YCC CAPITAL

Emerging Markets & China Strategy

────────────────────────────────────────

June 23, 2026

Executive Summary

China’s May 2026 fiscal data tells a familiar story: headline revenues are improving, yet underlying economic momentum remains fragile. Tax receipts strengthened, government revenues exceeded recent seasonal norms, and fiscal income quality improved as a larger share came from taxes rather than administrative or non-tax sources. However, beneath the surface, fiscal spending remained restrained, infrastructure-related expenditures continued to weaken, land-sale revenues deteriorated further, and special-purpose bond issuance lost momentum during the second quarter.

For investors, the key takeaway is that China’s fiscal position is not constrained by a lack of funds as much as by a lack of effective transmission. Fiscal resources exist, but conversion into tangible economic activity remains slow. Much like a reservoir that appears full while irrigation channels remain clogged, capital is accumulating within the system without generating the growth impulse policymakers seek.

From YCC Capital’s perspective, May’s data reinforces a broader theme that has defined China’s post-property-boom era: stabilization is possible, but sustainable acceleration remains elusive. Fiscal authorities are generating better revenues, yet the economy continues to struggle with weak private-sector confidence, sluggish property activity, and insufficient domestic demand.

Sources: Bloomberg, YCC Capital

(Based on China Ministry of Finance data discussed in the underlying report.)

YCC Perspective

Walking through many Chinese cities today reveals a striking contrast. Shopping malls remain crowded on weekends, restaurants are busy during holidays, and stock-market activity has recovered from previous lows. Yet conversations with business owners often tell a different story. Customers are more price-sensitive, investment decisions are postponed, and hiring remains cautious.

China’s fiscal data reflects exactly this contradiction.

Revenue collection has improved because industrial prices have stabilized and financial market activity has picked up. Yet spending, particularly spending that creates new economic activity, remains restrained. Revenue growth alone cannot generate stronger demand if government funds are not reaching projects, households, and businesses at a faster pace.

The result is an economy that appears healthier on paper than it feels on the ground.

