YCC CAPITAL

Global Fixed Income & Currency Strategy

Date: June 20, 2026

Executive Summary

A new chapter has begun at the Federal Reserve.

At its June 17, 2026 FOMC meeting, the Federal Reserve left the federal funds rate unchanged at 3.50%–3.75%, in line with market expectations. Yet beneath the unchanged rate decision lay one of the most consequential institutional shifts in years: Kevin Warsh’s first meeting as Federal Reserve Chair.

The meeting delivered two major messages.

First, the Fed’s policy stance became materially more hawkish. Inflation projections were revised sharply higher, policymakers projected a higher future rate path, and the updated dot plot suggested that roughly half of participating officials expect at least one rate increase before year-end.

Second, and arguably more important, Warsh initiated a fundamental redesign of how the Federal Reserve communicates, evaluates data, and conducts monetary policy. Forward guidance was substantially reduced, official statements were shortened, and five major policy review groups were established to reassess communications, balance-sheet operations, inflation frameworks, productivity trends, artificial intelligence, and economic data analysis.

For investors, this shift may prove more important than any single rate decision.

For nearly two decades, markets became accustomed to a Federal Reserve that provided extensive guidance regarding future policy intentions. Under Warsh, the institution appears poised to speak less, reveal less, and maintain greater strategic flexibility. Investors may increasingly need to rely on independent analysis of economic conditions rather than waiting for policy signals from central bankers.

At YCC Capital, our baseline expectation remains that the Federal Reserve stays on hold throughout the second half of 2026. However, the probability of future tightening has increased materially, and communication uncertainty itself may become a new source of market volatility.

YCC Perspective

Financial markets often resemble a long road trip. For years, investors traveled with a GPS constantly announcing every upcoming turn. Under Powell, the Federal Reserve frequently told markets where it expected to go next.

Warsh appears intent on turning off much of that navigation system.

The destination—price stability and sustainable growth—remains unchanged. The journey, however, may become significantly less predictable.

That distinction matters enormously for asset pricing.

The June FOMC Meeting: No Rate Change, But a More Hawkish Fed

The Federal Open Market Committee unanimously voted to keep the federal funds target range unchanged at 3.50%–3.75%. This marked the fourth consecutive meeting without a policy adjustment following the 25-basis-point rate cut delivered in December 2025.

While the decision itself was widely anticipated, the broader message represented a meaningful shift.

Prior to the meeting, markets had largely abandoned expectations for near-term rate cuts. Instead, investors increasingly began considering the possibility that the next move could ultimately be higher rather than lower rates. According to market pricing before the meeting, investors were already assigning growing probabilities to renewed tightening by late 2026 or early 2027.

Warsh’s inaugural statement reinforced that perception.

Compared with previous communications, the statement was noticeably shorter and less detailed. References to balancing risks, evaluating future data developments, and potential policy adjustments were largely removed. The document shifted away from elaborate narrative explanations toward concise factual descriptions.

Several changes stood out:

- Labor market conditions were characterized more positively.

- Productivity growth and capital investment were highlighted as strengths.

- Inflation was described as being driven not only by energy prices but also by broader supply disruptions.

- The language emphasizing support for maximum employment was deemphasized relative to the commitment to price stability.

The message was subtle but unmistakable: inflation has moved back to the center of the Fed’s policy framework.

Economic Forecasts: Inflation Becomes the Dominant Concern

The June Summary of Economic Projections revealed a substantially more inflation-focused outlook.

Inflation Forecasts Revised Sharply Higher

The median 2026 PCE inflation forecast rose from 2.7% to 3.6%.

Core PCE inflation projections increased from 2.7% to 3.3%.

Inflation forecasts for 2027 were also revised higher.

These revisions reflect concerns that energy-related shocks and broader supply disruptions may have more persistent effects on price levels than previously anticipated.

Labor Market Outlook Improves

The median unemployment rate forecast for 2026 was lowered modestly from 4.4% to 4.3%.

This adjustment aligns with recent labor market data showing stable unemployment and stronger-than-expected job creation.

Growth Forecasts Slightly Reduced

Real GDP growth projections for 2026 were lowered from 2.4% to 2.2%, suggesting policymakers see somewhat slower economic momentum ahead.

Higher Policy Rate Path

The median year-end federal funds rate projection increased from 3.4% to 3.8% for 2026 and from 3.1% to 3.6% for 2027.

The implication is clear: policymakers now see greater scope for future tightening than they did only three months ago.

The Dot Plot Sends a Hawkish Signal

Perhaps the most striking development came from the updated dot plot.

Among officials submitting interest-rate projections, half now expect at least one rate increase during 2026. Five officials anticipate two hikes, while one projects three increases. Only a single participant continues to foresee rate cuts this year.

This marks a dramatic shift from the March projections, when no official expected rate hikes and several still anticipated rate reductions.

Importantly, Warsh disclosed that he did not submit a personal dot plot projection.

The symbolism matters.

Rather than immediately influencing forecasts through his own submission, Warsh appears focused on reshaping the institution itself.

Understanding the Warsh Doctrine

Inflation First

Throughout his press conference, Warsh repeatedly emphasized the Federal Reserve’s commitment to restoring price stability.

