YCC CAPITAL

Global Strategy

June 26, 2026

Executive Summary

Financial markets often mistake a hawkish central bank meeting for the beginning of an even more aggressive tightening cycle. History, however, suggests that the loudest warnings from policymakers frequently arrive just as the underlying inflation backdrop begins to improve. The Federal Reserve’s June FOMC meeting may prove to be another example.

The Federal Reserve left the federal funds target range unchanged at 3.50%–3.75%, while delivering a notably more hawkish communication than markets had anticipated. The Committee upgraded its inflation projections, revised policy rate expectations higher, and emphasized that restoring price stability remains its overriding priority. Short-term Treasury yields moved higher in response, while longer-dated yields remained comparatively stable, reflecting a market that believes tighter policy today may ultimately restrain future growth.

From our perspective, however, the more important story lies beneath the headlines. Inflationary pressures appear increasingly concentrated in a handful of temporary drivers—notably energy prices and housing costs—both of which show signs of moderating over the medium term. At the same time, structural improvements in productivity, particularly those driven by artificial intelligence, could allow economic output to remain resilient even as labor demand gradually softens.

Much like a storm that appears most intense immediately before the clouds begin to clear, the Fed’s latest hawkish rhetoric may ultimately represent the high-water mark of this tightening narrative rather than the beginning of another prolonged inflation cycle.

Accordingly, YCC Capital believes market expectations for additional monetary tightening may now be approaching their cyclical peak. While inflation risks cannot yet be dismissed—particularly given ongoing geopolitical uncertainty in the Middle East—the balance of evidence increasingly points toward gradually easing price pressures over the next 12 to 18 months.

Overseas Macro Developments

A World Still Navigating Geopolitical Crosscurrents

Global financial markets spent the past week oscillating between optimism and renewed caution as developments in the Middle East continued to shift rapidly.

Early in the week, reports that the United States and Iran had reached a temporary ceasefire understanding, accompanied by an agreement to reopen commercial navigation through the Strait of Hormuz, helped ease investor anxiety. Oil prices retreated meaningfully, risk appetite improved, and global equity markets responded positively.

The improvement proved fragile. By the weekend, Iranian officials again suggested the possibility of closing the Strait of Hormuz, while U.S. officials maintained that commercial shipping remained operational. These conflicting statements underscored an important reality: geopolitical risks have moderated, but they have not disappeared. The current ceasefire remains vulnerable to sudden reversals, leaving energy markets highly sensitive to further developments.

Despite these uncertainties, falling crude oil prices provided sufficient support for risk assets. All three major U.S. equity indices advanced over the week, with the S&P 500 gaining 0.93%, marking its second consecutive weekly increase. Technology stocks once again served as the primary engine of market performance, reinforcing investors’ preference for companies with durable earnings growth and structural exposure to artificial intelligence.

From an investment perspective, this pattern is becoming increasingly familiar. Markets are no longer reacting simply to geopolitical headlines; rather, investors are constantly weighing geopolitical risks against technological innovation and resilient corporate profitability. For now, the latter continues to dominate.

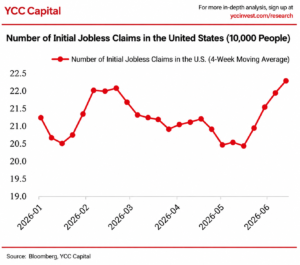

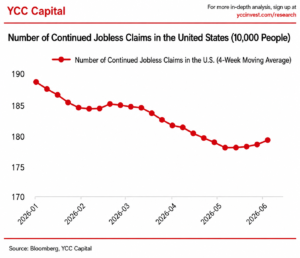

U.S. Labor Market Continues Its Gradual Cooling

Recent economic data suggest that the U.S. labor market is continuing its orderly moderation rather than experiencing a sharp deterioration.

Initial unemployment claims edged modestly higher during the week, while continuing claims also remained elevated relative to earlier in the year. These developments point toward gradually easing labor market tightness, although conditions remain far from recessionary.

This distinction matters.

Labor markets rarely transition directly from strength to weakness overnight. Instead, they typically resemble a slowly turning ship—momentum persists long after the initial change in direction. Current employment indicators continue to suggest that businesses are becoming somewhat more cautious in hiring, but widespread layoffs have yet to emerge.

At YCC Capital, we believe investors should resist interpreting every softer labor market reading as a recession signal. Instead, these data are more consistent with an economy moving toward a healthier balance between labor demand and supply after several years of exceptional tightness.

