AI valuations appear expensive, but whether the industry’s underlying earnings power, technological progress, and strategic importance remain sufficient to justify those valuations.

Our assessment is that while AI-related assets have undoubtedly become expensive, the current cycle continues to enjoy multiple layers of structural support. Rapid advances in model capabilities, falling inference costs, accelerating enterprise adoption, robust earnings growth, and an unprecedented global AI infrastructure investment cycle all provide meaningful fundamental backing. At the same time, valuation risks are accumulating, demanding greater discipline in portfolio construction.

For investors, this is increasingly becoming a market where careful positioning matters more than indiscriminate optimism.

Key Investment Conclusions

During the first half of 2026, global equity markets increasingly concentrated around companies with significant exposure to artificial intelligence. U.S. mega-cap technology firms, semiconductor supply chains across Japan, Korea and Taiwan, together with China’s domestic AI hardware ecosystem, substantially outperformed broader equity markets.

Although valuation multiples across AI-related industries have expanded significantly, they continue to be supported by several fundamental drivers, including continuous improvements in large language model capabilities, declining inference costs, expanding commercial applications, and sustained earnings growth.

Beyond traditional Scaling Law assumptions, current AI valuations also reflect strategic competition among major powers and a pronounced fear of missing out (FOMO). The global AI capital expenditure arms race remains the single most important industrial driver entering the second half of the year.

Within China’s A-share market, AI-related sectors continue to benefit from three major valuation pillars:

- Integration into the global AI supply chain

- Domestic technology substitution driven by export restrictions

- Rapid technological upgrading across semiconductor and computing ecosystems

Taken together, these forces continue to justify elevated valuations, although downside risks are becoming increasingly difficult to ignore.

YCC Capital therefore recommends maintaining a barbell investment strategy. Conservative allocations should emphasize short-duration government bonds and money market instruments to preserve liquidity, while growth allocations should remain concentrated in AI infrastructure and strategically important technologies. Preferred areas include semiconductor equipment, domestic chip manufacturers, memory, printed circuit boards (PCB), optical communication modules, liquid cooling systems, advanced packaging technologies, and leading large language model developers.

Principal Risks

Key downside risks include:

- AI capital expenditure generating lower-than-expected returns

- Slower-than-expected improvement in frontier model capabilities

- Weaker monetization of AI applications

- Delays in the development of China’s domestic computing ecosystem

- Rising U.S. real interest rates or tighter monetary policy compressing valuation multiples

- Excessively crowded market positioning increasing volatility

- Expanded government restrictions on the development or deployment of advanced AI models

Table of Contents

I. AI Dominated Global Equity Markets During the First Half of 2026

II. Are Current AI Valuations Excessive?

III. Why Elevated AI Valuations May Still Be Fundamentally Justified

IV. Every Bubble Eventually Faces Its Reckoning

V. Investment Strategy for China’s AI Sector

VI. Risk Factors

I. AI Dominated Global Equity Markets During the First Half of 2026

Global Capital Is Increasingly Pricing AI Exposure Rather Than Geography

The defining investment theme of the first half of 2026 was neither regional growth nor macroeconomic divergence. Instead, global capital increasingly differentiated companies according to one metric above all others: their degree of exposure to artificial intelligence.

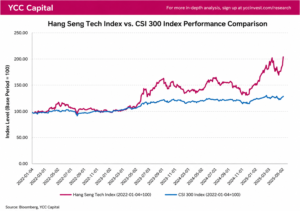

As of June 18, Korea’s KOSPI Index had surged 115.1% year-to-date, making it one of the world’s strongest-performing equity markets. The Philadelphia Semiconductor Index gained 102.5%, while Taiwan’s Weighted Index advanced 60.4%. Japan’s Nikkei 225, China’s STAR 50 Index, and ChiNext Index all substantially outperformed traditional broad-market benchmarks, with gains of 41.1%, 42.2%, and 32.8%, respectively.

By comparison, the Nasdaq 100 rose 20.4%, the S&P 500 gained 9.6%, and China’s CSI 300 increased only 6.7%.

The pattern is remarkably consistent across global markets. Investors have overwhelmingly favored sectors positioned closest to AI infrastructure, including semiconductor fabrication, advanced packaging, AI accelerators, high-performance networking, optical communications, and computing hardware.

Rather than rewarding economic recovery alone, markets have increasingly rewarded participation in what has become the largest technological investment cycle since the commercialization of the Internet.

One useful analogy is the California Gold Rush of the nineteenth century. While countless miners sought fortunes digging for gold, the most durable wealth was often created by businesses selling picks, shovels, railroads, and logistics. Today’s AI economy follows a similar logic. Instead of attempting to identify the ultimate winners among future AI applications, investors have increasingly concentrated capital into the indispensable infrastructure supporting the entire ecosystem.

The result has been an extraordinary global repricing of AI-related assets.

America’s Largest Companies Are Becoming AI Infrastructure Companies

The composition of America’s largest publicly traded companies illustrates this transformation with unusual clarity.

As of June 18, 2026, NVIDIA had become the world’s most valuable listed company, with a market capitalization exceeding US$5 trillion, reflecting its central position in AI accelerated computing and hyperscale data centers.

Alphabet, Microsoft, Amazon, and Meta have each evolved beyond traditional software companies into comprehensive AI infrastructure providers. Their competitive advantages increasingly rest upon cloud computing capacity, enterprise AI integration, proprietary large language models, and developer ecosystems capable of commercializing AI at scale.

Broadcom and Micron occupy equally strategic positions through custom AI chips, networking technologies, high-bandwidth memory (HBM), DRAM, and next-generation storage architectures.

Meanwhile, Apple, Tesla, and SpaceX represent longer-duration optionality tied to edge AI, autonomous robotics, commercial space infrastructure, and physical AI deployment.

Importantly, today’s technology leaders are not simply benefiting from speculative enthusiasm surrounding artificial intelligence. Their valuations increasingly reflect measurable improvements in earnings expectations, expanding cloud revenues, strengthening competitive moats, and sustained capital investment.

