YCC CAPITAL

U.S. Themes & Strategy

────────────────────────────────────────

June 25, 2026

Executive Summary

Financial markets occasionally encounter moments when a central bank decision changes not merely the policy outlook, but the entire framework through which investors interpret economic data. The June Federal Open Market Committee meeting appears to be one of those moments.

Although the Federal Reserve left its policy rate unchanged at 3.50%–3.75%, the market’s attention quickly shifted away from the rate decision itself and toward a broader institutional transformation taking place under newly appointed Chair Kevin Warsh. The meeting delivered a distinctly hawkish signal, triggering one of the sharpest short-end Treasury selloffs in recent years and forcing investors to substantially reprice future rate expectations.

The immediate reaction resembled a sudden recalibration of the market’s compass. Investors entered the meeting expecting a gradual path toward easing. They emerged confronting a Federal Reserve openly discussing additional tightening while simultaneously reducing forward guidance and emphasizing policy flexibility.

The result was dramatic:

- Two-year Treasury yields surged.

- Rate futures rapidly priced in additional hikes.

- The Treasury curve flattened.

- Equity markets were forced to reassess valuation assumptions.

- The probability of a prolonged higher-rate environment increased materially.

At YCC Capital, we believe the key takeaway is not merely that rates may rise further. The deeper story is that markets are being asked to adapt to a fundamentally different communication regime.

The End of the Powell Era Communication Model

The June 17 FOMC meeting represented the first major policy appearance of Chair Kevin Warsh.

The Committee voted unanimously to maintain rates at 3.50%–3.75%. However, the statement itself underwent substantial revision. Large portions of the previous forward-guidance language were removed, and notably, Warsh declined to submit his own economic projections or dot-plot forecast.

This marks a significant break from the practices established under Ben Bernanke, Janet Yellen, and Jerome Powell.

For more than a decade, investors became accustomed to extraordinary transparency from the Federal Reserve. Markets frequently received detailed guidance regarding future policy intentions. Under Warsh, that model appears to be ending.

His long-standing skepticism toward excessive forward guidance is now translating into policy reality.

The implication is profound. Investors may no longer receive the same level of certainty regarding the future path of rates. As a result, market volatility may increasingly reflect evolving data rather than central bank signaling.

In practical terms, markets must now do more of the forecasting work themselves.

The Dot Plot Sends a Clear Hawkish Message

The updated Summary of Economic Projections delivered the strongest surprise.

Among eighteen participants:

- Nine expect at least one rate hike this year.

- Six anticipate at least 50 basis points of additional tightening.

- Eight expect rates to remain unchanged.

- Only one projects a rate cut.

Just three months earlier, the median expectation was for a rate reduction.

Even excluding Warsh’s influence, the Committee appears almost evenly split between those favoring additional tightening and those preferring stability or easing. The balance of power inside the Fed has clearly shifted.

This is not a central bank preparing for recession.

It is a central bank increasingly concerned that inflation risks remain underappreciated.

Inflation Forecasts Move Sharply Higher

The Fed’s inflation projections underwent significant upward revision.

For year-end 2026:

- Headline PCE inflation rose from 2.7% to 3.6%.

- Core PCE inflation increased from 2.7% to 3.3%.

Interestingly, the 2027 inflation forecast moved only modestly higher to approximately 2.3%.

This suggests policymakers largely view the recent inflation acceleration—particularly energy-related price pressures stemming from Middle East tensions and oil market disruptions—as temporary rather than structural.

The distinction matters enormously.

If policymakers believed inflation had become entrenched, long-term forecasts would have risen far more aggressively.

Instead, the Fed appears to be communicating a different message:

Inflation is problematic today, but still controllable over time.

Growth Remains Resilient

The Fed’s growth outlook remains surprisingly constructive.

2026 GDP growth expectations were reduced only slightly, from 2.4% to 2.2%.

Meanwhile, the unemployment rate projection improved marginally from 4.4% to 4.3%.

Taken together, these forecasts effectively reject the hard-landing narrative that many investors anticipated earlier in the year.

The Fed is telling markets that it believes the economy can withstand somewhat tighter financial conditions.

This is a critical distinction because it provides policymakers with political and economic room to tighten further if inflation remains elevated.