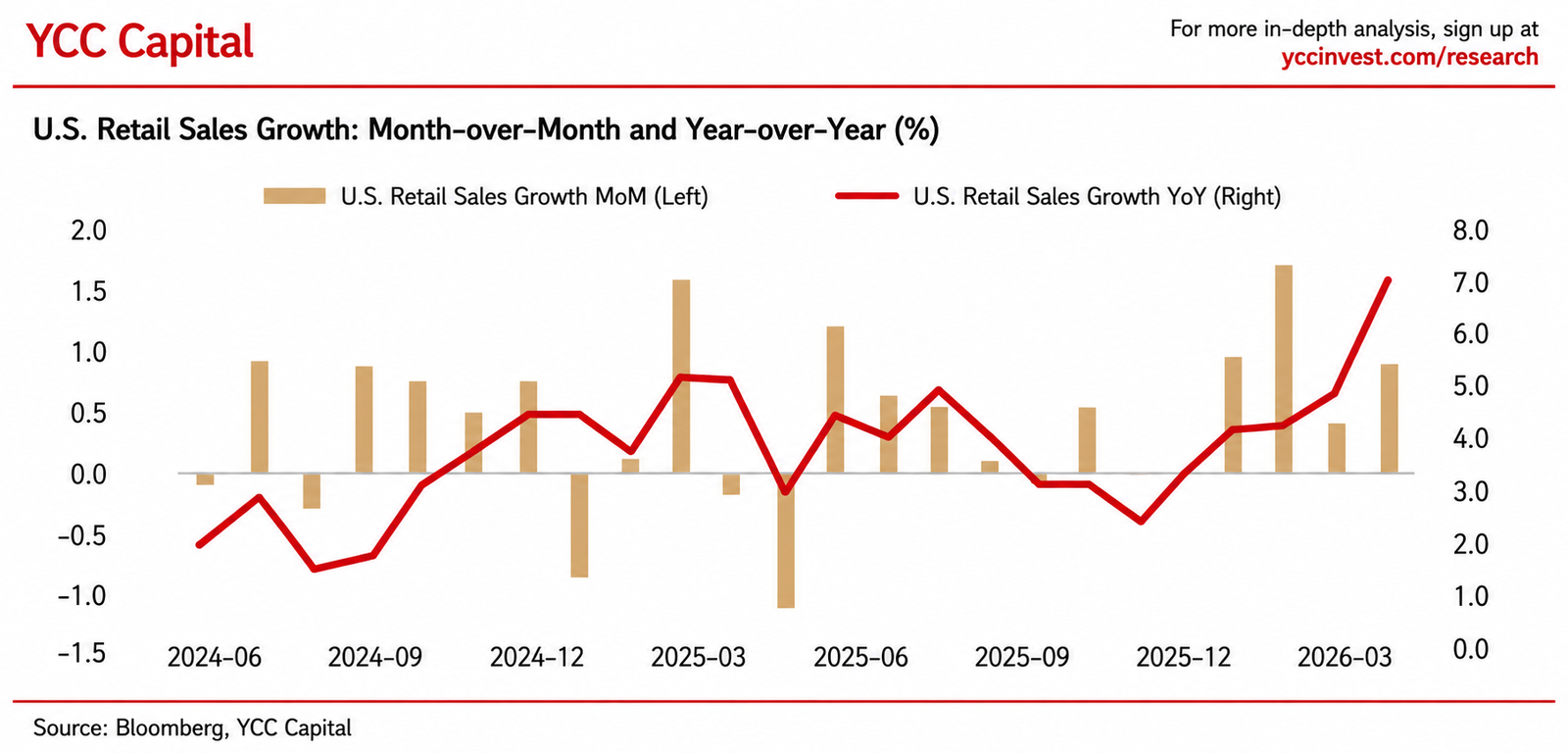

Consumer Spending Remains Remarkably Resilient

While employment has cooled modestly, U.S. households continue to demonstrate surprising resilience.

Retail sales expanded 6.88% year-over-year while increasing 0.88% month-over-month, indicating that consumer demand remains well supported despite elevated borrowing costs.

This resilience reflects several factors.

Household balance sheets remain healthier than during previous tightening cycles, wage growth continues to support disposable income, and many consumers continue to benefit from accumulated savings and rising productivity across key sectors of the economy.

For policymakers, resilient consumption presents both reassurance and frustration.