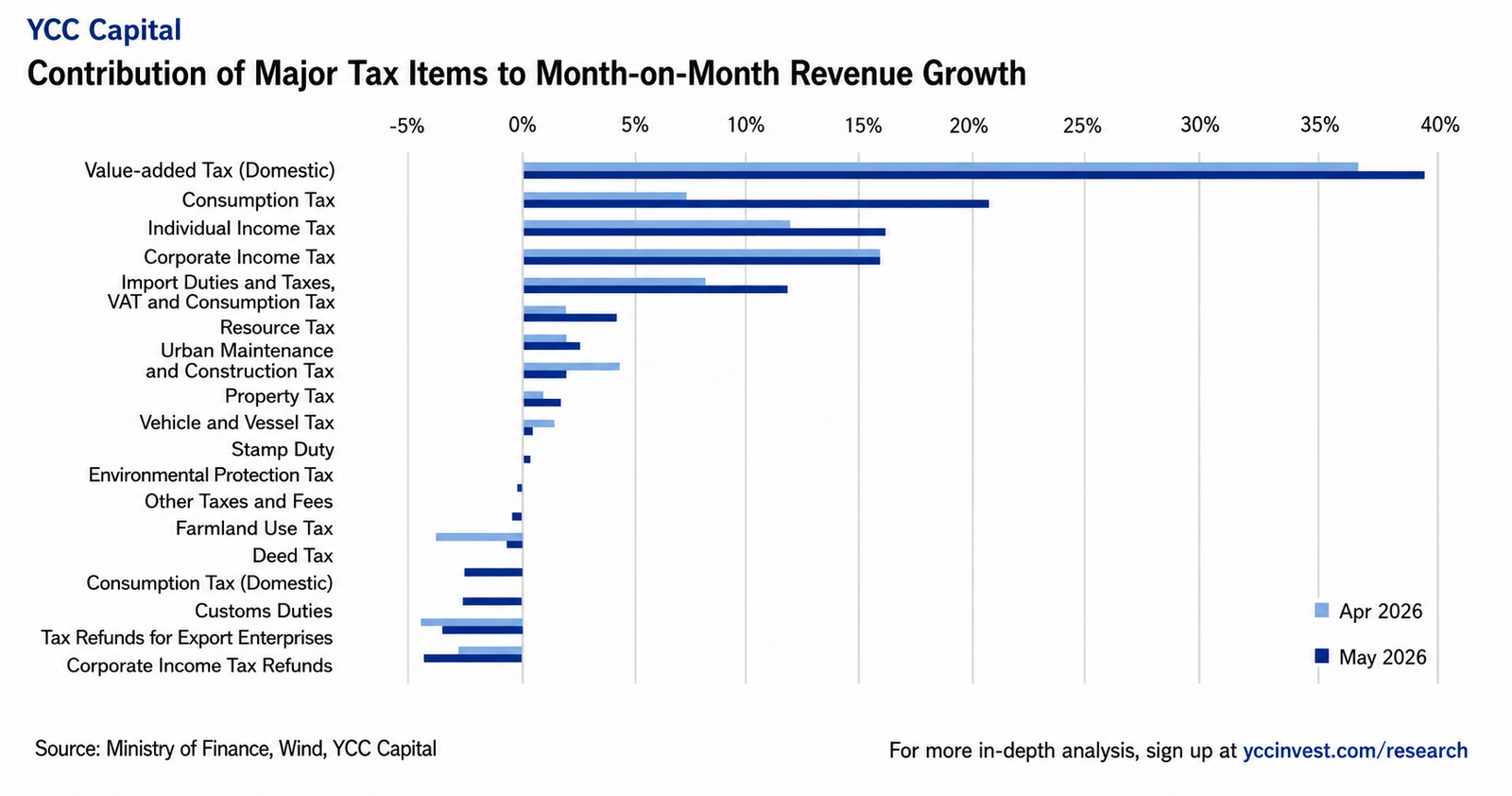

Fiscal Revenue Improves as Tax Quality Strengthens

Revenue Growth Remains Elevated

China’s general public budget revenue increased 6.6% year-over-year in May, remaining near the strongest pace recorded so far this year. During the first five months of 2026, total fiscal revenue rose 4.0% year-over-year, with roughly 45.5% of the annual budget target already completed, a pace ahead of recent years.

Importantly, the composition of revenue improved.

Tax revenues rose 6.8% year-over-year in May, while cumulative tax revenue growth accelerated to 4.4%. Non-tax revenues grew 5.6%, with cumulative growth reaching 2.2%. Compared with the first quarter, a larger proportion of government income originated from traditional tax sources, indicating healthier revenue generation rather than dependence on one-off administrative measures.

This matters because investors often focus solely on headline revenue growth. In reality, the source of revenue is equally important. Tax-driven growth generally reflects genuine economic activity, whereas non-tax revenues can often be temporary or policy-driven.

In May, the “tax content” of fiscal revenue improved meaningfully.

VAT and Financial Market Activity Drive Revenue Gains

Two tax categories were responsible for most of the improvement:

Value-Added Tax (VAT)

Domestic VAT revenue increased 7.9% year-over-year in May, with cumulative growth rising to 6.2%. Improving industrial prices and earlier recovery in manufacturing production supported nominal sales and expanded the tax base.

The improvement is particularly noteworthy because China has spent much of the past several years fighting industrial deflation. Even a modest recovery in upstream commodity and industrial prices can generate significant benefits for fiscal collections.

Stamp Duties

Stamp-duty revenue surged 109.8% year-over-year, while securities transaction stamp duties jumped 145.9%. Cumulative securities-related stamp duty growth reached nearly 89%, reflecting substantially stronger trading activity across China’s equity markets.

The rebound aligns with elevated turnover across the Shanghai and Shenzhen exchanges during May.

For policymakers, stronger stock-market activity serves multiple purposes. It boosts confidence, supports household wealth perceptions, and directly contributes to fiscal revenues.

Consumption Taxes Signal Continuing Weakness

Not all tax categories painted a positive picture.

Consumption-tax revenue declined during May, consistent with weakness in automobile purchases and other large-ticket discretionary spending categories. Retail sales data during the same period similarly suggested that end-user demand remains subdued.

This remains one of the central challenges facing China’s economy.

While industrial production can be supported through policy initiatives and export demand, durable improvement ultimately requires stronger household consumption. The persistence of weak consumption-tax collections suggests Chinese households remain cautious despite numerous policy support measures.

From a macro perspective, consumers continue to save more and spend less than policymakers would prefer.

Spending Remains Restrained Despite Revenue Recovery

Fiscal Expenditure Growth Remains Weak

General public budget expenditures fell 1.6% year-over-year in May, although this represented an improvement from April’s 3.2% decline. Cumulative expenditure growth during January–May slowed to 0.8%, while only 37.95% of the annual spending budget had been executed.

In other words, revenues are running ahead of schedule while spending remains behind schedule.

This divergence is one of the most important messages within the May data release.

Fiscal Pressure Concentrated at the Local Level

The spending slowdown is largely a local-government phenomenon.

Central government expenditures increased 11.3% year-over-year, while local-government spending declined 4.4%.

This distinction matters because local governments are responsible for much of China’s infrastructure investment, public services, and economic implementation.

Over the past decade, local governments served as China’s primary growth engine whenever economic momentum weakened. Today, however, they face significantly tighter financial conditions due to the prolonged property downturn and shrinking land-sale revenues.