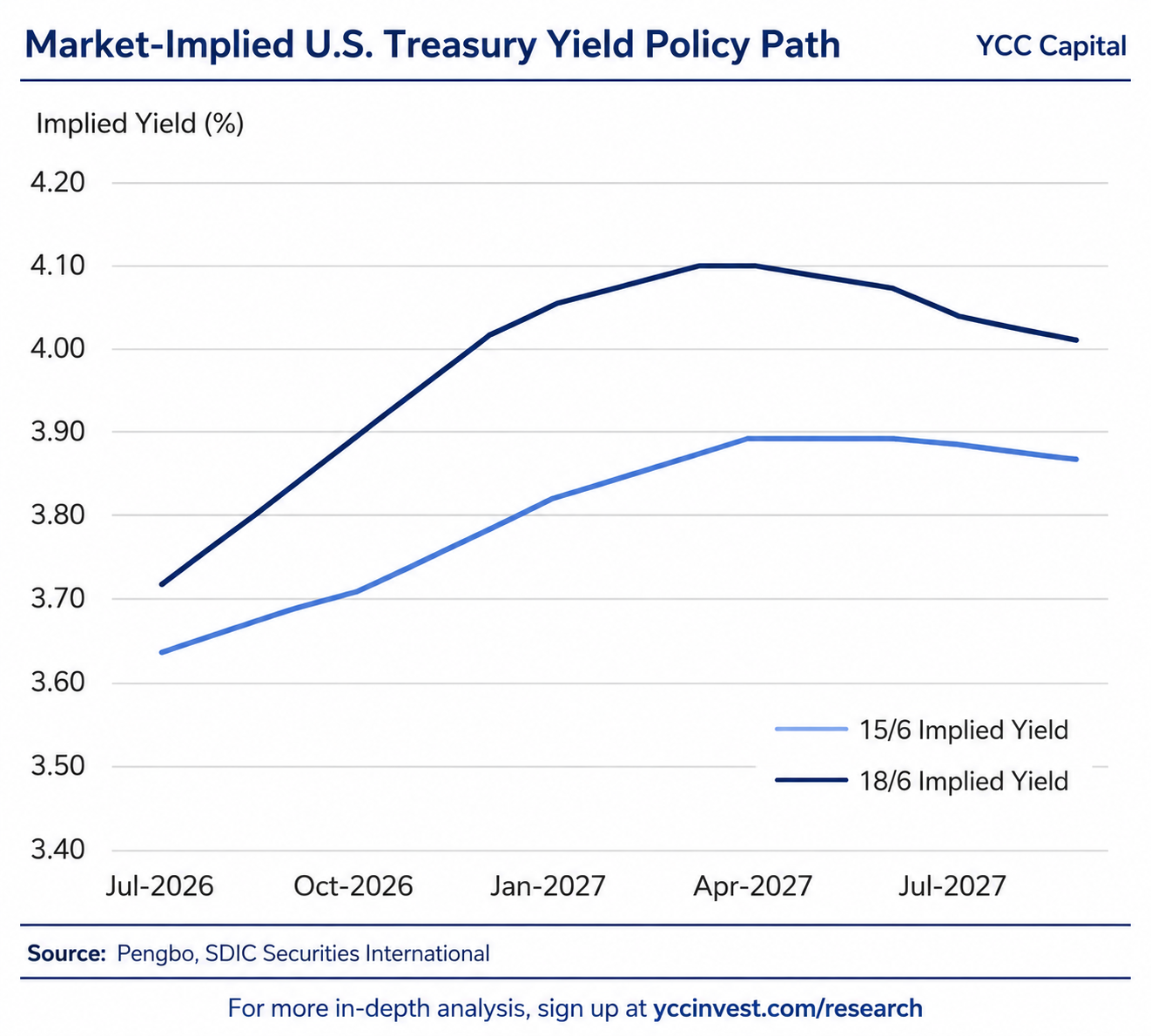

Treasury Markets Experience Violent Repricing

Bond markets reacted immediately.

The two-year Treasury yield jumped approximately 12 basis points in a single session, marking one of the largest FOMC-day increases since the Global Financial Crisis.

Rate futures underwent an equally dramatic adjustment.

Prior to the meeting, markets assigned only about a 27% probability to a September hike.

Within days, that probability surged to approximately 83%.

October contracts moved to fully price an additional hike, while cumulative tightening expectations through year-end climbed to roughly 155 basis points of implied tightening.

Such abrupt repricing underscores how unprepared investors were for the Fed’s hawkish pivot.

Why the Yield Curve Flattened

One of the most important developments was the divergence between short-term and long-term yields.

While front-end Treasury yields surged, 30-year yields actually declined.