Strong consumer demand helps sustain economic growth, but it also complicates the Federal Reserve’s efforts to return inflation fully toward its 2% target. As long as spending remains robust, policymakers are unlikely to declare victory over inflation prematurely.

Housing Remains the Economy’s Weakest Link

If one sector clearly illustrates the cumulative effects of higher interest rates, it is housing.

The NAHB/Wells Fargo Housing Market Index declined further to 35 in June 2026, remaining well below the neutral threshold of 50 and signaling continued pessimism among homebuilders.

Unlike consumer spending, residential real estate responds directly to financing costs. Mortgage rates remain elevated by historical standards, limiting affordability and discouraging both buyers and developers from expanding activity.

Yet today’s housing weakness may become tomorrow’s inflation relief.

Housing inflation behaves much like the wake behind a large cargo ship—it continues moving long after the vessel itself has changed direction. Home prices have already softened significantly over the past year, and because rental inflation historically follows changes in house prices with roughly a one-year lag, shelter inflation is likely to continue easing throughout 2027.

This represents one of the strongest structural arguments supporting a gradual decline in underlying U.S. inflation over the medium term.

Japan: Inflation Is Cooling, Reducing Pressure on the Bank of Japan

Japan’s latest inflation data reinforce the view that the country’s price pressures remain relatively well contained despite the gradual normalization of monetary policy.

Headline CPI and core CPI both remained broadly stable during the latest reporting period. More importantly, core inflation excluding both food and energy—the Bank of Japan’s preferred measure of underlying price dynamics—held steady at 1.1% year-over-year, unchanged from the previous month.

This suggests that Japan’s inflation momentum remains fundamentally different from that of the United States.

Whereas U.S. inflation has been driven by a combination of strong consumer demand, elevated shelter costs, and periodic energy shocks, Japan continues to experience a far more measured inflation environment. Wage growth has improved gradually, corporate pricing behavior has become more flexible than in previous decades, yet underlying demand-driven inflation remains moderate.

For the Bank of Japan, these figures provide greater flexibility.

Although the BOJ has begun the long process of normalizing monetary policy after years of ultra-loose settings, the latest inflation data reduce the urgency for further near-term rate hikes. Policymakers can afford to proceed cautiously rather than risk tightening financial conditions prematurely.

From an investment standpoint, this is broadly supportive for Japanese financial assets. A gradual policy normalization allows corporate earnings to continue benefiting from improving domestic demand while avoiding the abrupt tightening cycles that have historically destabilized financial markets.

YCC Capital continues to view Japan as one of the more constructive developed markets over the medium term. While cyclical headwinds remain, they should not be mistaken for structural decline. Corporate governance reforms, healthier inflation dynamics, and steady improvements in shareholder returns continue to support a favorable long-term investment case.

Fed Watch

June FOMC: Hawkish in Tone, Flexible in Framework

The June Federal Open Market Committee meeting represented the first policy meeting chaired by Kevin Warsh, making it an important signal of the Federal Reserve’s evolving policy philosophy.

As widely expected, the Committee voted unanimously (12–0) to maintain the federal funds target range at 3.50%–3.75%.

The decision itself surprised few investors.

The communication surrounding the decision, however, proved considerably more significant.

Compared with previous FOMC statements, the June communiqué was noticeably shorter and omitted much of the explicit forward guidance that had characterized recent meetings. Rather than attempting to pre-commit markets to a future policy path, the Committee focused almost exclusively on its assessment of current economic conditions.

This subtle change may ultimately prove more important than the interest-rate decision itself.

By reducing explicit forward guidance, the Federal Reserve is granting itself greater policy flexibility at a time when inflation, labor markets, and geopolitical risks remain unusually uncertain. Rather than locking itself into predetermined rate paths, policymakers appear increasingly willing to respond meeting by meeting as incoming data evolve.

In our view, this marks an important shift in the Fed’s communication strategy.

Revised Economic Projections Reflect Persistent Inflation Concerns

The updated Summary of Economic Projections reinforced the Committee’s cautious stance.

Relative to the March projections:

- The 2026 real GDP growth forecast was revised down from 2.4% to 2.2%, acknowledging that tighter financial conditions are gradually weighing on economic activity.

- Headline PCE inflation was revised upward from 2.7% to 3.6%.

- Core PCE inflation increased to 3.3%, reflecting stronger-than-expected underlying price pressures.