As long as AI infrastructure spending, cloud monetization, model capability improvements, and enterprise adoption continue reinforcing one another, premium valuations for leading AI firms remain fundamentally defensible.

The AI Arms Race Has Become a Capital Expenditure Race

Perhaps the clearest signal of industry conviction is the extraordinary pace of capital expenditure by America’s leading cloud providers.

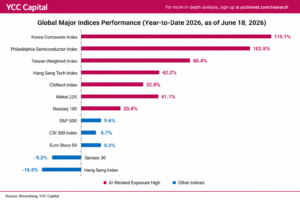

Combined capital expenditures among the five largest AI cloud companies expanded from approximately US$121.4 billion in 2021 to US$375.2 billion in 2025. Consensus expectations now suggest total spending could approach US$760 billion during 2026—more than six times the level observed only five years earlier.

Such acceleration represents more than aggressive corporate investment.

It reflects the realization that AI competition has evolved beyond developing increasingly capable models. Success now depends equally upon securing GPUs, constructing hyperscale data centers, expanding electricity generation, acquiring land, upgrading networking infrastructure, and ensuring long-term computing capacity.

Expected 2026 capital expenditures further illustrate the scale of this race:

- Amazon: approximately US$200 billion

- Microsoft: approximately US$190 billion

- Alphabet: approximately US$185 billion

- Meta: approximately US$135 billion

- Oracle: approximately US$50 billion

Collectively, these investment decisions reveal an important strategic calculation.

For hyperscale cloud providers, the cost of underinvesting in AI infrastructure increasingly exceeds the cost of temporary overinvestment.

A company that falls behind in computing capacity risks more than lower quarterly earnings. It risks permanently losing developers, enterprise customers, technological leadership, and ecosystem advantages that may prove nearly impossible to recover later.

When technology evolves nonlinearly, preserving strategic position becomes every bit as important as maximizing short-term returns.

China’s AI Ecosystem Also Displayed a Clear K-Shaped Market Structure

The same structural divergence was evident within China’s A-share market.

By June 18, 2026, sectors positioned closest to the global AI value chain dramatically outperformed the rest of the domestic equity market. Communication equipment rallied 95.9% year-to-date, while semiconductor companies gained 72.8%. Memory-related businesses advanced 43.6%, optical communication modules climbed 35.2%, electrical equipment appreciated 31.9%, and robotics companies rose 28.7%.

In sharp contrast, traditional sectors continued to struggle. Real estate declined 12.3%, consumer-related industries fell 15.3%, and financial stocks retreated 18.3%.

The message from capital markets was unmistakable.

Rather than rewarding broad economic exposure, investors increasingly concentrated capital in industries positioned at critical bottlenecks within the AI ecosystem—those supplying computing infrastructure, enabling domestic semiconductor substitution, participating in global export supply chains, or benefiting directly from rapid technological iteration.

However, this concentration also raises the performance threshold for future earnings. As valuation premiums migrate further upstream into hardware bottlenecks and critical infrastructure providers, investors will increasingly demand tangible evidence through accelerating orders, expanding margins, and sustained earnings growth.

Momentum alone will no longer be sufficient.

Valuations Have Expanded Sharply—But High Multiples Do Not Automatically Imply a Bubble

Valuation expansion has been substantial across China’s AI supply chain.

As of June 18, 2026, communication equipment companies traded at approximately 98.6 times earnings, while semiconductor firms commanded valuation multiples approaching 134.6 times earnings.

Memory manufacturers traded near 79.4x earnings, optical communication companies around 72.7x, robotics firms approximately 78.1x, electrical equipment manufacturers roughly 77.8x, and computer hardware businesses around 40.6x.

Traditional sectors presented an entirely different picture.

Financial institutions traded at only 14.0x earnings, real estate companies averaged 17.4x, while consumer sectors stood near 24.1x.

The valuation gap is therefore historically significant.

Yet expensive assets are not necessarily irrational assets.

High valuation simply indicates that markets have already incorporated expectations of continued earnings upgrades, sustained export demand, accelerating domestic substitution, and ongoing technological advancement.

The real challenge now shifts from valuation expansion toward earnings validation.

Future stock performance will depend less on multiple expansion and increasingly on whether companies can continue delivering stronger revenues, wider margins, improving order books, and consistent profitability.

Markets have already paid for optimism.

Now they will demand proof.

Three Structural Forces Continue Supporting China’s AI Valuation Premium

Despite elevated valuations, three powerful structural drivers continue supporting China’s AI-related sectors.

These factors extend beyond simple investor enthusiasm and instead reflect long-term industrial transformation.

First: Integration into the Global AI Supply Chain

The first support pillar comes from China’s increasingly important role within global AI hardware manufacturing.

Demand generated by American hyperscale cloud providers is now flowing through multiple layers of international supply chains before ultimately reaching Chinese exporters.

Export data illustrates this trend clearly.

By May 2026, China’s exports of AI-related products continued accelerating across multiple categories.

Memory component exports increased 157.9% year-over-year.

Integrated circuit exports expanded 100.7%.

Automatic data processing equipment and related components grew 66.1%.

Transformer exports rose 39.4%.

Importantly, growth is no longer concentrated within a single product category.

Instead, expansion now spans memory, semiconductor devices, servers, networking equipment, and power infrastructure simultaneously.

This suggests that overseas investment in AI infrastructure is steadily transmitting demand into China’s manufacturing ecosystem.

Looking more closely at individual product categories provides additional insight.

Memory remains the strongest leading indicator of AI-related external demand, reflecting robust consumption of HBM memory, enterprise SSDs, and large-scale data center storage.

Integrated circuit exports exceeding 100% year-over-year growth indicate that computing hardware demand remains exceptionally strong.

Server-related equipment and automatic data processing systems suggest that investment is gradually expanding beyond chips into complete hardware ecosystems.

