YCC CAPITAL

Emerging Markets & China Strategy

June 25, 2026

Executive Summary

China’s January–May 2026 fiscal data reveal a government sector undergoing an important transition. After front-loading support earlier in the year, fiscal authorities appear to be moving into a temporary consolidation phase before a likely reacceleration in the second half.

The key message is straightforward: fiscal revenues are recovering faster than expenditures. Government income has stabilized on the back of stronger industrial profitability, firmer producer prices, and more active capital markets. Meanwhile, spending growth has slowed considerably, suggesting policymakers are preserving ammunition for deployment later in the year.

This pattern resembles a household that has already purchased the materials for a major renovation project but has not yet fully begun construction. The cash is available, the plans are largely approved, but the labor and execution phase has been deferred.

For investors, the most important implication is that China’s fiscal impulse has not disappeared. Rather, it appears to have shifted into a later timetable. The combination of ultra-long special treasury bond issuance, special local government bond deployment, and policy-bank financing suggests fiscal support could strengthen during the third quarter.

At the same time, structural constraints remain significant. Persistent weakness in land sales revenues continues to weigh on local government finances, highlighting the ongoing challenges facing China’s property sector and local fiscal architecture.

From YCC Capital’s perspective, the data reinforce a broader theme: China continues to rely increasingly on state-led investment and fiscal engineering to offset structural weakness in private-sector demand and real estate. While cyclical stabilization is achievable, durable growth remains constrained by deeper balance-sheet pressures within households, developers, and local governments.

