YCC CAPITAL

Geopolitical Strategy

June 24, 2026

Executive Summary

Financial markets are eager to price peace. History suggests that peace is usually much harder to negotiate than a ceasefire.

The latest high-level U.S.–Iran talks in Switzerland represent the most important diplomatic breakthrough since the recent escalation in Middle East tensions. Markets interpreted the meeting as a constructive step toward de-escalation, pushing crude oil prices below recent peaks and easing inflation concerns. Yet investors should be careful not to mistake the opening of negotiations for the conclusion of negotiations.

Our assessment is that the Swiss talks primarily established a mechanism for implementing the previously agreed Memorandum of Understanding (MoU) framework rather than resolving the fundamental disputes at the heart of the conflict. The two sides have created communication channels, established a 60-day negotiating timeline, and reaffirmed commitments to maintain commercial navigation through the Strait of Hormuz during negotiations. However, the most contentious issues—including Iran’s nuclear program, sanctions relief, and the future governance of the Strait of Hormuz—remain unresolved.

The most likely outcome over the next several months is not a comprehensive peace treaty. Rather, it is an extension of the current fragile détente. Both Washington and Tehran have strong incentives to avoid renewed escalation, but neither appears politically positioned to make the concessions required for a permanent settlement.

For energy markets, this means the immediate risk of a catastrophic supply shock has declined. However, structural geopolitical risk remains elevated, suggesting that energy risk premiums are likely to remain embedded in oil markets even if prices continue to retreat from crisis highs.

From a longer-term perspective, one of the most important developments may not be the negotiations themselves but the accelerating search for alternatives to the Strait of Hormuz. The longer the conflict persists, the stronger the incentive for governments and energy producers to build infrastructure that reduces dependence on one of the world’s most strategically sensitive chokepoints.

YCC Perspective

Every global energy crisis eventually becomes a logistics story.

Consumers experience it through gasoline prices. Investors see it through inflation expectations. Governments feel it through strategic vulnerability. But beneath all of those effects lies a simple reality: energy must move from producers to consumers.

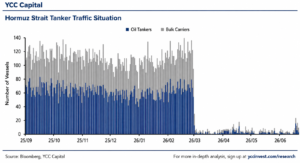

The Strait of Hormuz has long functioned as one of the most critical arteries of the global economy. The recent U.S.–Iran confrontation reminded markets that when a single waterway carries roughly one-fifth of global petroleum consumption, geopolitics and economics become inseparable.

The Swiss talks matter because they reduce the probability of immediate disruption. Yet they do not eliminate the underlying strategic competition that created the crisis in the first place.

A Diplomatic Breakthrough After Months of Escalation

On June 21, 2026, U.S. and Iranian representatives met in Switzerland under the coordination of Pakistan and Qatar. The meeting focused on implementation of the previously negotiated 14-point Memorandum of Understanding that established a preliminary framework for ending hostilities.

After approximately eighteen hours of discussions, mediators released a joint statement outlining the initial achievements of the talks.

Markets responded positively.

Oil prices retreated from recent highs. Inflation expectations eased. Rate-sensitive assets benefited from reduced concerns over a prolonged energy shock. Investors interpreted the talks as evidence that both Washington and Tehran preferred negotiation over escalation.

This reaction was understandable.

The meeting marked the first substantial face-to-face diplomatic engagement between the parties in roughly two months and represented a clear departure from the military-focused dynamic that had dominated recent headlines.

However, market optimism should be viewed in context. The Swiss meeting was less a peace agreement than the creation of a framework designed to make future negotiations possible.

What Was Actually Achieved?

The Swiss talks produced three major institutional outcomes.

First: A Formal Communication Architecture

The parties agreed to establish a high-level committee responsible for supervising negotiations and ensuring continued dialogue on key issues.

In many geopolitical conflicts, communication breakdowns create escalation risks that exceed the underlying policy disagreements. By establishing permanent negotiating channels, both sides reduced the probability of accidental confrontation.

Second: A 60-Day Roadmap

Negotiators agreed to pursue a final agreement within a 60-day window.

The timeline is important because it creates political momentum while also providing markets with a defined period during which both sides are expected to prioritize diplomacy.

Third: Protection of Commercial Shipping

Perhaps most significant for investors, the parties agreed to maintain commercial navigation through the Strait of Hormuz during the negotiation period.

Given the Strait’s central role in global energy transportation, this commitment immediately reduced fears of a near-term supply shock.

Additional statements from both governments reinforced the positive tone.

U.S. officials indicated that Iran had agreed to permit nuclear inspectors access to facilities and continue technical discussions on frozen assets and ceasefire implementation.

Iranian officials emphasized progress toward ending hostilities in Lebanon, obtaining exemptions for energy exports, securing partial asset releases, and initiating economic reconstruction discussions.

The U.S. Treasury subsequently issued a temporary 60-day general license permitting Iranian oil production, delivery, and sales under specific conditions.

Collectively, these measures signal a meaningful reduction in immediate tensions.