At first glance, this may appear contradictory.

In reality, it reflects confidence in the Fed’s inflation-fighting credibility.

Investors appear willing to accept higher short-term rates because they believe those higher rates will ultimately succeed in containing inflation over the long run.

Consequently, long-term inflation premiums fell.

However, investors should not become complacent.

History demonstrates that persistent flattening—or eventual inversion—often signals growing concern that policy may become excessively restrictive.

The risk of policy overshoot is not yet dominant, but it is increasingly being incorporated into market pricing.

Three Issues Investors Must Monitor

1. Warsh’s Five Reform Working Groups

Chair Warsh announced five major review initiatives focused on:

- Federal Reserve communications.

- Balance sheet policy.

- Data reliability.

- Productivity and labor markets.

- Inflation frameworks.

Most findings are expected before year-end.

The balance sheet review is particularly important because it could reshape the current ample-reserves framework governing approximately $6.7 trillion of liquidity.

Markets increasingly expect a gradual but meaningful shift toward continued quantitative tightening.

2. July and September FOMC Meetings

The dot plot expresses intentions, not commitments.

Warsh himself acknowledged that current data alone is insufficient to justify an immediate rate hike.

Additional inflation evidence will likely determine whether the Fed follows through on its increasingly hawkish rhetoric.

The next several inflation reports may therefore carry disproportionate market significance.

3. Oil Prices and Middle East Developments

The inflation outlook remains heavily influenced by energy markets.

If geopolitical tensions ease and oil prices retreat, markets may once again question the need for additional tightening.

Conversely, persistent energy inflation could reinforce the Fed’s hawkish stance.

Retail sales data continue to support the argument that consumer demand remains healthy enough to withstand somewhat tighter policy.

As a result, short-term market direction may increasingly hinge on developments in U.S.-Iran negotiations and broader Middle East dynamics.

Lessons from History: Do Rate Hikes Always Cause Recessions?

Investors often assume that rate hikes inevitably produce recessions.

History suggests a more nuanced reality.

Since 1978, many tightening cycles have indeed followed the familiar sequence:

Rate Hikes → Yield Curve Inversion → Recession

Yet notable exceptions exist.

The most famous example remains the 1994–1995 Greenspan tightening cycle, widely regarded as one of the most successful soft landings in modern monetary history.

More recently, the aggressive tightening campaign beginning in 2022 also avoided the severe recession many economists predicted.

These examples remind investors that monetary tightening raises risks but does not automatically guarantee economic contraction.

The Real Threat to Equities Is Uncertainty

One of the most overlooked observations from market history is that high rates alone rarely devastate stocks.

Equities performed well during:

- The 2004–2006 tightening cycle.

- The 2017–2018 tightening cycle.

What markets struggle with is uncertainty regarding future policy.

When interest-rate volatility rises sharply—as reflected in indicators such as the MOVE Index—investors demand larger risk premiums.

Valuations compress.

Risk assets weaken.

The current environment contains precisely those ingredients.

Middle East tensions, uncertain inflation dynamics, and Warsh’s reduced reliance on forward guidance have created an environment where investors possess less visibility regarding future policy decisions.

That uncertainty—not the current level of rates—is arguably the largest near-term challenge for equities.

The U.S. Economy: Soft Landing, But Increasingly Uneven

At YCC Capital, our base case remains a soft-landing scenario characterized by moderate growth.

However, the internal structure of the economy is becoming increasingly polarized.

Some sectors are accelerating rapidly.

Others remain under pressure.

The result resembles a two-speed economy rather than a broad-based expansion.

AI Remains the Dominant Growth Engine

Artificial intelligence and technology infrastructure spending continue to represent the strongest source of private-sector investment growth.

AI-related capital expenditures are expected to grow more than 40% year-over-year in 2026.

The economic impact increasingly resembles previous transformational infrastructure booms.

Just as railroads reshaped commerce in the nineteenth century and broadband transformed communication in the late twentieth century, AI infrastructure is becoming a foundational layer for future economic activity.

Data centers, semiconductors, networking equipment, and power infrastructure remain primary beneficiaries.

Small Businesses Continue to Struggle

Not all sectors share the same optimism.

The NFIB Small Business Optimism Index declined from 95.9 in April to 95.3 in May, marking a third consecutive month below the long-term average of 98.0.

The message from small businesses is clear:

Conditions have stabilized, but genuine recovery remains elusive.