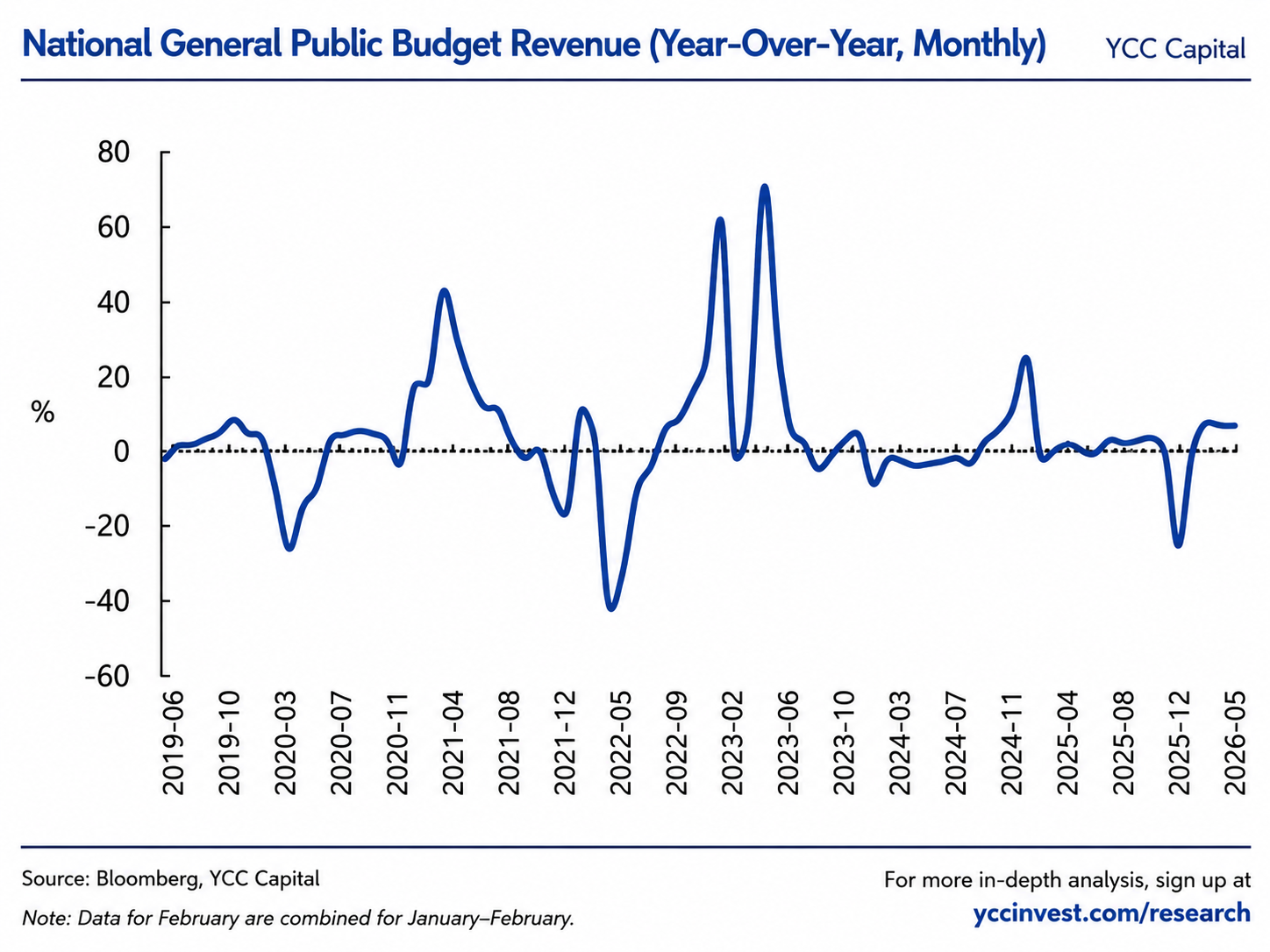

Fiscal Revenue: Signs of Stabilization and Recovery

Broad Fiscal Revenue Continues to Improve

During January–May 2026, national general public budget revenue reached RMB 1.005 trillion, representing year-over-year growth of 4.0%.

This marked an improvement from the January–April pace and signals a gradual recovery in government income generation.

May alone generated fiscal revenue growth of 6.6% year-over-year, demonstrating continued momentum.

Several factors supported this improvement:

- Better industrial profitability

- Higher producer price inflation

- Stronger manufacturing activity

- Increased activity in financial markets

- Improved tax collection dynamics

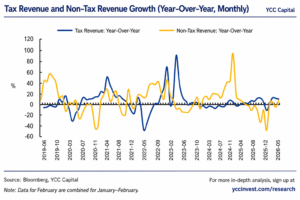

Combined tax and non-tax revenues are now contributing to fiscal recovery, a notable improvement from earlier periods when tax receipts carried most of the burden.

Tax Revenue Recovery Broadens

Tax revenue totaled RMB 826.2 billion during the first five months of the year, increasing 4.4% year-over-year.

The composition of this improvement offers valuable insight into the state of the economy.

Value-Added Tax Remains Supportive

Domestic VAT rose 6.2% year-over-year during January–May.

In May alone, VAT increased 7.9%.

Because VAT is closely tied to production and sales activity, the improvement suggests manufacturing conditions remain relatively resilient despite ongoing weakness in parts of the domestic economy.

Producer prices also provided support. Higher industrial prices help expand taxable revenue bases even when real economic activity remains only moderately strong.

Consumption Taxes Reflect Softer Consumer Demand

Not all areas were equally positive.

Domestic consumption tax revenue declined 3.1% year-over-year during the first five months.

May consumption tax receipts fell 2.0% after previously recording positive growth.

This slowdown is consistent with softer discretionary spending patterns, particularly in automobiles and consumer durables.

The data reinforce a recurring theme in China’s economy: manufacturing activity has often outperformed household consumption, creating an increasingly unbalanced growth profile.

Financial Markets Become an Important Revenue Source

One of the strongest components of fiscal revenue came from capital markets.

Stamp tax revenue increased 35.8% year-over-year.

Even more striking, securities transaction stamp tax revenue surged 88.8% cumulatively and 145.9% in May alone.

For fiscal authorities, active equity markets have become an increasingly important supplementary source of revenue.

This dynamic illustrates an important feature of China’s policy framework. Healthy financial market activity not only supports investor confidence but also directly contributes to government revenue generation.

Property-Related Taxes Remain Weak

Despite some marginal improvement, real-estate-related taxes continue to reflect significant underlying weakness.

During January–May:

- Deed tax revenue declined 14.8%

- Land value-added tax revenue declined 14.2%

Although the pace of decline narrowed compared with previous months, the property sector remains a substantial drag on fiscal conditions.

This is particularly important because land transactions have historically served as one of the most important funding channels for local governments.

The gradual stabilization observed in recent months should not be mistaken for a recovery. Rather, it appears more consistent with a bottoming process characterized by low transaction volumes and cautious market sentiment.

Corporate Profitability Shows Improvement

One encouraging development emerged from corporate income taxes.

Corporate income tax revenue turned positive on a cumulative basis for the first time this year, rising 0.2%.

Monthly growth reached 3.3%.

This improvement likely reflects:

- Stronger upstream commodity pricing

- Better profitability among advanced manufacturing industries

- Improved prepayments associated with recovering industrial profits

However, the recovery remains uneven.

Profit growth continues to be concentrated in select industries, while many traditional sectors face ongoing margin pressure.

As a result, the sustainability of corporate tax improvement remains uncertain.

Fiscal Expenditures: Deliberate Pause Before Potential Reacceleration

Spending Growth Slows Significantly

On the expenditure side, the picture differs considerably.

National general public budget expenditures reached RMB 1.139 trillion during January–May, increasing only 0.8% year-over-year.

This represented a further slowdown from earlier months.

In May alone, spending fell 1.6% year-over-year, marking a second consecutive monthly contraction.

The data suggest policymakers deliberately moderated fiscal deployment after strong first-quarter activity.

Rather than continuously accelerating spending, authorities appear to be smoothing fiscal support over the course of the year.

