YCC CAPITAL

Emerging Markets & China Strategy

Date: June 21, 2026

Executive Summary

There are moments in economic cycles when the headline numbers tell only half the story. Walking through a shopping district today in many Chinese cities offers a useful illustration. Factories continue shipping products around the world, ports remain busy, and exporters report solid order books. Yet many households remain cautious, postponing major purchases, reducing leverage, and waiting for greater confidence about the future.

That divergence defines China’s current macro landscape.

May 2026 data showed:

- Manufacturing PMI remained at the expansion-contraction threshold.

- Export growth stayed exceptionally strong.

- Producer prices continued recovering.

- Consumer inflation remained positive but subdued.

- Retail sales disappointed.

- Credit demand from households and businesses remained weak.

- Fixed asset investment continued contracting.

- The property sector remained under pressure despite gradual inventory improvement.

At YCC Capital, we believe the most important takeaway is not that China is falling back into recession. Rather, the economy is navigating a prolonged transition away from a property-led growth model toward a more balanced framework. That adjustment is inherently uneven and takes time.

While 2026 is shaping up to be a better macro year than 2025, the conditions for a powerful V-shaped recovery remain absent.

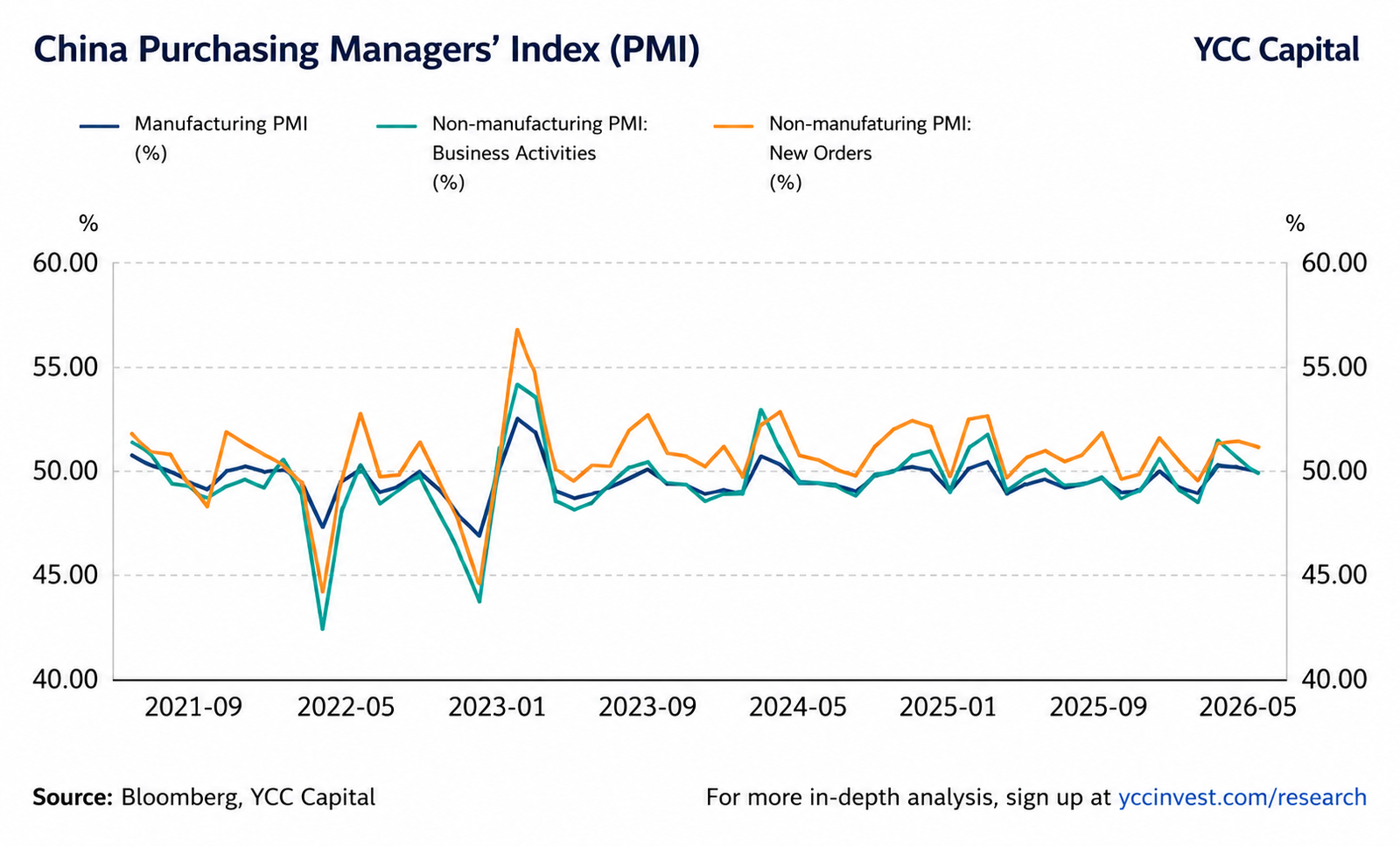

Manufacturing Activity: Stabilization Rather Than Acceleration

PMI Sits Exactly on the Neutral Line

China’s official manufacturing PMI registered 50.0 in May, down slightly from April and exactly at the dividing line between expansion and contraction. Large enterprises remained relatively healthy, while small and medium-sized firms experienced renewed pressure.

Key observations include:

- Production remained in expansion territory.

- New orders softened.

- Raw material inventories declined.

- Employment indicators weakened.

- Supplier delivery times lengthened further.

The message is straightforward: factories continue producing, but demand growth is not keeping pace.

Meanwhile, the non-manufacturing PMI improved modestly to 50.1, led primarily by services, while construction activity remained weak.

YCC View

China’s industrial sector remains supported by export competitiveness and ongoing supply-chain advantages. However, domestic demand has not yet become a sufficiently powerful second engine.

The economy is moving forward, but not accelerating.