As a result, even when Beijing wishes to stimulate growth, implementation increasingly encounters local fiscal constraints.

Social Spending Holds Up While Infrastructure Weakens

Social Expenditures Continue to Provide Support

China continues prioritizing social stability and household welfare.

Combined expenditures on:

- Social security and employment

- Healthcare

- Education

rose approximately 2.4% year-over-year in May. Cumulative growth remained a relatively healthy 4.7%, with social-security spending increasing 6.3% and healthcare spending increasing 11.3%.

These figures reflect Beijing’s increasing emphasis on what policymakers call “investing in people” rather than relying exclusively on large-scale construction projects.

Infrastructure Spending Continues to Contract

The picture is very different for infrastructure-related spending.

Combined expenditures on:

- Agriculture and water resources

- Transportation

- Urban and rural communities

- Energy conservation and environmental protection

declined approximately 12.1% year-over-year in May, while cumulative growth fell to -6.4%.

This weakness helps explain why infrastructure investment data has remained disappointing despite widespread expectations of fiscal stimulus.

For many years, investors assumed China could simply build its way out of economic slowdowns. May’s data suggests that model is becoming increasingly difficult to sustain.

Infrastructure remains important, but fiscal resources are no longer flowing into the sector at the pace seen during previous cycles.

Land Sales Continue to Weigh on Fiscal Capacity

The Property Problem Has Not Gone Away

China’s government-managed fund revenues declined 20.3% year-over-year in May, reflecting continuing stress within the property sector.

The biggest drag remained land-sale revenues.

Local government land-transfer income fell 35.8% year-over-year during May, while cumulative land-sale revenues reached only RMB 804.8 billion, down 28.7% from a year earlier.

For years, land sales functioned as the financial backbone of China’s local-government system. Municipal authorities financed infrastructure, public services, and development projects through proceeds generated from land transactions.

That model is now under sustained pressure.

The continued deterioration in land revenues suggests China’s property correction remains far from complete.

Special Bond Issuance Loses Momentum

Strong First Quarter Followed by Slower Execution

Special-purpose bond issuance began the year aggressively.

During the first quarter, China issued approximately RMB 1.16 trillion of new special-purpose bonds, representing roughly 26.4% of annual issuance plans and exceeding the pace of the previous two years.

However, issuance slowed noticeably during the second quarter.

The moderation reflects more than just financing decisions.

Authorities continue facing challenges including:

- Limited availability of qualified projects

- Delays in capital matching requirements

- Slow fund-disbursement processes

- Administrative bottlenecks affecting project execution

In short, China’s fiscal challenge increasingly involves implementation rather than authorization.

Money can be raised relatively easily. Turning that money into productive economic activity is becoming harder.

What Investors Should Watch in the Second Half

The most important variable for the remainder of 2026 is not revenue collection but spending execution.

The first five months reveal an unusual dynamic:

- Revenue collection is running ahead of recent historical patterns.

- Spending execution is running behind.

- Fiscal balances remain relatively well funded.

- Cash appears available.

- Project conversion remains slow.

This suggests China’s principal fiscal constraint is no longer financing capacity but administrative effectiveness.

If project pipelines improve and disbursement processes accelerate, fiscal spending could strengthen meaningfully during the second half of the year.

However, even if spending picks up, investors should avoid assuming a return to the powerful stimulus cycles that characterized earlier decades. Structural headwinds—including demographic decline, property-sector adjustment, and weak private-sector confidence—remain substantial.

Strategic Conclusions

China’s May fiscal report reinforces three broader macro conclusions:

First, fiscal revenue quality is improving. Tax collections are benefiting from recovering industrial prices and stronger capital-market activity.

Second, fiscal spending remains too cautious to generate a meaningful acceleration in domestic demand. Infrastructure-related expenditures continue to contract despite expectations for stronger policy support.

Third, the property downturn remains the largest structural drag on local-government finances. Weak land-sale revenues continue to constrain China’s broader fiscal system.

At YCC Capital, we continue to view China’s macro outlook as one characterized by stabilization rather than reacceleration. Policymakers possess tools to prevent a sharp downturn, but the evidence remains insufficient to support a sustained growth renaissance.

The second half of 2026 will likely be determined less by Beijing’s willingness to spend and more by its ability to transform available fiscal resources into real economic activity.

Sources: Bloomberg, YCC Capital

Editorial Board

Ken Cao – Chief Strategist, Global Investment Strategy

Le Gao – Managing Analyst

Yui Nabeshima – Strategist

Mai Ikeda – Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

Investor Relations: ir@yccinvest.com

For free daily market insights, macro research, and investment commentary, visit:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com