Meanwhile, transformer exports confirm that AI data centers continue requiring enormous investments in electrical infrastructure alongside computing capacity.

Taken together, these trends suggest that global AI demand remains firmly in its infrastructure construction phase rather than approaching maturity.

Second: Domestic Technology Substitution

A second structural driver stems from intensifying technological competition between the United States and China.

Export restrictions, semiconductor controls, and tightening technology sanctions have significantly accelerated China’s efforts to develop indigenous computing capabilities.

While geopolitical rivalry undoubtedly creates economic inefficiencies, it simultaneously strengthens long-term investment incentives for domestic innovation.

Artificial intelligence has increasingly become intertwined with national competitiveness.

Beyond improving productivity, AI is now viewed as a foundational technology influencing economic leadership, scientific discovery, cybersecurity, military capabilities, and strategic autonomy.

Anthropic CEO Dario Amodei famously described future frontier AI as potentially equivalent to “having fifty million geniuses working inside a data center.”

Although the exact figure is symbolic, the underlying implication is profound.

Future AI systems may coordinate millions of specialized digital agents possessing expertise comparable to elite researchers, engineers, scientists, lawyers, physicians, and software developers.

Such systems would dramatically amplify national productive capacity.

Countries achieving meaningful leadership in this technology would likely enjoy significant advantages across economic growth, military modernization, scientific innovation, and geopolitical influence.

Viewed through this lens, current AI investment increasingly resembles an arms race rather than a conventional business cycle.

Governments and corporations alike increasingly operate under the logic that missing this technological transition could carry irreversible strategic consequences.

Third: Rapid Technological Progress Continues Reinforcing Valuations

Unlike many historical speculative episodes, today’s AI industry continues delivering measurable technological improvements at an extraordinary pace.

Model capabilities have advanced continuously across reasoning, programming, multimodal understanding, scientific research, mathematics, and autonomous task execution.

At the same time, inference costs continue falling, enterprise adoption continues rising, and increasingly capable open-source ecosystems are expanding global access.

These developments matter because valuation ultimately depends upon expectations of future cash flows.

Each improvement in model capability expands the range of commercially viable AI applications.

Each decline in inference cost lowers adoption barriers.

Each new enterprise deployment strengthens recurring demand for infrastructure.

The resulting feedback loop continues reinforcing both industry fundamentals and investor confidence.

AI Is Becoming a Strategic Imperative Rather Than a Cyclical Investment Theme

One of the defining characteristics of the current cycle is that AI investment increasingly transcends traditional return-on-investment calculations.

Cloud providers continue expanding capital expenditure despite uncertain near-term payback periods.

Governments continue increasing national AI funding despite fiscal constraints.

Corporations continue integrating AI despite incomplete monetization.

Why?

Because competitive positioning increasingly matters as much as immediate profitability.

When every major participant believes future technological leadership depends upon today’s infrastructure investment, delaying expenditure becomes strategically dangerous.

The greatest perceived risk is no longer overspending.

It is falling permanently behind.

This dynamic helps explain why AI-related valuations have remained elevated even as many investors argue that prices already appear expensive.

Markets are no longer pricing AI solely as another technology sector.

They are pricing AI as foundational infrastructure for the next phase of global economic development.

II. Are Current AI Valuations Excessive?

Artificial intelligence has become the defining investment narrative of this decade. Unsurprisingly, one question now dominates conversations among institutional investors:

Has AI become another dot-com bubble?

The comparison is understandable. Valuations have expanded rapidly, capital spending has reached unprecedented levels, and investor enthusiasm borders on euphoric in certain segments of the market.

Yet drawing direct parallels to the Internet bubble of 2000 risks oversimplifying today’s environment.

History rarely repeats itself precisely. More often, it rhymes.

The current AI cycle shares certain characteristics with previous technological booms, but it also differs in several crucial respects. Today’s industry leaders generate enormous cash flows, command dominant competitive positions, and continue delivering measurable earnings growth alongside rapid technological progress.

The appropriate question is therefore not whether valuations are high—they clearly are—but whether those valuations remain fundamentally supported.

To answer that question, it is helpful to examine several key indicators.

Capital Expenditure: AI Spending Has Reached Internet-Bubble Scale

One of the strongest arguments raised by skeptics concerns the extraordinary pace of capital investment across the AI ecosystem.

By historical standards, today’s spending is enormous.

During the late stages of the Internet boom, Cisco and Intel increased capital expenditures by roughly 80% and 96%, respectively.

Today, the five largest U.S. hyperscale cloud providers are displaying similar—or even more aggressive—investment behavior.

Median capital expenditure growth reached approximately 74% in 2025, while the fastest-growing companies expanded spending by more than 200%.

At first glance, these figures resemble the investment excesses that preceded the collapse of the technology bubble twenty-five years ago.

However, the similarities become less convincing upon closer examination.

During the dot-com era, much investment was financed by optimistic expectations and abundant external capital. Numerous companies possessed limited profitability and uncertain business models.

Today’s AI infrastructure investment is fundamentally different.

The overwhelming majority of spending is being undertaken by highly profitable companies including Microsoft, Amazon, Alphabet, Meta, and Oracle.

These firms already generate substantial operating cash flow, possess dominant cloud computing franchises, and maintain deep enterprise customer relationships.

More importantly, capital spending is directly linked to measurable demand.

Cloud revenue continues expanding.

Remaining Performance Obligations (RPO) continue increasing.

Enterprise AI adoption continues accelerating.

In other words, investment is not occurring in anticipation of hypothetical markets alone—it is supporting businesses that already exist and continue growing.

This distinction does not eliminate risk.

Rather, it changes where investors should focus.

Instead of asking whether companies are spending too much, investors should monitor whether those investments continue producing proportional increases in revenue, utilization rates, and operating cash flow.

The health of the AI cycle ultimately depends not upon the size of capital expenditure itself, but upon its productivity.

Valuations Are Elevated—but the Market Is Not Yet Experiencing a Broad-Based Bubble

Valuation multiples undoubtedly deserve careful attention.