Many smaller firms continue facing elevated financing costs, rising labor expenses, and weakening consumer purchasing power.

Manufacturing Returns to Expansion

After a prolonged period of contraction during 2025, U.S. manufacturing has re-entered expansion territory.

The ISM Manufacturing PMI reached 54.0 in May, its highest level in four years.

AI-driven data center construction has played a meaningful role in this improvement.

Meanwhile, services activity remains even stronger.

The Services PMI climbed to 54.5 and has now remained in expansion territory for nearly two years.

The main concern lies in prices.

The services price index rose to 71.3, its highest reading since August 2022, suggesting inflation pressures remain present beneath the surface.

Labor Markets Remain Surprisingly Durable

Hard employment data continue to show resilience.

Job openings increased to approximately 7.6 million.

The ratio of job openings to unemployed workers moved back above one, a level typically associated with labor market balance.

The unemployment rate held steady at 4.3%.

Nonfarm payrolls increased by 172,000 in May, exceeding expectations.

Yet softer confidence measures tell a different story.

Consumer sentiment remains historically weak.

This divergence between strong labor-market statistics and cautious household psychology represents one of the defining features of the current cycle.

Americans are working and earning, but many still feel financially constrained.

Consumer Spending Continues to Hold Up

Retail sales data remain surprisingly strong.

Headline retail sales increased 0.9% month-over-month in May.

Even after excluding automobiles and gasoline, spending remained healthy.

Core control-group retail sales accelerated to 0.7%.

Eleven of thirteen retail categories recorded gains.

Online retail emerged as the strongest contributor.

This reflects an increasingly value-conscious consumer.

Families are not necessarily spending less.

They are spending more selectively.

Many households now search aggressively for discounts, promotions, and online alternatives.

The behavior resembles a family navigating rising grocery bills by comparison-shopping rather than abandoning purchases entirely.

Consumption remains resilient, but efficiency has become a priority.

The Growing Divide Inside Consumer Spending

Beneath the headline strength lies a significant structural shift.

Discount retailers, e-commerce platforms, and value-oriented channels continue gaining market share.

Meanwhile, many mid-market retailers face mounting pressure.

Businesses dependent on discretionary purchases—including apparel, furniture, restaurants, and household goods—are experiencing a more difficult operating environment.

The consumer is not disappearing.

The consumer is becoming more selective.

That distinction matters enormously for equity investors.

Investment Implications

Equities

Near-term volatility may remain elevated as markets adapt to the Warsh era.

However, fundamentals ultimately drive long-term performance.

We continue to favor areas directly linked to AI infrastructure investment, particularly semiconductors and related hardware segments where earnings visibility remains strongest.

Over the medium term, investor attention should increasingly shift toward application-layer monetization.

The next phase of the AI cycle will be determined not by infrastructure spending alone, but by whether corporations successfully convert AI investment into sustainable profits.

Fixed Income

We remain cautious on duration exposure.

The bond market’s hawkish repricing process may not yet be complete.

Yield-curve steepening trades appear less attractive than earlier in the cycle, while potential balance-sheet reforms could introduce additional volatility into term premiums.

Foreign Exchange

The U.S. dollar should remain supported in the near term by higher rate expectations and relatively strong economic performance.

Longer term, questions surrounding Federal Reserve independence and evolving institutional frameworks deserve close monitoring.

For now, however, U.S. economic resilience continues to provide a meaningful foundation for dollar strength.

YCC Capital Strategic View

The market is entering a new chapter.

Under Powell, investors became accustomed to a Federal Reserve that often illuminated the road ahead with detailed guidance. Under Warsh, the road appears intentionally less illuminated.

That transition will not be comfortable.

Periods of uncertainty often feel unsettling because investors lose familiar reference points. Yet markets ultimately return to fundamentals.

Our core view remains that the United States is progressing toward a soft landing rather than a recession. Growth is slowing but remains positive. Inflation is proving stickier than hoped but remains manageable. AI investment continues to provide a powerful structural tailwind.

The path forward may become more volatile, but volatility alone is not recession.

For investors willing to focus on earnings quality, productivity gains, and structural beneficiaries of technological investment, opportunities remain abundant despite the changing policy landscape.

Editorial Board

Ken Cao – Chief Strategist, Global Investment Strategy

Le Gao – Managing Analyst

Yui Nabeshima – Strategist

Mai Ikeda – Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

Investor Relations: ir@yccinvest.com

For free daily market insights, macro research, and investment commentary, visit:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com