YCC CAPITAL

Commodity & Energy Strategy

June 27, 2026

Executive Perspective

Every major oil shock tells the same story at first glance: prices surge, headlines scream about shortages, and markets brace for recession. Yet history repeatedly reminds investors that the real economic consequences are rarely determined by the initial disruption alone. Instead, they are shaped by what follows—how quickly production returns, how much spare inventory remains, and whether delayed demand eventually re-emerges.

The current Middle East supply disruption appears to fit that historical pattern. Although crude prices have retreated significantly from their spring highs, the decline should not be mistaken for a normalization of global energy markets. Much of the apparent resilience has been purchased through extraordinary inventory drawdowns, emergency supply substitution from non-Middle Eastern exporters, and temporary demand destruction caused by elevated shipping costs and record insurance premiums.

From YCC Capital’s perspective, investors risk focusing excessively on today’s oil price while overlooking tomorrow’s supply constraints. Physical oil infrastructure cannot simply be switched back on overnight. Damaged wells, transportation networks, export terminals, and storage facilities require months—not weeks—to restore. Meanwhile, inventories that have cushioned markets throughout the first half of the year are steadily being depleted.

Like a household relying on its savings account after losing income, the global oil market has managed to avoid immediate crisis by spending accumulated reserves. Eventually, however, those savings become exhausted unless income recovers. The same logic increasingly applies to global petroleum inventories.

Our base case therefore remains that crude oil prices will remain structurally elevated throughout the second half of 2026, even if geopolitical tensions gradually stabilize.

Why Hasn’t Oil Reached Crisis Levels?

The most surprising feature of recent months has not been the supply disruption itself, but rather the market’s relatively orderly response.

