YCC CAPITAL

Emerging Markets & China Strategy

June 23, 2026

Executive Summary

China’s May economic data painted a picture of an economy becoming increasingly bifurcated. On the surface, headline growth metrics remain respectable, supported by strong exports and resilient industrial production. Beneath that surface, however, domestic demand continues to deteriorate. Investment contracted further, retail sales slipped into negative territory, and the property downturn remains firmly entrenched.

The result is an economy increasingly dependent on external demand and policy-supported industrial activity while household confidence, private-sector investment, and real estate remain significant drags.

From YCC Capital’s perspective, the most important takeaway is not that China is slowing dramatically, but that growth quality continues to weaken. The economy is generating output, yet struggling to generate sustainable domestic demand. Factories remain busy, but consumers remain cautious. Exporters are expanding, while households continue to retrench.

The contrast increasingly resembles a household whose salary is still growing but whose spending keeps shrinking. The income statement looks healthy, but the underlying confidence is fading.

China’s policy makers still possess considerable fiscal and monetary tools. However, unless policies succeed in restoring confidence among households and private businesses, cyclical stimulus alone is unlikely to generate a durable reacceleration.

Key Themes

- Export growth remains exceptionally strong.

- Industrial production is benefiting from external demand and technology sectors.

- Fixed asset investment has deteriorated significantly.

- Consumer spending has turned negative.

- Real estate remains the largest structural drag on growth.

- Additional policy easing is likely if external demand weakens later this year.

Source: Bloomberg, YCC Capital.

The Big Picture: Two Economies Inside One China

The dominant feature of China’s economy today is divergence.

One economy is connected to global trade, advanced manufacturing, artificial intelligence infrastructure, semiconductors, and export-oriented production. This economy continues to perform relatively well.

The other economy consists of households, property developers, local businesses, and private investors. This economy remains under considerable pressure.

May data highlighted this divide more clearly than at any point this year.

Two trends stand out:

1. External Strength vs. Domestic Weakness

Exports accelerated sharply.

Export growth surged from 14.1% in April to 19.4% in May, providing significant support to manufacturing activity and industrial production.

At the same time:

- Fixed asset investment fell further into negative territory.

- Consumer spending contracted.

- Property activity remained deeply depressed.

2. Supply Strength vs. Demand Weakness

Production accelerated while demand weakened.

Factories continued to produce goods at a healthy pace, supported by exports and technology investment. Yet consumers and businesses showed little willingness to spend.

This imbalance has become one of the defining characteristics of China’s post-pandemic economy.

Source: Bloomberg, YCC Capital.