During the peak of the Internet bubble, the Nasdaq 100 traded at valuation levels approaching 250 times earnings.

Cisco reached approximately 208 times earnings.

These extraordinary multiples reflected speculative enthusiasm detached from underlying fundamentals.

Today’s market appears significantly different.

As of June 18, 2026, the Nasdaq 100 traded at roughly 34 times trailing earnings.

Within the AI sector itself, median price-to-earnings multiples among leading companies stood near 48 times earnings.

Some individual companies have indeed reached valuation levels approaching historical extremes, with the highest decile nearing 200 times earnings.

These pockets clearly exhibit speculative characteristics.

Nevertheless, such cases remain exceptions rather than the market average.

Unlike the year 2000, today’s valuation expansion is concentrated primarily within a relatively narrow group of companies possessing dominant technological positions.

The broader technology sector has not entered a generalized speculative frenzy.

This distinction matters.

Broad market bubbles typically involve indiscriminate buying across nearly all technology companies, regardless of quality or profitability.

Today’s investors remain highly selective.

Capital is flowing disproportionately toward businesses possessing genuine competitive advantages in AI infrastructure, computing power, semiconductors, cloud services, and large language models.

Markets may be optimistic.

They are not yet uniformly irrational.

Earnings Growth Continues Supporting Higher Valuations

Perhaps the single most important factor separating today’s AI leaders from many Internet companies of the late 1990s is earnings.

Ultimately, valuation becomes sustainable only when profits expand alongside investor expectations.

Historical comparisons are revealing.

Near the peak of the Internet bubble, Cisco generated earnings growth of roughly 32%, while Intel achieved approximately 44%.

Today’s leading AI companies display remarkably similar—or even stronger—performance.

Median earnings growth across major AI firms stands around 36%, while the strongest companies are recording profit growth exceeding 300%.

This tells an important story.

The current AI cycle is not driven solely by multiple expansion.

Corporate earnings are participating in the rally.

Of course, not every company enjoys such momentum.

Performance dispersion remains significant.

Businesses positioned at critical infrastructure bottlenecks continue delivering exceptional profitability, while firms with weaker competitive advantages often rely more heavily upon future expectations than current earnings.

Consequently, investors should increasingly distinguish between companies whose valuations are justified by realized profitability and those dependent almost entirely upon optimistic projections.

That distinction is likely to become even more important as the cycle matures.

PEG Analysis Suggests Much of the Premium Remains Fundamentally Justified

One useful method for evaluating expensive growth companies is the PEG ratio, which compares valuation multiples with expected earnings growth.

Viewed through this framework, much of today’s AI sector appears less stretched than headline valuation multiples might suggest.

Across representative AI companies, the median PEG ratio remains close to 1.0.

Nearly half of the companies analyzed trade at PEG ratios below one.

In practical terms, this indicates that expected earnings growth broadly offsets elevated valuation multiples.

Markets are paying high prices—but they are also receiving correspondingly strong growth expectations.

Several segments stand out as particularly attractive under this framework.

Memory manufacturers continue benefiting from surging demand for high-bandwidth memory and data center storage.

Optical communication companies remain critical suppliers for hyperscale networking infrastructure.

AI server manufacturers continue expanding alongside cloud capital expenditure.

Printed circuit board producers benefit from increasingly sophisticated hardware architectures.

Several global AI leaders likewise remain positioned in what could be described as the “high growth, reasonable valuation” quadrant despite their elevated headline multiples.

Conversely, companies exhibiting PEG ratios approaching two deserve closer scrutiny.

In these cases, valuation expansion has already moved substantially ahead of earnings expectations.

Should future profit forecasts disappoint, these businesses could experience considerably sharper multiple compression.

The higher the valuation, the smaller the margin for disappointment.

Today’s Market Reflects a Structural Re-Rating Rather Than Pure Speculation

Taken together, current evidence suggests that AI remains in a period of structural revaluation supported by both realized earnings and long-term expectations.

This does not imply valuations cannot become excessive.

History teaches that every transformational technology eventually attracts speculative capital.

Some companies will inevitably disappoint.

Others will fail entirely.

Nevertheless, the market today differs materially from the indiscriminate speculation that characterized the final stages of the dot-com bubble.

Rather than rewarding every company mentioning artificial intelligence, investors continue concentrating capital in businesses possessing genuine technological leadership, meaningful cash flow generation, and strategic relevance within the global AI ecosystem.

That distinction provides an important degree of resilience.

It does not eliminate downside risk—but it does suggest that today’s AI rally rests upon considerably stronger economic foundations than many historical comparisons imply.

For investors, the challenge is therefore becoming increasingly nuanced.

The question is no longer whether AI represents a revolutionary technology.

That debate has largely been settled.

The real question is identifying which companies possess sufficiently durable competitive advantages to justify the premium valuations that markets have already assigned.

Those answers will determine who emerges as the long-term winners after today’s extraordinary enthusiasm eventually gives way to a more disciplined phase of fundamental investing.

III. Why Elevated AI Valuations May Still Be Fundamentally Justified

Valuation alone rarely determines the outcome of a technological revolution.

Every generation of investors eventually reaches a point where prices appear uncomfortably high. Yet some of history’s most transformative companies—from Microsoft to Amazon and Google—looked expensive long before they became substantially more valuable.

Artificial intelligence may ultimately follow a similar trajectory.

While portions of today’s AI ecosystem undoubtedly exhibit speculative characteristics, several structural forces continue to provide meaningful support for elevated valuations. These drivers extend well beyond market enthusiasm and reflect genuine technological progress, accelerating commercial adoption, and intensifying geopolitical competition.

In our view, five factors continue to distinguish the current AI cycle from a conventional speculative bubble.

1. AI Capabilities Continue Advancing at an Extraordinary Pace

The strongest argument supporting today’s valuations is remarkably simple:

The technology continues to improve at an exceptional rate.

