YCC CAPITAL

U.S. Bond Strategy

June 22, 2026

YCC Perspective

Central banking is often compared to steering a large ship: course corrections usually come slowly, and the vessel rarely turns abruptly. The June FOMC meeting suggests the Federal Reserve may be preparing for something different. While markets focused on the decision to leave rates unchanged, the more important development was the shift in communication strategy under newly appointed Fed Chair Kevin Warsh. The message was clear: inflation control has re-emerged as the dominant priority, and investors may need to rethink assumptions that the next move is inevitably lower rates. This analysis is based on the June Federal Reserve meeting review contained in the source report.

Executive Summary

The June 2026 FOMC meeting marked a significant turning point in Federal Reserve communication and policy signaling. While the federal funds rate was left unchanged at 3.50%-3.75%, the meeting delivered a distinctly hawkish message.

Key developments included:

- Removal of virtually all language implying future rate cuts.

- Stronger characterization of labor-market conditions.

- Unanimous support among voting members.

- Hawkish revisions in the dot plot.

- Upward revisions to inflation forecasts.

- Creation of multiple Fed working groups that may reshape communication and operational frameworks.

The meeting represented Chair Kevin Warsh’s first FOMC gathering and may prove more consequential for future policy expectations than the rate decision itself.

The June FOMC Meeting: What Changed?

Policy Rate Left Unchanged

On June 17, the Federal Reserve maintained the federal funds target range at 3.50%-3.75%.

Following three consecutive rate cuts into the end of 2025, the Fed has now left rates unchanged at all four policy meetings in 2026. The decision was fully anticipated by markets, with CME futures pricing nearly a 99% probability of no change prior to the announcement.

The End of the “Automatic Rate-Cut” Narrative

The most notable change was not the rate decision itself, but the language surrounding it.

The April statement had included wording that suggested policymakers were considering the timing and magnitude of further adjustments to rates. Markets interpreted this as meaning the next move would likely be a cut, with uncertainty centered only on timing.

That language was completely removed in June.

This deletion effectively eliminated the Fed’s prior easing bias and represented a meaningful hawkish recalibration.

Labor Market Language Became More Optimistic

The Fed upgraded its assessment of employment conditions.

Previous references to subdued employment growth were replaced with language emphasizing that employment growth remains broadly consistent with labor-force expansion.

Additionally, policymakers highlighted:

- Strong productivity growth.

- Robust capital investment activity.

- Continued labor-market resilience.

These changes reinforce the Fed’s view that the economy remains capable of tolerating restrictive monetary policy.

Unanimous Voting Outcome

The April meeting had produced visible internal disagreement.

Several officials opposed the easing bias embedded in the statement, while others advocated immediate rate cuts.

By contrast, the June meeting resulted in a unanimous 12-0 vote.

The shift suggests that internal consensus has strengthened around maintaining a restrictive stance and prioritizing inflation risks.

Chair Warsh’s First FOMC: A New Operating Philosophy?

Kevin Warsh’s first meeting as Fed Chair delivered a notable stylistic and strategic shift.

The statement itself was substantially shortened and revised. According to Fed watchers, the communication framework was rewritten from beginning to end.

Perhaps most importantly, the revised statement placed overwhelming emphasis on inflation while providing relatively limited discussion of employment concerns.

The Fed continued to acknowledge:

- Elevated inflation.

- Significant uncertainty stemming from Middle East geopolitical tensions.

- Ongoing risks to the economic outlook.

However, the balance of communication clearly shifted toward inflation control.

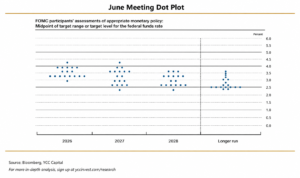

The Dot Plot Turned Decisively Hawkish

The June Summary of Economic Projections revealed a considerably more hawkish outlook than markets had anticipated.

According to the projections:

- Roughly half of Fed officials now expect at least one rate increase during 2026.

- Nine officials projected at least one hike.

- Six projected two or more hikes.

- Only one participant forecast a rate cut.

At the previous projection round, no officials anticipated rate increases.

This represents one of the sharpest hawkish shifts in Fed projections in recent years.

Could the Dot Plot Itself Disappear?

An intriguing development was that Chair Warsh did not submit an individual interest-rate projection.

This omission has sparked speculation that the new Chair may eventually modify or even eliminate the dot plot framework altogether.

If that occurs, markets would lose one of their primary tools for interpreting future Fed intentions, potentially increasing volatility around policy expectations.

Economic Forecasts: Slower Growth, Higher Inflation

The Fed’s updated projections reflected a classic stagflationary tilt.

Officials now expect:

Growth

- Lower GDP growth in 2026.