- The median projection for the year-end federal funds rate rose from 3.4% to 3.8%, implying that policymakers now expect monetary policy to remain restrictive for longer than previously anticipated.

Collectively, these revisions send a clear message: while growth is expected to moderate only modestly, inflation remains the Federal Reserve’s principal concern.

Markets responded accordingly.

Two-year Treasury yields rose noticeably as investors priced in a greater probability that policy rates would remain elevated well into 2027. Longer-dated Treasury yields, however, remained comparatively stable, suggesting that investors continue to believe inflation will eventually return toward target even if near-term policy remains restrictive.

This divergence between the front end and the long end of the Treasury curve is significant. It indicates that markets increasingly distinguish between today’s policy stance and tomorrow’s inflation outlook.

Chair Warsh Places Inflation at the Center of the Conversation

During the post-meeting press conference, Chair Warsh repeatedly emphasized the importance of restoring price stability while devoting comparatively less attention to labor market risks.

The tone of the discussion suggested that inflation remains the Federal Reserve’s primary policy objective despite signs of gradually cooling employment conditions.

Equally noteworthy was Warsh’s announcement of five working groups tasked with reviewing the Federal Reserve’s monetary policy framework.

The review will focus on:

- External communications and policy transparency.

- Balance sheet strategy.

- Data collection and analytical methodologies.

- Productivity and labor market dynamics.

- The long-term inflation framework.

Although these initiatives are administrative rather than immediately policy-relevant, they signal a broader effort to modernize the Federal Reserve’s decision-making process in response to structural economic changes, including technological innovation and evolving labor market dynamics.

YCC Capital View: Peak Hawkishness May Already Be Behind Us

Despite the decidedly hawkish tone of the June meeting, we believe markets should distinguish between policy rhetoric and the underlying inflation trajectory.

Several factors support this conclusion.

First, much of the recent acceleration in inflation reflects temporary energy-related developments associated with geopolitical tensions in the Middle East. Oil prices contributed materially to May’s inflation readings, yet expectations surrounding renewed U.S.–Iran negotiations have already led to renewed declines in crude prices.

Historically, short-lived spikes in oil prices have had only limited and temporary effects on core inflation. Unless energy prices remain elevated for a prolonged period, their contribution to sustained inflation is typically modest.

Second, housing inflation appears increasingly likely to decline over the coming year. U.S. home prices have weakened steadily throughout 2026, and because changes in home prices typically lead rental inflation by approximately twelve months, shelter inflation should continue moderating well into 2027.

Finally, the labor market may face an additional structural headwind that extends beyond the traditional business cycle.

Artificial intelligence is beginning to reshape productivity across a wide range of industries. Unlike previous economic slowdowns, future increases in unemployment may reflect businesses’ ability to produce more output with fewer workers rather than collapsing demand.

If productivity growth continues accelerating, labor demand could soften even while economic output remains relatively resilient.

Taken together, these developments suggest that inflation pressures are likely approaching their cyclical peak even if official inflation data remain elevated in the near term.

For that reason, we believe the June FOMC meeting may ultimately be remembered less as the beginning of another tightening cycle than as the moment when expectations for further tightening reached their highest point.

YCC Strategic View

Looking Beyond the Headlines

Markets have spent much of the past several weeks focusing on whether the Federal Reserve has become more hawkish. In our assessment, this framing misses the more important question.

The issue is not whether policymakers sound hawkish today, but whether the underlying drivers of inflation justify an extended tightening cycle.

At YCC Capital, we believe the evidence increasingly suggests they do not.

The recent rise in inflation has been disproportionately driven by factors that are either cyclical or externally generated. Energy prices remain heavily influenced by geopolitical developments in the Middle East, while shelter inflation continues to lag the sharp slowdown already visible in U.S. housing prices. Neither appears likely to generate a sustained acceleration in core inflation over the medium term.

Meanwhile, economic growth is beginning to moderate in a gradual and orderly fashion. Consumer spending remains healthy, but hiring momentum has slowed. Housing activity remains subdued, and businesses are becoming increasingly focused on productivity gains rather than expanding payrolls.

Taken together, these developments point toward an economy that is decelerating—not contracting.

That distinction is critical for investors.

Soft landings are rarely obvious in real time. They often feel uncomfortable because growth slows before inflation fully retreats, leaving policymakers sounding restrictive even as underlying conditions improve. Investors who focus solely on central bank rhetoric risk overlooking the broader macroeconomic transition already underway.