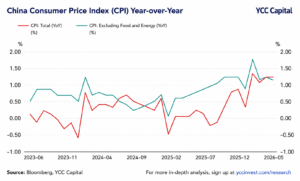

Inflation: Producer Prices Recover Faster Than Consumer Prices

CPI Remains Benign

Consumer inflation rose 1.2% year-over-year in May. Food prices continued to exert downward pressure, particularly pork prices, while service-related categories showed moderate gains.

Consumer price dynamics remain remarkably restrained despite policy easing.

This reflects:

- Cautious household spending behavior.

- Weak housing-related demand.

- Limited pricing power among retailers.

- High savings preferences among consumers.

PPI Continues Recovering

Producer prices increased 3.9% year-over-year, extending the recovery trend observed throughout 2026. Rising energy prices, particularly in coal, petrochemicals, and non-ferrous metals, contributed significantly to the improvement.

Notably, producer inflation is rising faster than consumer inflation.

Historically, this pattern often appears in the early stages of cyclical recoveries when industrial activity improves before household demand fully rebounds.

YCC View

Inflation conditions remain constructive rather than problematic.

We expect:

- CPI to continue gradually rising.

- PPI momentum to moderate somewhat if global energy prices ease.

- Deflation concerns to continue fading throughout 2026.

Trade: Exports Continue to Surprise on the Upside

External Demand Remains the Bright Spot

China’s total trade volume reached $648.1 billion in May, representing 22.6% year-over-year growth.

Key figures:

| Indicator | May 2026 |

|---|---|

| Exports | $376.8 billion |

| Export Growth | +19.4% YoY |

| Imports | $271.4 billion |

| Import Growth | +27.4% YoY |

| Trade Surplus | $105.4 billion |

Export growth remained strong across major trading partners.

Highlights include:

- Exports to the United States rose 35.4%.

- Exports to ASEAN increased 24.3%.

- Exports to the European Union rose 7.6%.

- Exports to Japan increased 10.9%.

A particularly notable trend is the continued expansion of ASEAN’s role within China’s export ecosystem.

Why Exports Are Holding Up

Chinese manufacturers continue benefiting from:

- Scale advantages.

- Cost competitiveness.

- Technological upgrading.

- Strong demand for industrial products and intermediate goods globally.

YCC View

The biggest threat to China’s exports is not tariffs.

The larger risk is a broader slowdown in global growth.

If the U.S. economy enters recession or global demand weakens materially, export momentum could fade quickly. Until then, exports remain China’s strongest macro pillar.