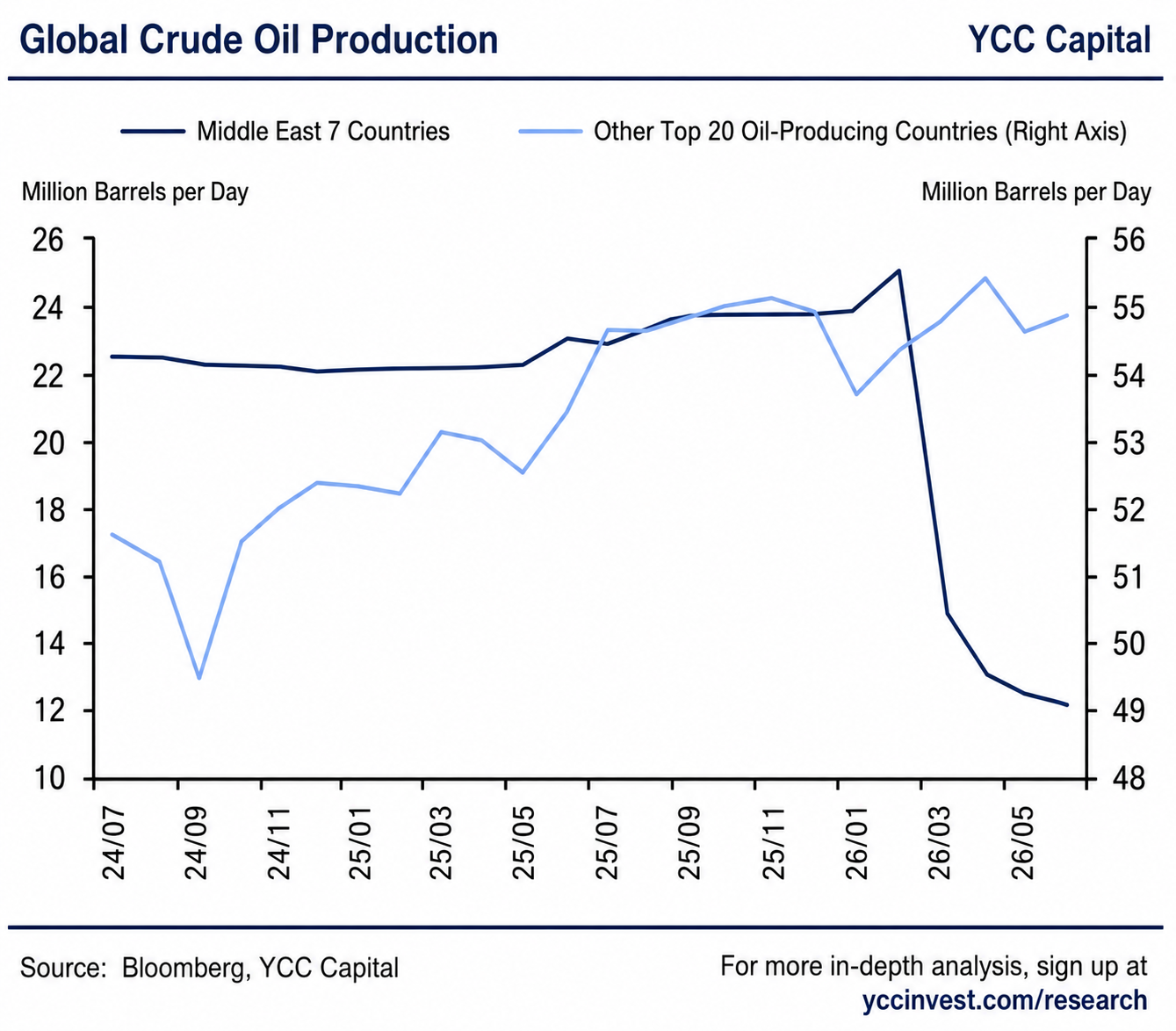

Since the outbreak of the U.S.–Iran conflict and repeated disruptions around the Strait of Hormuz, roughly one quarter of global seaborne petroleum trade has been affected. Seven major Middle Eastern producers collectively reduced output dramatically, while global oil production fell sharply from pre-conflict levels.

Under normal circumstances, such a shock might have pushed Brent crude well above previous historical peaks. Instead, prices briefly approached US$120 per barrel before retreating toward the US$80 range.

This resilience reflects three temporary stabilizers rather than any lasting improvement in market fundamentals.

Supply Substitution Has Offset Part of the Shock

The first stabilizer has been a rapid increase in exports from producers outside the Middle East.

North America, Latin America and Eastern Europe have collectively increased crude exports substantially, offsetting roughly half of the lost Middle Eastern supply. Compared with February levels, Middle Eastern exports declined by approximately 324 million barrels by May, while total global exports fell by only 148 million barrels.

North America alone contributed nearly 100 million additional barrels of exports during this period, with Latin America and Eastern Europe also expanding shipments meaningfully.

The United States has played a particularly important role. American crude exports recently reached record levels while net crude imports fell close to zero, demonstrating the remarkable flexibility of North American energy production.

However, this substitution should not be mistaken for unlimited spare capacity.

Most major non-OPEC producers are already operating near practical production limits. Incremental supply becomes progressively more expensive as production expands, suggesting that further substitution will become increasingly difficult if Middle Eastern disruptions persist.

Source: Bloomberg, YCC Capital

Strategic Inventories Have Become the World’s Shock Absorber

The second stabilizing force has been unprecedented inventory drawdowns.

Rather than allowing domestic shortages to develop, governments have increasingly relied on commercial and strategic petroleum reserves.

The United States offers perhaps the clearest example.

Since the conflict began, U.S. crude inventories have fallen by approximately 96 million barrels, including over 75 million barrels released from the Strategic Petroleum Reserve (SPR). Reserve levels have now declined to their lowest point since the 1980s.

Importantly, this pace of depletion exceeds that observed during the Russia–Ukraine energy crisis in 2022.

These releases have allowed American refiners to maintain high utilization rates despite declining imports, preserving gasoline availability and helping stabilize consumer inflation.

Japan, China and several OECD economies have adopted similar inventory management strategies.

Yet inventories represent a finite buffer rather than a renewable source of supply.