Portfolio Implications

Fixed Income

The sharp rise in short-term Treasury yields following the June FOMC meeting reflects markets pricing in a higher probability that policy rates will remain restrictive for longer.

However, longer-duration Treasury yields have remained comparatively stable.

This divergence suggests that bond investors increasingly expect inflation to moderate over the medium term despite elevated policy rates today.

If our base case proves correct, duration should become progressively more attractive as inflation continues to ease and markets begin looking beyond the current policy cycle.

Rather than expecting another sustained rise in long-term yields, investors should prepare for a period in which longer-duration government bonds gradually regain their role as effective portfolio diversifiers.

Equities

The resilience of U.S. equities throughout recent geopolitical uncertainty highlights an important feature of the current market cycle.

Corporate earnings—not macro headlines—remain the dominant driver of equity performance.

Technology companies continue benefiting from secular investment in artificial intelligence, cloud infrastructure, semiconductor demand, and enterprise software modernization. These trends are unlikely to reverse simply because monetary policy remains restrictive for several additional quarters.

More broadly, companies capable of improving productivity, maintaining pricing power, and generating robust free cash flow should continue outperforming businesses that rely primarily on cyclical demand.

While market volatility is likely to remain elevated, we continue to favor high-quality businesses with durable competitive advantages rather than highly leveraged or economically sensitive sectors.

Commodities

Oil prices remain the largest near-term macro uncertainty.

The current decline in crude prices reflects improving expectations surrounding Middle East diplomacy rather than a fundamental increase in global supply.

Should geopolitical tensions escalate once again, energy markets would likely experience another sharp but temporary spike.

History suggests, however, that geopolitical oil shocks rarely generate persistent core inflation unless supply disruptions become prolonged.

Consequently, investors should avoid extrapolating short-term energy volatility into long-term inflation expectations.

Gold continues to serve as an effective portfolio hedge against geopolitical shocks and policy uncertainty, although its medium-term performance will increasingly depend on the trajectory of real interest rates rather than oil prices alone.

Foreign Exchange

The U.S. dollar is likely to remain relatively well supported while the Federal Reserve maintains a restrictive policy stance.

However, if inflation gradually moderates and markets begin anticipating eventual policy easing, the dollar’s upside may become increasingly limited.

Currency markets are entering a phase where relative growth differentials and capital flows are likely to matter more than incremental changes in interest-rate expectations alone.

YCC Capital’s Bottom Line

Financial markets often react most strongly when central banks sound the toughest.

Ironically, those moments have frequently marked turning points rather than new beginnings.

We believe the June FOMC meeting fits that pattern.

Although policymakers understandably remain focused on inflation, the underlying economic forces are gradually shifting. Housing inflation is poised to slow, energy-related price pressures appear increasingly temporary, and structural productivity gains from artificial intelligence could soften labor demand without necessarily triggering a recession.

This combination supports our central thesis that market expectations for additional monetary tightening are approaching their cyclical peak.

Investors should therefore remain disciplined rather than reactive.

The coming quarters are likely to be characterized less by accelerating inflation than by a gradual transition toward slower but more sustainable growth, creating opportunities for patient long-term investors willing to look beyond today’s headlines.

Risks

Our constructive medium-term outlook remains subject to several important risks.

The most immediate risk stems from renewed escalation in the Middle East. Any prolonged disruption to global energy supplies—particularly through the Strait of Hormuz—could push crude oil prices materially higher, delaying the expected moderation in inflation and forcing the Federal Reserve to maintain restrictive monetary policy for longer than currently anticipated.

Trade policy also warrants close attention. Additional tariffs or broader supply-chain disruptions could place renewed upward pressure on goods inflation, complicating the disinflation process despite easing housing costs.

Finally, while artificial intelligence is expected to boost productivity over time, the pace and magnitude of its adoption remain uncertain. A slower-than-expected productivity improvement would weaken one of the key structural arguments supporting our view that labor market pressures will ease without triggering a significant deterioration in economic activity.

Accordingly, investors should continue monitoring inflation dynamics, labor market conditions, and geopolitical developments rather than relying on any single indicator.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital.

© 2026 YCC Capital. All rights reserved.

YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S., and structured as a Rule 506(c) fund. Performance data, where referenced, has been verified by independent third parties, including NAV Consulting; however, individual investor results may vary.

Contact Us

YCC Capital Research

For free daily macro insights, market strategy, and institutional research delivered directly to your inbox, sign up at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com