Unlike previous speculative episodes, AI is not merely promising future breakthroughs—it is delivering them.

The modern AI era effectively began with Google’s landmark 2017 paper Attention Is All You Need, which introduced the Transformer architecture and fundamentally reshaped machine learning. Three years later, OpenAI demonstrated the commercial potential of large-scale generative models through GPT, initiating an unprecedented acceleration in model capability.

Since then, progress has been relentless.

DeepMind’s AlphaFold revolutionized structural biology by accurately predicting protein structures, a breakthrough that contributed to Demis Hassabis receiving the Nobel Prize in Chemistry.

ChatGPT subsequently transformed artificial intelligence from a specialist research topic into a mainstream technology used daily by hundreds of millions of people worldwide.

Since 2022, frontier models developed by OpenAI, Anthropic, Google, DeepSeek, Alibaba, Kimi, MiniMax, and others have continued achieving rapid improvements across reasoning, coding, mathematics, scientific research, multilingual understanding, and multimodal capabilities.

Unlike many previous technology cycles, progress has not plateaued.

Each successive generation of models demonstrates measurable improvements over its predecessor.

This sustained technological momentum remains one of the strongest fundamental arguments supporting continued investment across the AI ecosystem.

2. Scaling Laws Continue Supporting Massive Infrastructure Investment

Perhaps no concept has influenced AI investment more profoundly than the principle known as the Scaling Law.

The idea is elegantly straightforward.

As computational resources, model parameters, and training data increase, model intelligence improves in a largely predictable manner.

Although researchers continue debating its ultimate limits, there is currently little evidence that this relationship has fundamentally broken down.

For investors, the implications are enormous.

If larger models consistently produce more capable systems, then every major AI company possesses a powerful incentive to invest aggressively in computing infrastructure.

This creates a self-reinforcing cycle.

Greater capital expenditure enables larger computing clusters.

Larger computing clusters enable more capable models.

More capable models attract more users and enterprise customers.

Growing commercial demand justifies additional infrastructure investment.

The cycle then repeats itself.

This positive feedback loop explains why hyperscale cloud providers continue announcing increasingly ambitious investment plans despite already spending hundreds of billions of dollars annually.

From a strategic perspective, slowing investment could mean surrendering technological leadership.

Consequently, the AI infrastructure race increasingly resembles a flywheel rather than a traditional investment cycle.

As long as Scaling Laws remain economically relevant, capital expenditure is likely to remain structurally elevated.

3. Falling Inference Costs Are Accelerating Global AI Adoption

Technological progress alone cannot sustain valuations indefinitely.

Commercial adoption must eventually follow.

Fortunately for the AI industry, this transition is already underway.

One of the least appreciated developments over the past two years has been the dramatic decline in inference costs.

Generating AI outputs has become substantially cheaper.

Lower costs reduce barriers to adoption, making AI economically viable for an expanding range of applications across industries.

China’s National Data Administration provides an illustration of this remarkable expansion.

By March 2026, average daily token usage had exceeded 140 trillion tokens, representing more than a thousand-fold increase compared with early 2024 and more than 40% growth from the end of 2025 alone.

The broader global trend appears equally compelling.

J.P. Morgan estimates that inference token consumption in China could expand from roughly one quadrillion tokens in 2025 to nearly 390 quadrillion tokens by 2030.

Even if actual growth falls short of these projections, the trajectory remains extraordinary.

Much like the rapid decline in cloud computing costs enabled widespread digital transformation over the previous decade, declining AI inference costs are dramatically expanding the universe of commercially viable applications.

Lower prices rarely reduce demand for transformative technologies.

More often, they unleash entirely new markets.

4. Enterprise AI Adoption Continues Accelerating Worldwide

Technological revolutions ultimately succeed when businesses integrate them into everyday operations.

Recent surveys suggest that this process is gaining considerable momentum.

According to international industry research, enterprise AI adoption increased across nearly every major economy during 2026.

Although China and Japan experienced relatively modest year-over-year gains due to already high adoption rates, countries such as the United States, Germany, and India recorded significantly faster increases.

The United States reached an enterprise adoption rate of approximately 41%.

Germany climbed to 37%.

India similarly reached 37%.

China maintained adoption near 29%, reflecting a more mature deployment base.

These figures indicate that AI is steadily transitioning from experimentation toward operational implementation.

Organizations increasingly employ AI not simply to reduce costs, but to enhance software development, automate customer service, improve research productivity, optimize logistics, accelerate engineering design, and support strategic decision-making.

The trend resembles earlier waves of enterprise software adoption.

Initially viewed as optional productivity tools, cloud computing and digital transformation eventually became operational necessities.

Artificial intelligence appears to be following a comparable path.

Once competitors successfully deploy AI at scale, remaining on the sidelines becomes increasingly difficult.

5. The U.S.–China AI Competition Has Become a Structural Driver of Investment

Perhaps the most powerful force supporting today’s valuations lies outside traditional economics.

Artificial intelligence has become a strategic priority for governments.

The competition between the United States and China increasingly extends beyond commercial leadership into questions of national security, technological sovereignty, military capability, and geopolitical influence.

In recent years, the United States has tightened export controls on advanced semiconductor technologies while simultaneously encouraging domestic AI development.

Policy priorities have increasingly shifted toward preserving American technological leadership in frontier AI.

China, meanwhile, has accelerated efforts to develop indigenous semiconductor ecosystems, domestic computing infrastructure, and nationally competitive AI models in response to external restrictions.

This dynamic creates an unusual investment environment.

Neither side believes it can afford to slow down.

Both perceive technological leadership as strategically indispensable.

The result resembles an arms race more than a conventional technology cycle.

Unlike traditional capital investment driven solely by expected financial returns, AI spending increasingly reflects strategic necessity.

When governments and corporations believe losing technological leadership could permanently weaken national competitiveness, investment decisions become less sensitive to short-term profitability.

Missing the next technological wave is perceived as more dangerous than temporarily overspending.