Why a Permanent Peace Agreement Remains Difficult

The central challenge is that the negotiations have not yet resolved the issues that matter most.

In effect, the talks addressed process rather than substance.

The largest unresolved issue is the future status of the Strait of Hormuz.

The Memorandum of Understanding states that Iran will engage with Oman and other Gulf states to determine future governance arrangements for the Strait in accordance with international law and the sovereign rights of coastal states.

This language appears constructive but masks a deep legal and geopolitical disagreement.

Iran maintains that its authority derives from principles associated with innocent passage and sovereign security considerations. Tehran argues that it retains the right to intercept vessels deemed threatening to national security.

The United States, by contrast, insists that the Strait operates under the principle of transit passage, a framework that guarantees uninterrupted movement of international commercial shipping.

This disagreement is not merely legal.

It strikes directly at the balance between Iranian sovereignty and the global trading system.

As a result, the Swiss talks temporarily protected navigation but did not establish a durable framework governing the Strait after the 60-day negotiation period expires.

This distinction is critical.

Temporary access is not the same thing as permanent resolution.

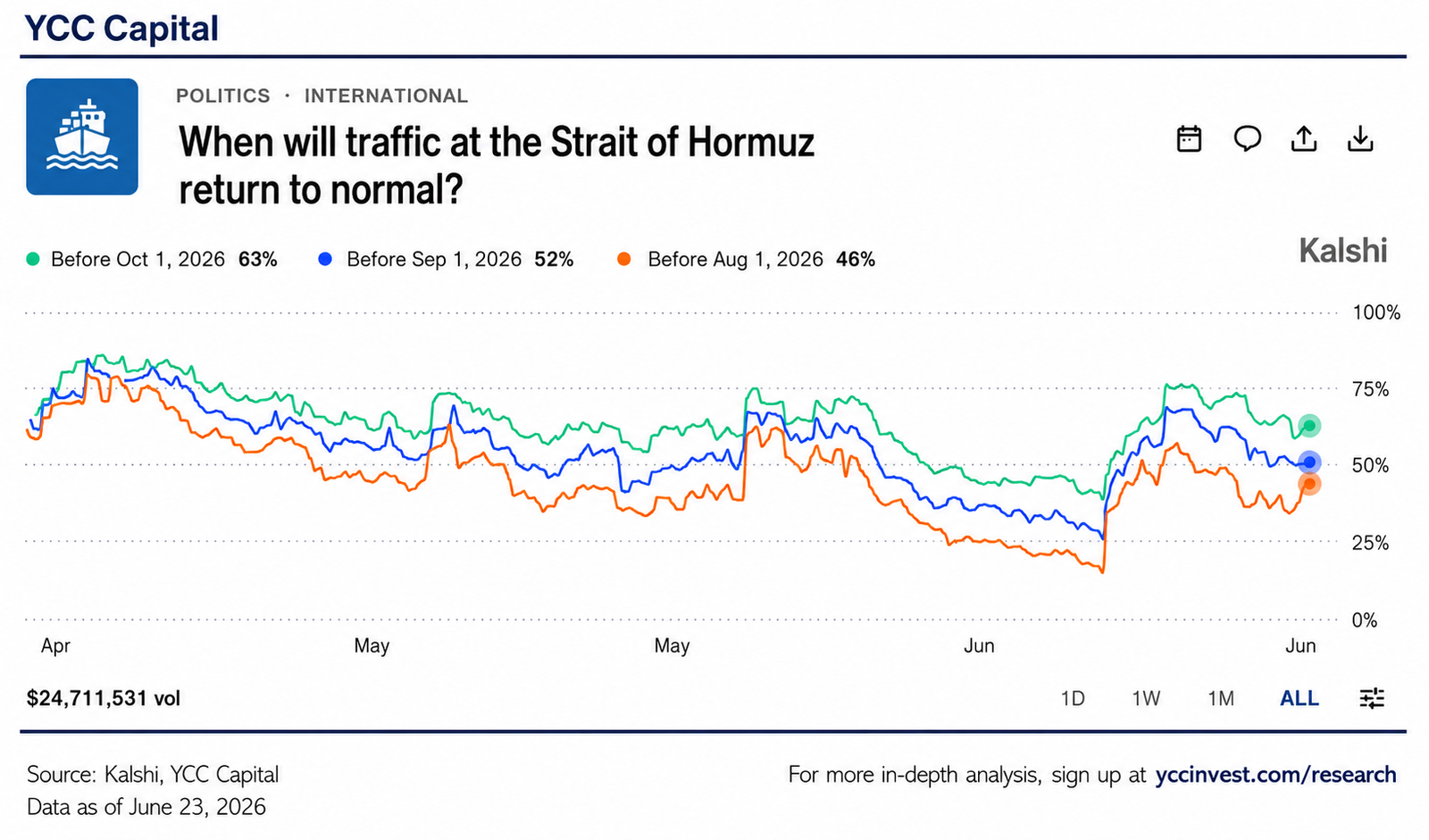

Reading Market Expectations

Prediction markets continue to display skepticism regarding both the normalization of shipping traffic and the likelihood of a rapid final agreement.