Markets often underestimate this distinction. Releasing reserves can smooth short-term volatility, but every barrel withdrawn today represents one less barrel available for future emergencies.

The longer geopolitical disruptions continue, the smaller this protective cushion becomes.

Demand Has Been Delayed—Not Destroyed

The third factor preventing a sustained oil spike has been temporary demand suppression.

High crude prices naturally reduce consumption, but today’s weakness appears less like permanent destruction and more like postponed purchasing.

Global seaborne crude imports declined approximately 17% between February and May, according to shipping data.

China accounted for much of this decline.

Imports from seven major Middle Eastern producers fell to their lowest recorded levels, while imports from alternative suppliers increased only modestly. Domestic refinery utilization also weakened noticeably, reflecting delayed downstream demand.

However, this should not necessarily be interpreted as a structural collapse in Chinese energy consumption.

Instead, Chinese refiners appear to be utilizing existing inventories while waiting for more favorable pricing conditions. Once prices moderate and logistics improve, some of this deferred demand is likely to return.

Other Asian importers tell a similar story.

Japan, South Korea and Singapore all experienced temporary import declines during the peak of price volatility before gradually rebuilding purchases as markets stabilized.

Demand has therefore been shifted through time rather than permanently eliminated.

For investors, this distinction matters enormously.

Delayed demand frequently returns precisely when inventories are already depleted, creating the conditions for renewed price pressure.

Supply Recovery Will Be Much Slower Than Production Shutdowns

Markets frequently assume that once geopolitical tensions ease, oil production quickly resumes.

History suggests otherwise.

Restarting oil production is considerably more complicated than shutting it down.

Oil reservoirs depend upon carefully balanced underground pressure systems. Extended shutdowns alter these pressure dynamics, increasing the risk of water intrusion, sediment contamination and declining production efficiency when operations resume.

Middle Eastern carbonate reservoirs introduce additional engineering complexity. Extended inactivity also allows paraffin and asphalt deposits to accumulate inside wells and pipelines, increasing restoration costs.

Industry estimates suggest that heavily damaged producers such as Iraq could require six to nine months merely to restore production capacity under ideal conditions.

Physical infrastructure presents an additional challenge.

Storage facilities, export terminals, loading ports and pipelines have all sustained damage during recent hostilities. Repairing this network requires significant financial resources and engineering capacity.

History reinforces this conclusion.

Following U.S. sanctions against Iran in 2019 and the COVID-19 disruption in 2020, Iranian oil production recovered only gradually. Output declined rapidly but recovered far more slowly, illustrating the asymmetry between production losses and restoration.

This asymmetry remains one of the most underappreciated features of today’s oil market.

China’s Energy Transition Does Not Eliminate Oil Dependence

China continues investing aggressively in renewable energy, electric vehicles and industrial electrification.

Nevertheless, oil remains deeply embedded across heavy manufacturing, chemicals, logistics, aviation and numerous industrial supply chains.

Recent data indicate that the long-term decline in oil intensity has begun to slow.

While China’s economic model is gradually becoming less energy intensive, petroleum continues to occupy an essential role within industrial production.

From YCC Capital’s perspective, this represents another reason why global oil demand may prove more resilient than consensus currently expects.

At the same time, China’s broader macroeconomic outlook remains challenging.

Property-sector weakness, subdued private investment and persistent industrial overcapacity continue weighing on domestic demand. These structural headwinds are likely to limit China’s pricing power, meaning any increase in producer inflation would primarily reflect imported commodity costs rather than improving underlying economic momentum.

Transportation Costs Have Become an Inflation Multiplier

Crude oil prices represent only one component of delivered energy costs.

Shipping expenses have risen dramatically following disruptions around the Strait of Hormuz.

Marine insurance premiums reportedly increased from roughly 0.2–0.3% of vessel value before the conflict to between 1% and 3% afterward.

Freight rates experienced similar increases as tanker availability tightened.

These higher transportation costs effectively amplify the inflationary effects of elevated crude prices.