This helps explain why global AI capital expenditure has remained remarkably resilient despite concerns over valuation.

AI Has Become the Operating System of Future Economic Power

Artificial intelligence is no longer viewed simply as another software category.

It is increasingly regarded as the foundational operating system for the next generation of economic growth.

Its implications extend well beyond productivity improvements.

AI influences scientific research, healthcare, advanced manufacturing, defense systems, cybersecurity, financial services, education, logistics, autonomous transportation, and countless other sectors.

Control over frontier AI technologies increasingly implies influence over future industrial competitiveness itself.

This broader strategic significance helps explain why governments, corporations, and investors continue committing enormous financial resources to AI infrastructure.

The investment case therefore extends beyond near-term earnings.

It increasingly reflects expectations regarding long-term geopolitical and technological leadership.

A Virtuous Cycle—or a Dangerous One?

Yet investors should remain intellectually honest.

The same forces supporting today’s extraordinary valuations could eventually amplify future risks.

Rapid technological progress encourages larger capital expenditure.

Larger capital expenditure accelerates model development.

Better models stimulate greater adoption.

Growing adoption reinforces investor optimism.

Investor optimism supports even higher valuations.

Higher valuations facilitate further capital investment.

The cycle becomes increasingly self-reinforcing.

History shows that such positive feedback loops can persist for remarkably long periods.

History also shows that they rarely continue indefinitely.

Recognizing this dual reality is essential.

Current valuations may remain fundamentally supported for longer than many skeptics expect.

At the same time, every additional round of optimism gradually narrows investors’ margin of safety.

The challenge is therefore not deciding whether AI represents a revolutionary technology—it almost certainly does.

The challenge is determining how much of that future has already been priced into today’s markets.

YCC Strategic View

Imagine watching electricity spread across America at the beginning of the twentieth century. Factories looked expensive. Utilities appeared overvalued. Railroads transporting industrial equipment seemed priced for perfection.

Many investors undoubtedly concluded that the opportunity had already passed.

They were simultaneously right—and spectacularly wrong.

Some companies collapsed.

Others became the defining enterprises of the next century.

Artificial intelligence is likely to produce a similar outcome.

The winners will not simply be those associated with AI.

They will be those controlling the indispensable infrastructure, intellectual property, and ecosystems upon which the next digital economy will ultimately be built.

IV. Every Bubble Eventually Faces Its Reckoning

The extraordinary enthusiasm surrounding artificial intelligence has prompted understandable comparisons with previous episodes of technological exuberance. While we believe the AI revolution rests on substantially stronger economic foundations than many historical bubbles, investors should resist the temptation to conclude that this cycle is somehow exempt from financial history.

Every major technological revolution has experienced periods during which capital markets moved ahead of underlying economic reality. Optimism, after all, is rarely linear. It tends to accelerate until expectations become impossible to satisfy.

The challenge for investors is therefore not to predict exactly when enthusiasm may cool, but to distinguish between a structural growth story and the inevitable cycles of overinvestment and correction that accompany transformative technologies.

Technological Revolutions Have Always Followed Similar Financial Patterns

Economic historian Carlota Perez provides one of the most useful frameworks for understanding long-term technological change.

According to her research, every major technological revolution since the eighteenth century has progressed through four broad stages:

- Installation, when new technologies attract large amounts of speculative capital.

- Financial Bubble, as investor enthusiasm increasingly outruns commercial reality.

- Correction and Institutional Adjustment, during which excessive speculation is eliminated.

- Deployment, when the underlying infrastructure built during the bubble supports decades of broad-based economic expansion.

This pattern can be observed repeatedly throughout history.

The Industrial Revolution experienced speculative investment in canals before financial conditions tightened during the 1790s. Although many investors suffered losses, the canal networks themselves remained and helped support Britain’s industrial expansion.

The railway boom of the 1840s followed a similar trajectory. Britain approved thousands of miles of railway construction, much of which ultimately proved uneconomic. Nevertheless, the surviving infrastructure transformed transportation and commerce for generations.

The late nineteenth century witnessed another wave of speculative investment surrounding steel, electricity, chemicals, and global infrastructure. Excessive financial optimism culminated in the Baring Crisis, yet the underlying technologies continued driving industrial development for decades.

The automobile age experienced its own speculative climax during the Roaring Twenties before collapsing into the Great Depression. Despite the market crash, mass production, highways, petroleum infrastructure, and consumer manufacturing became defining features of twentieth-century economic growth.

More recently, the Internet boom reached extraordinary valuation levels before collapsing between 2000 and 2002. Thousands of companies disappeared, but the fiber-optic networks, software infrastructure, and digital ecosystems constructed during that period ultimately enabled the rise of Google, Amazon, cloud computing, e-commerce, smartphones, and today’s digital economy.

History therefore offers a subtle but important lesson.

Financial bubbles often destroy capital.

They rarely destroy transformative technologies.

Indeed, speculative excess frequently finances the very infrastructure required for long-term innovation.

Artificial intelligence is unlikely to prove an exception.

The More Transformational the Technology, the Larger the Bubble

Perez’s framework also suggests another important relationship.

The more disruptive a technology becomes, the greater the likelihood that financial markets will temporarily overestimate both the speed and scale of its economic impact.

Artificial intelligence arguably represents one of the most profound technological advances in modern history.

Unlike previous digital innovations that primarily automated information processing, AI increasingly performs reasoning, software development, scientific research, engineering design, creative production, and decision support.

Its potential influence spans virtually every industry.

Precisely because the opportunity appears so large, capital markets have become willing to discount decades of future growth into today’s prices.

This process may continue for some time.

It also increases the probability that expectations eventually outrun reality.

In our view, investors should not dismiss bubble risks simply because AI is revolutionary.

Paradoxically, the technology’s enormous long-term potential makes speculative excess more—not less—likely.

Weak Links Often Determine the Speed of Technological Progress

One reason technological revolutions frequently disappoint short-term expectations lies in what Stanford economist Chad Jones describes as the Weak Link Theory.