He acknowledged that inflation has remained above the 2% target for approximately five years and stressed that maintaining credibility requires ultimately returning inflation to target.

This signals a leadership philosophy that places greater weight on inflation control than many investors had expected.

Rejecting the Traditional Inflation-Employment Tradeoff

One of Warsh’s most notable comments involved his rejection of the conventional view that policymakers must choose between lower inflation and stronger employment.

He argued that sound policy should allow robust growth, stable prices, and strong labor markets to coexist.

Whether such an outcome proves achievable remains uncertain, but the statement suggests that Warsh may be less willing than previous chairs to tolerate elevated inflation in pursuit of employment gains.

Five Major Working Groups: The Institutional Reset

Warsh announced the creation of five comprehensive review groups.

1. Communications Working Group

Reviewing the Fed’s communication structure, including the future of the Summary of Economic Projections and potentially the dot plot itself.

2. Balance Sheet Working Group

Examining reserve frameworks, balance-sheet composition, and alternative monetary operating structures.

3. Data Working Group

Assessing new information sources and methodological improvements to economic measurement.

4. Productivity and Employment Working Group

Evaluating the impact of AI and emerging technologies on productivity, labor markets, and monetary policy.

5. Inflation Framework Working Group

Reassessing the fundamental drivers of inflation and alternative approaches to maintaining price stability.

The groups are expected to begin work immediately, present preliminary frameworks during the autumn, and complete much of their work before year-end.

Taken together, these initiatives represent the most comprehensive internal review of Federal Reserve operating principles in many years.

AI and the Future of Inflation

Warsh has previously argued that artificial intelligence could become a major disinflationary force by boosting productivity and lowering unit production costs.

During this meeting, however, he adopted a more balanced position.

He acknowledged that AI may ultimately enhance productivity significantly, but emphasized that the economy is currently experiencing a race between demand and supply.

Massive investment in data centers, computing infrastructure, and AI development is already contributing to economic demand. The timing and magnitude of future productivity gains remain uncertain.

This distinction is crucial.

Long-term technological revolutions often begin with inflationary investment booms before producing disinflationary productivity benefits.

History rarely moves in a straight line.

Less Communication, More Market Volatility?

Perhaps the most consequential long-term change involves communication strategy.

Warsh has long argued that excessive forward guidance reduces policymaker flexibility and can trap central bankers into defending outdated forecasts.

At this meeting:

- Forward guidance was significantly reduced.

- The future of the dot plot was openly questioned.

- Press conference frequency may eventually be reconsidered.

- Greater emphasis was placed on economic data rather than Fed commentary.

For investors accustomed to detailed central-bank guidance, this represents a profound adjustment.

Imagine playing chess after years of hearing your opponent explain every upcoming move. Suddenly the explanations stop.

The board remains the same.

The uncertainty increases.

Outlook for the Second Half of 2026

Labor Market Recovery Reduces Pressure for Rate Cuts

The U.S. labor market has shown signs of stabilization and improvement during 2026.

May nonfarm payrolls increased by 172,000, substantially exceeding expectations. Previous months were revised higher, while the unemployment rate remained stable at 4.3%.

The labor market is not overheating, but neither is it deteriorating.

As a result, the urgency for additional easing has diminished.

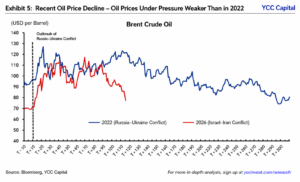

Falling Oil Prices Reduce Immediate Inflation Risks

Although energy prices have been a major contributor to recent inflation readings, geopolitical tensions have eased somewhat and oil prices have retreated from recent highs.

Brent crude declined sharply from above $95 per barrel earlier in June to approximately $79 per barrel by mid-month.

If energy prices remain contained, inflation pressures could moderate more quickly than feared.

Political Constraints Remain Significant

Despite Warsh’s stated commitment to Federal Reserve independence, political realities cannot be ignored.

With U.S. midterm elections approaching and economic concerns becoming increasingly important politically, significant rate increases could face substantial political resistance.

Political pressure alone does not determine monetary policy.

But it can influence the environment in which decisions are made.

YCC Capital Strategic View

Our base case remains unchanged:

Base Case (60%)

- Federal Reserve remains on hold through most or all of H2 2026.

- Inflation gradually moderates.

- Labor markets remain stable.

- First potential rate hike postponed into 2027.

Hawkish Scenario (25%)

- Energy prices rebound.

- Inflation remains persistently above target.

- Markets increasingly price future tightening.

- Treasury yields move higher.

Volatility Scenario (15%)

- Communication reforms create confusion.

- Markets overreact to isolated data releases.

- Asset-price volatility increases even without actual policy changes.

The greatest risk may not be policy action itself.

It may be uncertainty regarding policy intentions.

For years, markets learned how to interpret Powell’s Federal Reserve. Investors must now learn how to interpret Warsh’s.

That learning process is unlikely to be smooth.

Editorial Board

Ken Cao – Chief Strategist, Global Investment Strategy

Le Gao – Managing Analyst

Yui Nabeshima – Strategist

Mai Ikeda – Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

Sign up for free daily market insights and macro research updates at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com