- Lower GDP growth in subsequent years.

Inflation

- Higher PCE inflation forecasts.

- Higher core PCE inflation forecasts.

- Further upward revisions extending into later years.

The largest revision was to 2026 PCE inflation, which increased by approximately 90 basis points to 3.6%.

Core PCE inflation is projected at approximately 3.3%.

The message is straightforward: inflation is proving more persistent than policymakers expected earlier in the year.

A Quiet but Important Development: Fed Working Groups

Beyond rates and forecasts, another major announcement received relatively little market attention.

The Federal Reserve plans to establish several specialized working groups covering:

- Communication practices.

- Economic data usage.

- Inflation analysis.

- Productivity trends.

- Artificial intelligence and its economic implications.

These initiatives suggest Warsh intends to conduct a broad review of how the Fed communicates and operates.

For investors, the implications may extend well beyond a single policy meeting. The way markets interpret forward guidance itself could change.

Market Reaction: Hawkish Shockwaves

Financial markets responded immediately.

Equities

Following the statement:

- S&P 500 declined sharply.

- Nasdaq fell nearly 1% initially before extending losses.

- Dow Jones Industrial Average weakened materially.

Losses deepened further during Chair Warsh’s press conference.

Treasury Market

Two-year Treasury yields rose dramatically.

The yield moved from below 4.06% before the decision to nearly 4.20% after the press conference.

The move reflected aggressive repricing of future Fed policy expectations.

U.S. Dollar

The dollar index surged above the psychologically important 100 level and continued strengthening throughout the session.

Gold

Gold suffered one of the most immediate reactions.

Spot prices fell sharply after the announcement and extended declines during the press conference, reflecting higher real yields and stronger dollar conditions.

Outlook for the U.S. Economy

Growth Remains Supported by the AI Investment Boom

The report argues that large-scale AI-related capital expenditure continues to support U.S. economic activity.

Productivity gains, infrastructure investment, semiconductor spending, and digital-capital deployment remain major growth drivers.

Much like railroad construction in the 19th century or internet infrastructure spending in the late 1990s, AI investment has become a central pillar supporting corporate earnings and economic momentum.