Economic systems resemble interconnected networks rather than isolated technologies.

Improving one component dramatically does not automatically improve the entire system.

A supply chain remains constrained by its slowest participant.

A factory remains limited by its weakest process.

An economy remains constrained by its largest bottleneck.

The same principle applies to artificial intelligence.

AI may enable certain tasks to become ten times more efficient.

Yet if complementary systems—regulation, energy infrastructure, data quality, organizational restructuring, workforce training, legal frameworks, cybersecurity, or enterprise integration—fail to advance at comparable speeds, overall productivity gains will inevitably fall short of investors’ most optimistic expectations.

Markets often price technological revolutions as though every supporting component will improve simultaneously.

Reality rarely cooperates.

This helps explain why financial markets repeatedly become disappointed despite genuine technological progress.

The technology itself succeeds.

Its surrounding ecosystem simply requires more time than investors initially expect.

Potential Catalysts for an AI Market Correction

Although the long-term outlook for artificial intelligence remains constructive, investors should closely monitor several developments that could materially alter market sentiment.

1. Capital Expenditure Stops Generating Economic Returns

The first and perhaps most important question concerns capital allocation.

Current investment levels are unprecedented.

They remain sustainable only if corresponding revenues continue expanding.

Several indicators deserve close attention.

First, investors should monitor capital expenditure relative to operating cash flow.

Companies whose investment increasingly exceeds internally generated cash become progressively more dependent upon optimistic future assumptions.

Second, cloud revenues, Remaining Performance Obligations (RPO), enterprise AI subscriptions, and recurring AI-related income should continue growing alongside infrastructure spending.

Third, utilization rates across GPUs, networking infrastructure, electricity generation, and hyperscale data centers should remain healthy.

Infrastructure that sits idle eventually becomes a financial burden rather than a competitive advantage.

Oracle already illustrates this tension.

Its capital expenditure relative to operating cash flow has risen dramatically, placing increasing pressure upon future earnings.

If investment continues rising while utilization and revenues begin slowing, markets may eventually question whether the AI infrastructure buildout has become excessive.

2. Scaling Laws Begin to Produce Diminishing Returns

Although Scaling Laws continue supporting aggressive investment, investors should remember that no empirical relationship necessarily extends forever.

Larger models eventually confront practical constraints.

Electricity becomes more expensive.

Training data becomes scarcer.

Semiconductor manufacturing encounters physical limitations.

Memory bandwidth and networking introduce new bottlenecks.

Training costs increase exponentially.

At some point, each additional dollar invested may produce progressively smaller improvements in model capability.

That does not imply innovation will stop.

Rather, future progress may increasingly depend upon algorithmic efficiency, model distillation, inference optimization, specialized architectures, and software innovation instead of brute-force computing power alone.

Investors should therefore monitor not only larger models, but also cheaper intelligence.

The companies reducing the cost of intelligence may ultimately become as valuable as those expanding its capability.

3. Enterprise Adoption Slows

Corporate surveys remain encouraging.

Most large enterprises continue planning additional AI investment despite uncertain short-term returns.

This behavior reflects a familiar strategic dilemma.

Few executives wish to explain to shareholders why competitors embraced AI while they delayed.

Fear of missing out continues influencing boardroom decisions almost as much as investment committee decisions.

However, enthusiasm cannot substitute indefinitely for measurable productivity gains.

If corporations begin postponing deployments, reducing budgets, or delaying enterprise implementation because returns remain elusive, market expectations could adjust rapidly.

Fortunately, current evidence suggests the opposite.

Most enterprises continue expanding AI budgets despite acknowledging that precise return-on-investment calculations remain difficult.

For now, adoption momentum remains intact.

4. Governments Tighten Regulation Around Frontier AI

Another important risk stems from public policy.

As frontier models become increasingly capable, governments may become less concerned with promoting innovation and more focused on controlling potential societal risks.

If future systems approach Artificial General Intelligence (AGI), concerns surrounding national security, misinformation, cyber capabilities, autonomous weapons, or uncontrolled self-improving systems could encourage coordinated international regulation.

Some leading AI researchers—including Elon Musk, Demis Hassabis, and Sam Altman—have publicly argued that AGI may emerge before the end of this decade.

Whether such forecasts prove accurate remains uncertain.

Nevertheless, even a modest probability of highly capable autonomous systems increases the likelihood of future regulatory intervention.

Current frontier models remain well short of fully autonomous AGI.

Yet investors should recognize that regulatory risk will likely increase alongside model capability.

5. Liquidity Conditions Become Less Supportive

Finally, macroeconomic conditions continue mattering enormously.

Technology valuations remain particularly sensitive to real interest rates.

Persistent inflation driven by energy prices, sustained fiscal expansion, or exceptionally large capital expenditure cycles could encourage tighter monetary policy.

Higher real interest rates reduce the present value of long-duration growth assets.

At the same time, crowded investor positioning increases vulnerability to abrupt corrections.

Technology rallies often end not because narratives suddenly become false, but because liquidity temporarily disappears.

Markets built upon optimism can reverse surprisingly quickly when investors simultaneously seek to reduce exposure.

The larger the consensus, the more violent the unwind can become.

V. Investment Strategy: Building a Portfolio for an AI-Driven World

Given both the extraordinary opportunity and the growing risks, YCC Capital believes investors should avoid positioning portfolios at the middle of the risk spectrum.

Instead, we recommend a barbell strategy.

The objective is straightforward:

Protect capital if markets correct sharply while maintaining meaningful exposure to the technologies most likely to create long-term wealth.

Defensive Allocation (Approximately 40–60%)

The defensive side of the portfolio should prioritize liquidity and resilience.

Short-duration government bonds, Treasury bills, and high-quality money market funds provide stable income while preserving the flexibility to deploy capital during periods of market stress.

Cash is often criticized for producing low returns.

During major corrections, however, liquidity becomes an option with significant value.

Investors holding cash when others become forced sellers possess opportunities unavailable to fully invested portfolios.