Even after the signing of the Memorandum of Understanding, market-implied probabilities suggest investors remain unconvinced that a comprehensive settlement is imminent.

This is notable because financial markets are often highly responsive to diplomatic headlines.

The persistence of skepticism suggests that investors recognize the complexity of the unresolved issues and the long history of failed U.S.–Iran negotiations.

Five Scenarios for the Next Phase

Scenario 1: Comprehensive Peace Agreement (Probability: 5%)

The most optimistic outcome would see Washington and Tehran reach consensus on nuclear issues, sanctions relief, and governance of the Strait of Hormuz.

A permanent peace agreement would be signed, military tensions would dissipate, and shipping activity would likely recover rapidly to pre-conflict levels.

While theoretically possible, current political realities make this scenario unlikely.

Scenario 2: Extended Negotiations and Fragile Stability (Probability: 40%)

This is our base case.

The parties fail to resolve their most important disputes within sixty days but choose not to escalate tensions.

Instead, negotiations are extended, existing arrangements remain in place, and both sides continue pursuing diplomacy.

Under this scenario, the Strait remains open but traffic recovers only gradually.

This outcome reflects the political incentives facing both governments. Washington seeks to avoid an inflationary oil shock, while Tehran seeks economic relief from sanctions and financial pressure.

Neither side currently benefits from renewed conflict.

Scenario 3: Strait Remains Open but Under Iranian Fee-Based Management (Probability: 30%)

Negotiations progress slowly and Iran begins implementing a formal transit-fee structure for commercial shipping.

Countries dependent on Gulf energy supplies negotiate individually with Tehran to preserve access.

Shipping continues but remains below historical levels due to increased costs and operational uncertainty.

Energy markets would likely adapt, but risk premiums would remain elevated.

Scenario 4: Renewed Pressure Through Partial Blockades (Probability: 15%)

Negotiations stall and both parties use the Strait as leverage.

Iran attempts to raise economic pressure through restrictions on navigation while the United States pursues countermeasures designed to limit Iranian financial gains.

Shipping volumes decline sharply and oil prices move materially higher.

Scenario 5: Major Military Escalation (Probability: 10%)

The most adverse outcome involves renewed military confrontation.

Diplomatic channels collapse. Military operations resume. The Strait of Hormuz experiences severe disruption or complete closure.

In this scenario, global energy markets would face a significant supply shock and oil prices could experience a dramatic spike.

The Longer-Term Strategic Question: Will the World Reduce Its Dependence on Hormuz?

One of the most underappreciated consequences of prolonged geopolitical tension is the acceleration of infrastructure investment.

When a family repeatedly experiences traffic jams on the same highway, they eventually search for alternative routes. Nations behave similarly.

The longer the U.S.–Iran confrontation persists, the greater the incentive for governments and energy producers to diversify transportation networks.

The United Arab Emirates has already announced plans to expand alternative export infrastructure capable of bypassing the Strait of Hormuz. New pipeline capacity is expected to significantly increase the country’s ability to move crude oil without relying on the waterway.

Additional investments across the Gulf region are likely.

To be clear, no alternative currently threatens the strategic importance of Hormuz. Prior to the conflict, nearly 20 million barrels per day of oil and petroleum products transited the Strait, representing approximately 20% of global petroleum consumption.

Its importance remains immense.

However, even partial diversification could reduce the vulnerability of global energy markets to future disruptions.

That means the long-term upside risk to oil prices from Hormuz-related crises may gradually diminish over time.

Investment Implications

The Swiss talks reduce immediate geopolitical tail risk but do not eliminate structural geopolitical risk.

For investors, several conclusions emerge:

First, the probability of a near-term oil supply shock has declined meaningfully.

Second, oil markets are likely to retain a geopolitical risk premium given unresolved disputes surrounding sanctions, nuclear policy, and maritime governance.

Third, inflation expectations should continue easing if negotiations remain active and shipping volumes gradually recover.

Fourth, longer-term infrastructure investment aimed at bypassing Hormuz could reshape global energy transportation patterns over the coming decade.

Finally, investors should avoid assuming that a ceasefire framework automatically translates into a durable peace settlement. History repeatedly demonstrates that the final stages of conflict resolution are often the most politically difficult.

Strategic Conclusion

The Swiss talks represent a genuine diplomatic achievement.

They reopen communication channels, reduce the risk of immediate escalation, and create a framework for future negotiations. These developments are constructive and should not be dismissed.

Yet the deeper geopolitical realities remain unchanged.

The United States continues to prioritize nuclear non-proliferation and unrestricted maritime commerce. Iran continues to view strategic deterrence and regional influence as core national interests. These objectives remain fundamentally difficult to reconcile.

Accordingly, the most likely path forward is not rapid normalization but a prolonged period of managed instability.

Markets may celebrate the opening of diplomacy. Policymakers still face the harder task of transforming diplomacy into lasting peace.

Sources: Bloomberg, YCC Capital

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For free daily market insights, macro strategy reports, and investment commentary, sign up at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com