Credit Conditions: Weak Demand for Borrowing Persists

Perhaps the most revealing part of the May data came from financial indicators.

Social Financing Growth Slows

Outstanding Total Social Financing (TSF) expanded 7.7% year-over-year, while RMB loans to the real economy increased only 5.5%.

More importantly, underlying demand remains soft.

Household Borrowing Weakens

In May:

- Household loans declined.

- Short-term consumer loans fell.

- Medium and long-term housing-related loans also contracted.

This signals continued caution among consumers.

People are choosing to save rather than spend or leverage.

Corporate Borrowing Also Remains Muted

Corporate lending showed little evidence of a major investment cycle.

Short-term and long-term corporate loans remained weak, while much of the increase came through bill financing rather than productive investment borrowing.

That is often a sign that:

- Business confidence remains fragile.

- Firms are prioritizing liquidity management.

- Capital expenditure plans remain conservative.

YCC View

Credit data suggest that monetary easing alone cannot solve the problem.

The challenge today is not credit supply.

The challenge is credit demand.

Until households regain confidence and businesses see stronger future opportunities, borrowing activity will likely remain subdued.

Consumption and Investment: The Missing Piece of the Recovery

Retail Sales Disappoint

May retail sales fell 0.6% year-over-year, reflecting both base effects and underlying demand weakness.

Several key categories remained particularly weak:

- Automobiles

- Building materials

- Furniture

- Household appliances

These sectors share an important characteristic:

They are closely linked to housing activity.

When property transactions slow, the ripple effects extend across the broader consumption ecosystem.

A Real-World Example

Buying a home is rarely a single purchase.

A new apartment often leads to:

- Furniture purchases.

- Appliance upgrades.

- Renovation spending.

- Vehicle purchases.

- Increased discretionary consumption.

When housing activity weakens, many of those secondary spending channels weaken as well.

This helps explain why consumption remains sluggish despite improving industrial conditions.

Fixed Asset Investment Continues Contracting

During January-May:

- Fixed asset investment fell 4.1%.

- Private sector investment fell 7.1%.

- Manufacturing investment rose modestly.

- Infrastructure investment remained positive but moderate.

The divergence between public and private investment remains striking.

Private sector confidence has yet to fully recover.

Property Market: Still Searching for a Durable Bottom

The property sector remains the most important drag on domestic demand.

Sales Continue Declining

During the first five months of 2026:

- Property sales area fell 10.8%.

- Residential sales area fell 12.1%.

- Property sales value declined 13.5%.

Meanwhile:

- New construction starts declined 22.6%.

- Residential starts fell 23.4%.

- Completed housing projects declined 23.4%.

Inventory Trends Improve Gradually

One encouraging sign is that unsold housing inventory has begun to decline modestly.

Inventory reduction is often one of the earliest indicators that a housing market is approaching stabilization.

YCC View

We continue to believe China is now in the late stages of its property adjustment cycle.

That does not mean a rapid rebound is imminent.

Instead, the process resembles a large ship slowly changing direction. Momentum built over decades cannot reverse overnight.

The encouraging development is that the property sector’s drag on growth appears to be diminishing gradually.

The second half of 2026 may prove to be a critical period in establishing a durable bottom.

Strategic Outlook

China’s economy today resembles a relay race in which the export sector continues running strongly while domestic demand struggles to grab the baton.

The good news:

- Exports remain resilient.

- Industrial activity is stable.

- Inflation is normalizing.

- Property inventory is improving gradually.

The challenges:

- Consumer confidence remains soft.

- Credit demand is weak.

- Private investment lacks momentum.

- Housing activity continues contracting.

For policymakers, the task remains clear:

- Strengthen domestic demand.

- Support household income growth.

- Encourage private-sector investment.

- Stabilize the housing market without reigniting speculation.

Our baseline expectation is that China’s macro environment in 2026 will be better than in 2025, but growth is likely to remain moderate rather than explosive. Investors should continue monitoring policy implementation, inflation trends, housing stabilization, and signs of improving credit demand as the key indicators that would signal a more durable economic acceleration.

Editorial Board

Ken Cao – Chief Strategist, Global Investment Strategy

Le Gao – Managing Analyst

Yui Nabeshima – Strategist

Mai Ikeda – Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

For free daily market insights, macro strategy updates, and investment research, visit:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com