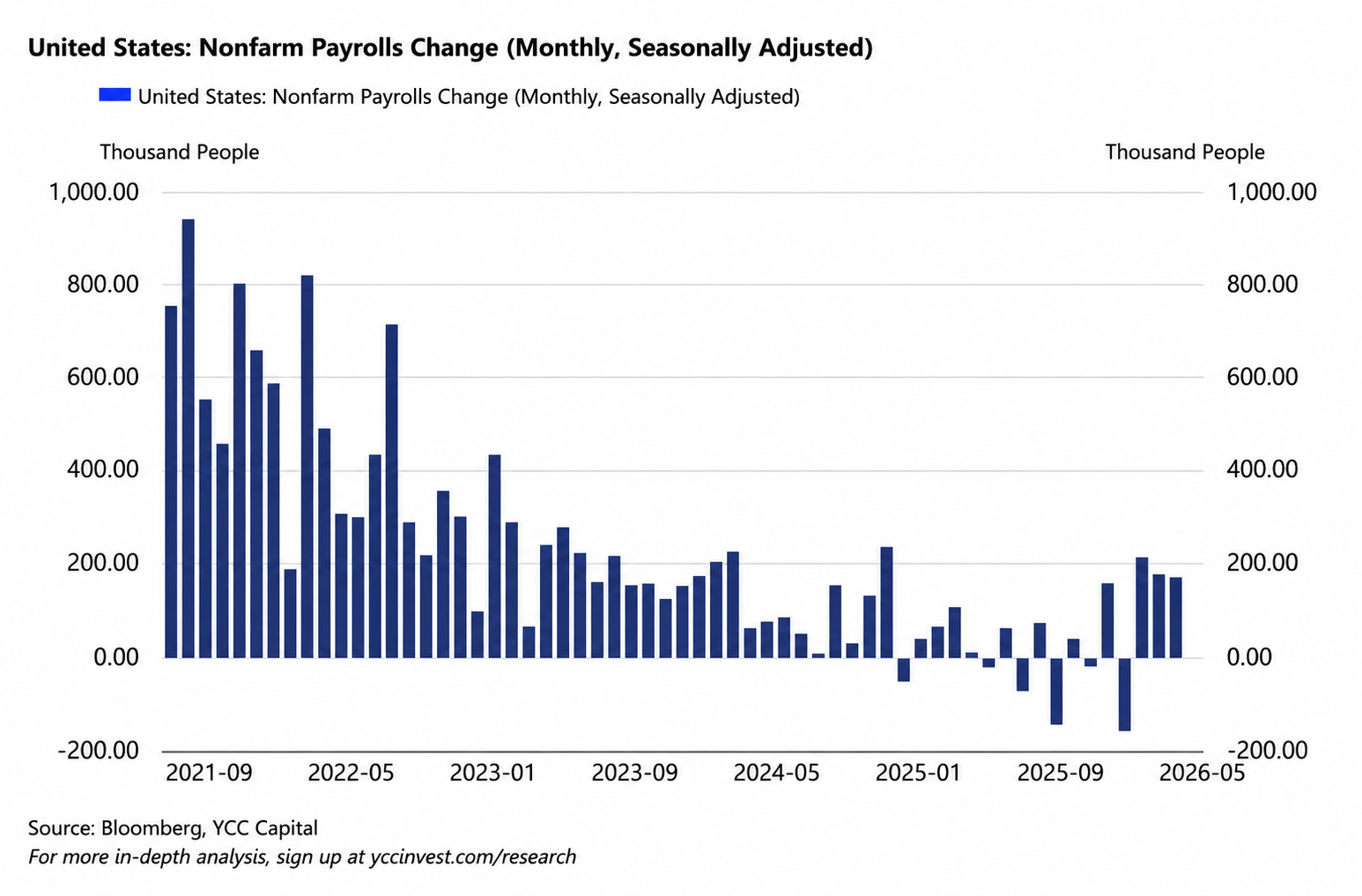

Labor Market Remains Resilient

Recent employment data continue to surprise positively.

May nonfarm payrolls increased by approximately 172,000, significantly exceeding expectations.

The unemployment rate remained at 4.3%.

These figures reinforce the Fed’s assessment that labor-market conditions remain healthy despite restrictive monetary policy.

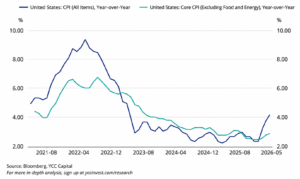

Inflation Pressures Are Reaccelerating

Recent inflation indicators have shown renewed upward momentum.

Key measures cited in the report include:

- CPI inflation rising to approximately 4.2%.

- Core CPI remaining elevated.

- Core PCE reaching its highest level since late 2023.

- PCE inflation continuing to exceed the Fed’s target.

Energy-related pressures and geopolitical disruptions have contributed to the rebound.

YCC Capital Strategic Outlook

U.S. Equities

The AI spending cycle remains a powerful support for earnings and equity valuations.

However, markets increasingly resemble a crowded theater with multiple exits but only one narrative. As long as AI investment remains unquestioned, valuations can remain elevated. If confidence in the durability of AI-related spending weakens, downside risks could emerge quickly.

We remain cautiously constructive on long-term U.S. equities while recognizing elevated valuation risk.

U.S. Treasuries

The Fed’s communication shift supports higher short-end yields.

Longer-duration yields may face competing forces:

- Persistent inflation.

- Slower growth expectations.

- Geopolitical uncertainty.

Yield curves could remain volatile as markets reassess the probability of future tightening.

Gold and Precious Metals

The structural case for gold remains intact.

De-globalization, reserve diversification, and geopolitical fragmentation continue supporting long-term demand.

However, in the near term:

- Elevated real yields.

- Hawkish Fed policy.

- Dollar strength

may limit upside potential and keep precious metals range-bound.

Commodities

Commodity performance remains highly uneven.

AI-linked industrial metals continue to benefit from infrastructure demand.

Meanwhile, China-linked demand remains structurally weaker, reflecting persistent property-sector challenges, subdued domestic confidence, and broader economic headwinds.

Energy markets remain heavily influenced by geopolitical developments.

Chinese Assets

While policymakers continue pursuing stabilization measures, structural pressures remain significant.

Weak household demand, ongoing property-market adjustment, demographic challenges, and fragile private-sector confidence continue to weigh on medium-term growth prospects.

As a result, global investors are likely to remain selective toward China-related exposure.

Conclusion

The June 2026 FOMC meeting may ultimately be remembered less for the unchanged policy rate and more for the emergence of a new Federal Reserve regime.

Chair Warsh’s debut introduced:

- A more hawkish policy bias.

- A stronger focus on inflation.

- A substantial overhaul of communication practices.

- Greater uncertainty regarding future policy signaling tools.

For investors, the key lesson is that the Fed is no longer guiding markets toward eventual easing. Instead, it is signaling a willingness to keep policy restrictive—and potentially tighten further—if inflation remains persistent.

The era of assuming lower rates are always around the corner appears to have ended, at least for now.

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

Sign up for our free daily market insights and research updates at:

Source: Bloomberg, YCC Capital