Importers pay more not only for the oil itself but also for moving and insuring every shipment.

Shipping companies have likewise experienced significant margin compression despite higher freight rates, reflecting escalating operating costs and heightened geopolitical risk.

Three Scenarios for Oil Prices in H2 2026

Scenario 1: Diplomatic Breakthrough (25% Probability)

If U.S.–Iran negotiations produce a comprehensive agreement within the current sixty-day framework and the Strait of Hormuz fully reopens, global supply conditions would gradually normalize.

We estimate Brent crude averaging approximately US$70 per barrel in Q3 before easing toward US$65 in Q4.

Under this outcome:

- U.S. CPI moderates toward 3.3% in Q3 and around 3.1% in Q4.

- China’s PPI averages 4.4% in Q3 before slowing to 3.4% in Q4.

Even in this optimistic scenario, prices remain well above pre-conflict expectations because inventory rebuilding would continue supporting demand.

Scenario 2: Managed Stalemate (60% Probability)

This remains YCC Capital’s central expectation.

Negotiations continue without comprehensive resolution, while shipping conditions fluctuate between partial reopening and periodic disruption.

Oil markets remain tight, but panic gradually subsides.

Brent crude averages approximately US$80 per barrel during Q3 before easing modestly toward US$75 during Q4.

Inflation would likely evolve as follows:

- U.S. CPI averages roughly 3.8% in Q3 before moderating toward 3.5%–4.0% in Q4.

- China’s PPI averages approximately 4.8% in Q3 and 4.4% in Q4.

This scenario reflects a world where inventories continue falling faster than production can recover.

Scenario 3: Renewed Escalation (15% Probability)

Should negotiations collapse entirely and the Strait of Hormuz experience renewed closure, supply disruptions would intensify substantially.

Brent crude could average US$100 per barrel during Q3 before remaining elevated near US$95 in Q4.

Such an outcome would likely push:

- U.S. CPI toward 4.7% in Q3 and approximately 5.0% during Q4.

- China’s PPI toward 5.7% in Q3 and 5.9% in Q4.

This represents the primary macroeconomic tail risk for global markets over the coming quarters.

Investment Implications

For investors, the most important conclusion is not that oil prices will necessarily rise dramatically from current levels.

Rather, it is that the probability of a rapid return to low-energy-price conditions appears considerably smaller than markets currently assume.

Persistent energy inflation favors selective exposure to energy producers, commodity-linked currencies and inflation-sensitive assets while reducing the attractiveness of long-duration fixed income should inflation expectations remain elevated.

Within equities, sectors benefiting from pricing power and stable cash generation appear better positioned than highly energy-intensive industries.

From a geographic perspective, the United States remains comparatively resilient owing to its expanding domestic energy production and greater energy independence. While higher oil prices would temporarily delay the Federal Reserve’s progress toward price stability, the broader U.S. economy retains greater flexibility than many import-dependent regions.

China, by contrast, remains more vulnerable to imported commodity inflation against the backdrop of structural domestic economic challenges. Rising energy costs would add further pressure to manufacturers already facing weak demand, excess capacity and slowing private-sector investment.

YCC Capital Strategic View

Oil markets often appear calm immediately before structural imbalances become fully visible.

Today’s moderation in prices should therefore not be interpreted as evidence that supply constraints have disappeared. Instead, inventories have temporarily concealed the true extent of the disruption.

The coming quarters are likely to be defined less by geopolitical headlines than by the pace at which inventories are exhausted relative to production recovery.

That dynamic supports our base case that crude prices remain structurally firm throughout the second half of 2026, with inflation proving more persistent than many market participants currently anticipate.

Investors should therefore focus not merely on where oil trades today, but on how quickly the world’s energy safety buffer is disappearing beneath the surface.

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S. and structured as a Rule 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.

Contact Us

For institutional inquiries and media requests:

Email: ir@yccinvest.com

Sign up for free daily market insights at:

Prepared by YCC Capital Research.