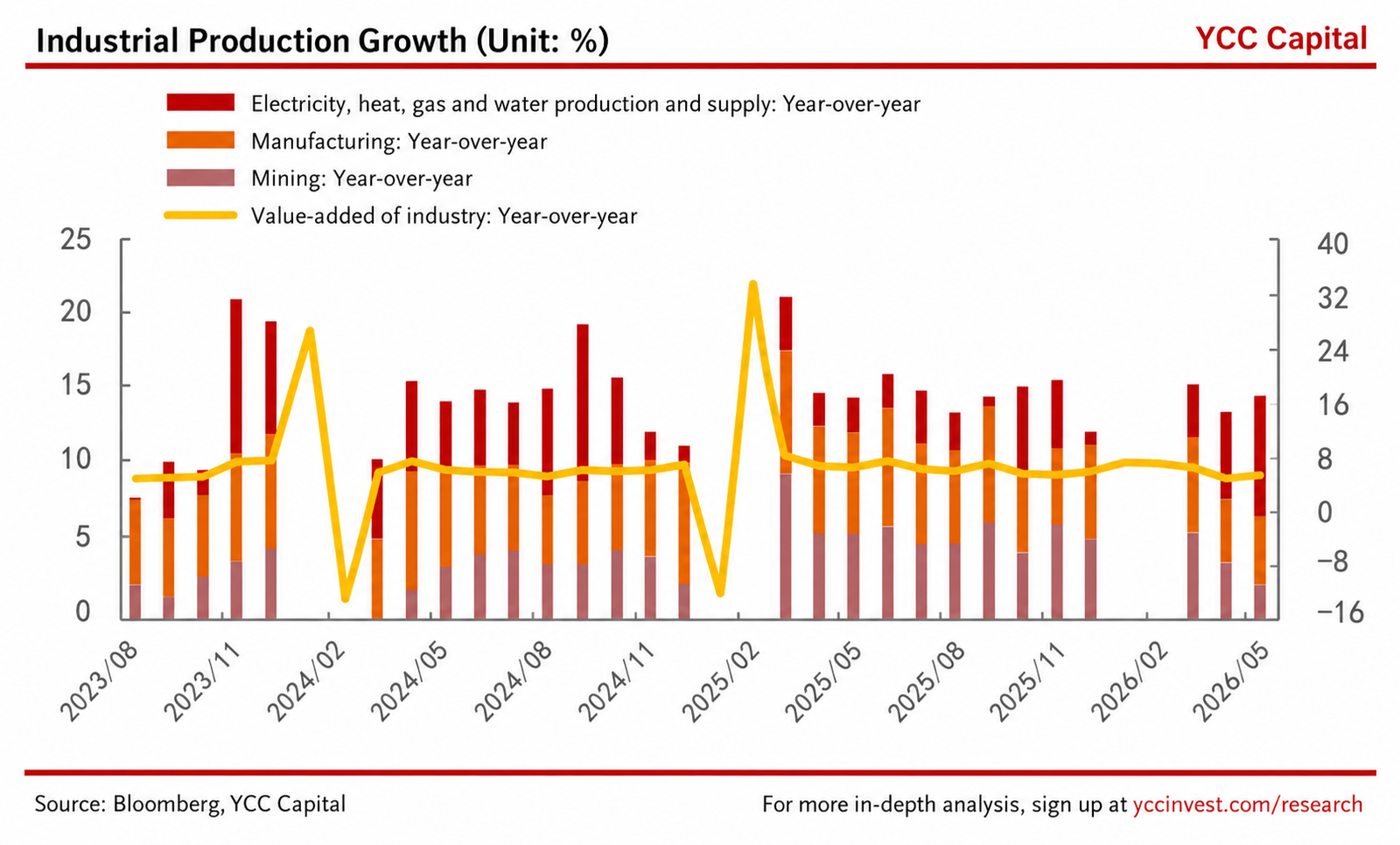

Industrial Production: Exports Continue to Carry the Economy

China’s industrial production rose 4.5% year-over-year in May, exceeding expectations and improving from April’s 4.1%.

While the headline number appears encouraging, the drivers reveal a more nuanced story.

Export Demand Remains the Primary Engine

Industrial export deliveries increased 10.1% year-over-year in May.

This marked the second consecutive month of double-digit growth.

Global demand for Chinese manufactured goods has remained remarkably resilient despite geopolitical tensions and ongoing trade frictions.

For many manufacturers, foreign customers continue to provide stronger demand than domestic buyers.

Technology Manufacturing Accelerates

High-tech manufacturing expanded 15.1% year-over-year, accelerating by 2.3 percentage points from April.

Several factors are contributing:

- Global AI investment spending.

- Rising semiconductor exports.

- Domestic data center construction.

- Continued state support for strategic industries.

China’s technology manufacturing complex remains one of the few areas enjoying simultaneous policy support, strong investment, and robust demand.

Traditional Sectors Remain Mixed

Performance varied across industries:

Stronger sectors

- General equipment manufacturing

- Specialized equipment manufacturing

- Automobile production

Weaker sectors

- Non-metallic minerals

- Certain commodity-processing industries

- Construction-linked sectors

These patterns further reinforce the divergence between newer growth industries and traditional sectors tied to property development.

Source: Bloomberg, YCC Capital.

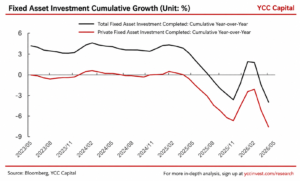

Fixed Asset Investment: A Significant Deterioration

Perhaps the most concerning development in the May data was the continued collapse in investment activity.

Urban fixed asset investment fell 4.1% year-over-year during the first five months of 2026.

This represented a substantial deterioration from the previous reading of -1.6%.

Private-sector investment declined 7.1%.

Private investment often serves as one of the clearest indicators of business confidence. The continued decline suggests firms remain hesitant to commit capital despite government efforts to support growth.

Source: Bloomberg, YCC Capital.

Infrastructure Spending Loses Momentum

Infrastructure investment growth slowed to just 0.6%.

On a monthly basis, infrastructure investment is estimated to have contracted nearly 10%.

Several factors contributed:

- Reduced urgency after a strong first quarter.

- Slower fiscal expenditure growth.

- Lower issuance of local government special bonds.

- Policy makers adopting a more patient stance amid strong exports.

This appears more like a deliberate policy pause than a loss of capacity.

China’s government retains significant control over infrastructure spending. As a result, infrastructure remains one of the most likely channels for future stimulus if growth weakens further.

Looking ahead, YCC Capital expects infrastructure activity to improve during the second half of 2026 as projects associated with national strategic development plans accelerate.

Source: Bloomberg, YCC Capital.

Manufacturing Investment Turns Negative

Manufacturing investment declined 0.4% year-over-year during January-May.

This represents a meaningful shift from positive growth earlier in the year.

Several forces appear to be at work.

Rising Input Costs

Producer prices have accelerated, particularly in upstream commodity sectors.

Higher costs are causing many firms to delay expansion plans and reassess investment budgets.

Capacity Rationalization

Ongoing efforts to address excessive competition and industrial overcapacity are beginning to weigh on investment decisions.