Central Government Supports Growth While Local Governments Lag

The divergence between central and local government spending remains striking.

In May:

- Central government expenditures rose 11.3%

- Local government expenditures fell 4.4%

This gap reflects a broader structural reality.

While Beijing maintains considerable fiscal flexibility, local governments remain constrained by:

- Weak land sales

- Elevated debt burdens

- Reduced financing capacity

- Slower property market activity

The result is an increasingly centralized fiscal system in which the national government assumes a larger role in stabilization efforts.

Spending Priorities Favor Technology and Social Welfare

Despite overall spending moderation, resource allocation remains targeted.

May spending growth included:

- Science and technology expenditures: +13.0%

- Healthcare expenditures: +10.7%

- Social security and employment expenditures: +1.3%

These priorities align closely with Beijing’s long-term strategic objectives.

The government continues directing resources toward technological self-sufficiency, industrial upgrading, and social stability.

For global investors, this trend reinforces the importance of distinguishing between favored strategic sectors and areas facing policy headwinds.

Infrastructure Spending Remains Soft

Infrastructure-related spending remained notably weak.

May expenditures declined across several categories:

- Agriculture, forestry, and water affairs: -15.7%

- Environmental protection: -19.1%

- Urban and community affairs: -9.7%

- Transportation: -5.0%

Although the pace of decline moderated relative to April, infrastructure investment has yet to regain meaningful momentum.

Part of the weakness appears linked to slower special bond issuance and changing investment priorities.

Government Funds and Land Finance: The Core Structural Constraint

Land Sales Continue to Deteriorate

Perhaps the most important structural issue in China’s fiscal system remains land-related revenue.

Government fund income totaled RMB 125.2 billion during January–May, down 19.2% year-over-year.

More importantly, state-owned land-use rights sales generated only RMB 80.5 billion, representing a sharp decline of 28.7%.

The deterioration accelerated relative to previous months.

In May alone:

- Government fund revenue fell 20.3%

- Land sales revenue fell 35.8%

These figures underscore the continuing weakness of China’s property market.

For years, local governments relied heavily on land sales to finance infrastructure projects, public services, and economic development initiatives.

That model is now under substantial pressure.

At YCC Capital, we continue to view local government fiscal stress as one of the most significant medium-term challenges facing China’s economy.

Government Fund Expenditures Also Weaken

Government fund expenditures declined 4.3% year-over-year during January–May.

Local government fund expenditures fell 6.6%.

Meanwhile, central government fund expenditures increased 67.7% from a low base.

Again, the pattern points toward growing centralization of fiscal support.

The central government is increasingly compensating for weakened local fiscal capacity.

Special Bonds and Future Fiscal Stimulus

One notable development was the sharp slowdown in special local government bond issuance.

New special bond issuance in May totaled approximately RMB 160.8 billion, the lowest monthly level of the year.

This slowdown likely contributed to weaker infrastructure spending.

However, the story may not end there.

Several major funding channels remain available:

- Ultra-long special treasury bonds

- Additional special local government bonds

- Policy-bank financial instruments

- Large-scale strategic infrastructure projects

Recent fiscal deposit data suggest spending momentum may already be beginning to accelerate beneath the surface.

YCC Capital Strategic View

China’s fiscal data present a mixed but revealing picture.

On one hand, revenue recovery is genuine. Industrial activity, capital market turnover, and selective corporate profit improvements are helping stabilize government finances.

On the other hand, the structural challenges remain difficult to ignore.

The property sector continues to undermine local government finances. Land-sale revenues remain deeply depressed. Infrastructure spending has yet to reaccelerate meaningfully. Private-sector demand remains less robust than policymakers would prefer.

The likely path forward is therefore one of continued state-led support rather than self-sustaining private-sector expansion.

We expect fiscal policy to become more supportive during the third quarter as authorities seek to maintain growth momentum ahead of important policy meetings and year-end targets.

Investors should closely monitor:

- July Politburo meeting guidance

- Special bond issuance trends

- Ultra-long treasury bond deployment

- New infrastructure initiatives

- Local government financing conditions

While China may achieve near-term stabilization through policy support, we remain cautious regarding the longer-term growth outlook. The economy continues to face significant structural adjustments tied to demographics, property-market deleveraging, and local government balance-sheet stress.

In contrast, the global investment environment continues to favor markets with stronger private-sector dynamism, healthier household balance sheets, and greater productivity-driven growth potential.

Risk Factors

The outlook could be affected by several risks:

A sharper-than-expected slowdown in domestic demand or external demand could weaken fiscal revenues and growth momentum. Policy implementation may also prove less effective than anticipated. In addition, fiscal transmission mechanisms remain vulnerable to local government financing constraints and continued property market weakness.

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For free daily market insights, macro research, and investment commentary, please visit and subscribe at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com