Growth Allocation (Approximately 40–60%)

The growth allocation should remain highly concentrated.

Rather than attempting to own every company associated with artificial intelligence, investors should focus upon businesses occupying indispensable positions within the global AI value chain.

Preferred areas include:

- Semiconductor manufacturing equipment

- Advanced domestic semiconductor designers

- High-bandwidth memory and storage technologies

- Printed circuit boards (PCB)

- Optical communication modules

- Liquid cooling infrastructure

- Advanced semiconductor packaging

- Leading frontier large language model developers

- Critical AI infrastructure providers

These businesses benefit from structural demand regardless of which individual AI applications ultimately dominate.

Much like the suppliers of steel, electricity, or cloud infrastructure during previous technological revolutions, they represent foundational rather than speculative components of the ecosystem.

Avoid the “Middle Ground”

One of the defining characteristics of a successful barbell strategy is deliberately avoiding mediocre opportunities.

In today’s AI market, this means remaining cautious toward businesses merely attaching AI branding to legacy products without possessing meaningful technological advantages.

Similarly, mature technology companies lacking exposure to AI while offering limited growth may continue losing investor attention as capital concentrates around higher-conviction opportunities.

During periods of structural technological transformation, markets often become increasingly unforgiving toward companies lacking clear strategic relevance.

Market Volatility Should Be Viewed as Opportunity

Periods of sharp market weakness should not automatically be interpreted as evidence that the AI thesis has failed.

Disappointing quarterly earnings, temporary demand fluctuations, new equity issuance, or liquidity-driven corrections may produce substantial drawdowns even within fundamentally strong businesses.

Investors prepared with liquidity can often use such periods to increase exposure at significantly more attractive valuations.

The objective of the barbell strategy is therefore not to eliminate volatility.

It is to survive volatility while preserving the ability to exploit it.

VI. Principal Investment Risks

Investors should continue monitoring several key risks:

- AI capital expenditure generates lower-than-expected economic returns.

- Frontier model capabilities improve more slowly than anticipated.

- Commercial monetization of AI applications disappoints.

- China’s domestic semiconductor and computing ecosystem develops more slowly than expected.

- Rising U.S. real interest rates compress valuation multiples across growth assets.

- Crowded investor positioning amplifies market volatility.

- Governments impose stricter regulations on frontier AI development and deployment.

YCC Closing Perspective

Artificial intelligence increasingly resembles electricity rather than software.

Electricity transformed every industry without every electric company becoming a successful investment.

AI is likely to follow a similar path.

The technology itself appears destined to reshape the global economy. Yet only a relatively small group of companies will ultimately capture disproportionate economic value.

The challenge for investors is therefore becoming more selective, more disciplined, and more patient—not less optimistic.

The next decade may well produce extraordinary wealth creation.

History suggests it will also produce extraordinary volatility.

Successful investors will need to be prepared for both.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice.

Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein.

This report is based upon publicly available information and data believed to be reliable. However, YCC Capital makes no representation or warranty, express or implied, regarding the accuracy, completeness, reliability, or timeliness of such information. Forward-looking statements contained herein involve risks, uncertainties, assumptions, and other factors that could cause actual outcomes to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult their own financial, legal, accounting, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any direct or indirect loss arising from the use of, or reliance upon, this publication or any information contained herein.

This report is intended solely for informational purposes and may not be reproduced, redistributed, published, or transmitted for commercial purposes without the prior written consent of YCC Capital.

© 2026 YCC Capital. All rights reserved.

YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy focused on identifying capital-flow-driven mispricings and asymmetric hedging opportunities across global markets. The Fund is registered in the State of Delaware, United States, and is structured as a Rule 506(c) investment vehicle. Where referenced, performance data has been independently verified by third-party administrators, including NAV Consulting; however, individual investor performance may differ depending on subscription timing and investment circumstances.

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For complimentary daily macro research, investment strategy notes, and market intelligence, visit:

Join our free daily newsletter for institutional-quality analysis covering global macroeconomics, artificial intelligence, geopolitics, equities, fixed income, commodities, currencies, and long-term investment themes.

Final YCC Perspective

The AI revolution will almost certainly create both extraordinary fortunes and spectacular disappointments.

History rarely rewards investors simply for recognizing that a revolutionary technology exists. Instead, it rewards those who correctly identify where durable economic value ultimately accumulates. Railroads transformed commerce, but many railway companies failed. The Internet changed civilization, yet most dot-com stocks disappeared. Artificial intelligence will likely follow the same pattern.

Today’s market is pricing not only faster earnings growth, but also a profound reorganization of the global economy. That makes elevated valuations understandable—but it also leaves little room for execution mistakes.

Looking ahead, we remain constructive but increasingly selective. The United States continues to hold meaningful advantages in frontier AI research, software ecosystems, hyperscale cloud infrastructure, and semiconductor design. These strengths should allow U.S. technology leadership to remain resilient, even as competition intensifies.

By contrast, China’s AI ambitions continue to face meaningful structural headwinds. Export controls on advanced semiconductors, demographic pressures, weak private-sector confidence, property market fragility, and increasing geopolitical fragmentation are likely to constrain China’s ability to fully replicate the depth of the U.S. AI ecosystem. While China’s domestic AI supply chain may continue benefiting from import substitution and policy support, investors should distinguish carefully between policy-driven optimism and sustainable commercial competitiveness.

Ultimately, the defining investment opportunity of the coming decade will not be owning every company associated with artificial intelligence. It will be identifying the businesses that become indispensable infrastructure for the global digital economy—those whose technologies remain essential regardless of which applications ultimately prevail.

Markets may continue oscillating between exuberance and anxiety. Innovation, however, rarely follows a straight line.

For disciplined long-term investors, periods of volatility should be viewed less as reasons for retreat than as opportunities to accumulate ownership in the highest-quality AI franchises at more attractive valuations.

The AI age has not ended.

If anything, it has only just begun.