For example, automobile manufacturing investment declined 2.7%.

AI and Technology Remain Bright Spots

Not all manufacturing sectors are weakening.

Investment linked to:

- AI infrastructure

- Semiconductors

- Advanced manufacturing

- Data centers

continues to expand rapidly.

In many respects, China is increasingly becoming a tale of two manufacturing sectors: traditional industries facing profitability pressure and advanced industries benefiting from structural policy support.

Source: Bloomberg, YCC Capital.

Real Estate: The Structural Problem Remains Unsolved

The property market continues to be the single largest drag on China’s economy.

Real estate investment fell 16.2% year-over-year through May.

Monthly investment activity fell approximately 24.4%.

These are not stabilization numbers.

These are recession-level numbers.

Despite repeated policy interventions, China has yet to engineer a sustained recovery in housing demand.

Source: Bloomberg, YCC Capital.

Housing Sales Continue to Fall

Property sales remain weak across both volume and value metrics.

January-May data showed:

- New home sales area down 10.8%.

- New home sales value down 13.5%.

May itself was even weaker:

- Sales area down 13.2%.

- Sales value down 9.3%.

Meanwhile, secondary-home prices across major cities continued to decline.

The brief “spring rebound” observed in several cities earlier this year appears insufficient to alter the broader trend.

A useful analogy is that China’s property market resembles a patient whose fever has fallen slightly but whose underlying illness remains untreated. Temporary stabilization is not the same as recovery.

Source: Bloomberg, YCC Capital.

Why Property Matters So Much

The property sector affects virtually every part of China’s economy:

- Household wealth

- Local government finances

- Construction employment

- Consumer confidence

- Banking system collateral

When housing weakens, spending weakens.

When spending weakens, businesses invest less.

When investment slows, growth weakens further.

This negative feedback loop remains one of the central challenges facing Chinese policy makers.

Until confidence in housing stabilizes, it will be difficult for China to achieve a broad-based domestic recovery.

Source: Bloomberg, YCC Capital.

Consumers Remain Cautious

Retail sales declined 0.6% year-over-year in May.

This represented a notable disappointment and marked a return to contraction.

Consumer demand remains one of the weakest links in China’s recovery.

Source: Bloomberg, YCC Capital.

The Confidence Problem

Several factors are contributing to weak spending:

High Base Effects

Last year’s trade-in subsidy programs boosted purchases of:

- Vehicles

- Home appliances

- Consumer electronics

As those programs fade, comparisons have become more difficult.

Weak Property Market

Consumers tend to spend more when they feel wealthier.

Falling home prices continue to suppress household confidence.

Consumer Sentiment Remains Depressed

Consumer confidence fell to 89.0 in April, the lowest level since the second half of last year.

This may be the most important statistic in the entire report.

Economic recoveries are ultimately psychological events.

When households feel optimistic, they spend.

When they feel uncertain, they save.

China’s consumers continue to choose caution.

Source: Bloomberg, YCC Capital.

What Happens Next?

Economic Outlook

Growth momentum slowed during the second quarter due to:

- Cost pressures.

- Policy timing adjustments.

- Weather disruptions.

- Weak domestic demand.

Nevertheless, several factors could support activity later this year:

- Infrastructure project acceleration.

- Lower global energy prices.

- Continued export resilience.

- Ongoing AI-related investment.

Policy Outlook

For now, policymakers appear comfortable maintaining a relatively stable stance.

Strong exports have reduced pressure for immediate large-scale stimulus.

However, if external demand weakens materially during the second half of 2026, Beijing is likely to respond with:

- Interest rate cuts.

- Reserve requirement ratio reductions.

- Increased government bond issuance.

- Additional fiscal support measures.

Source: Bloomberg, YCC Capital.

YCC Capital Strategic View

China’s economy is not collapsing, but neither is it genuinely reaccelerating.

The current model increasingly relies on exports, industrial policy, and strategic manufacturing investment while domestic demand remains fragile.

This creates several risks.

First, export-led growth leaves China more vulnerable to global demand cycles and geopolitical developments.

Second, weak household confidence limits the effectiveness of traditional stimulus measures.

Third, persistent property weakness continues to undermine private-sector sentiment.

At YCC Capital, we remain cautious on China’s medium-term outlook. While targeted sectors such as AI infrastructure, advanced manufacturing, and strategic technologies may continue to outperform, the broader economy still faces significant structural headwinds.

In contrast, the United States continues to demonstrate stronger household consumption, deeper capital markets, superior productivity dynamics, and greater flexibility in adapting to economic shocks. While U.S. growth is unlikely to be without volatility, the long-term outlook remains comparatively more constructive.

The key question for investors is no longer whether China can produce growth. It clearly can.

The more important question is whether China can restore confidence.

That answer remains elusive.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For complimentary daily market insights, macro research, and investment commentary, visit:

Footer (for every page):

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com