Global Strategy

June 27, 2026

Executive Perspective

Financial markets rarely wait for certainty—they price the direction of change. Over the past six months, investors have been consumed by one question: would geopolitical tensions in the Middle East trigger a second inflation wave severe enough to derail the global easing cycle?

Our assessment is increasingly that the answer is no.

The energy shock that temporarily disrupted inflation expectations now appears to be evolving into a geopolitical risk premium rather than a persistent macroeconomic regime shift. Oil prices remain sensitive to headlines, yet the transmission into core inflation has been remarkably limited across most developed economies. As negotiations surrounding Iran gradually reduce the probability of a prolonged supply disruption through the Strait of Hormuz, the world economy is beginning to transition from an environment dominated by inflation fears toward one increasingly shaped by liquidity conditions.

History reminds us that markets often become obsessed with yesterday’s crisis precisely when tomorrow’s opportunity is quietly taking shape. Like a homeowner who continues reinforcing the roof after the storm has already passed, policymakers and investors risk focusing too heavily on fading inflation while underestimating the significance of improving financial conditions.

For investors, this transition matters enormously.

Rather than asking whether inflation has disappeared completely, the more important question is whether central banks can once again shift their attention toward growth, liquidity, and financial stability. We believe that pivot has already begun.

Investment Thesis

YCC Capital believes the second half of 2026 will be characterized by four major macro transitions.

First, the inflation shock is becoming increasingly concentrated in energy rather than broad-based consumer prices. Core inflation across most developed markets continues to moderate despite elevated oil prices, suggesting that wage-price spirals remain largely absent.

Second, global economic growth is slowing without collapsing. Manufacturing activity linked to artificial intelligence infrastructure continues to outperform traditional sectors, while services activity has softened under the weight of higher interest rates and weaker consumer confidence.

Third, central banks are entering a prolonged policy pause rather than embarking on another aggressive tightening campaign. Although several policymakers have temporarily delayed additional rate cuts because of geopolitical uncertainty, the overall direction of monetary policy remains substantially easier than during the inflation peak.

Finally, liquidity—not inflation—will increasingly become the dominant driver of asset prices. As balance-sheet policy gradually becomes more important than policy rates, investors should begin paying closer attention to the evolution of quantitative tightening and financial conditions rather than focusing exclusively on headline inflation data.

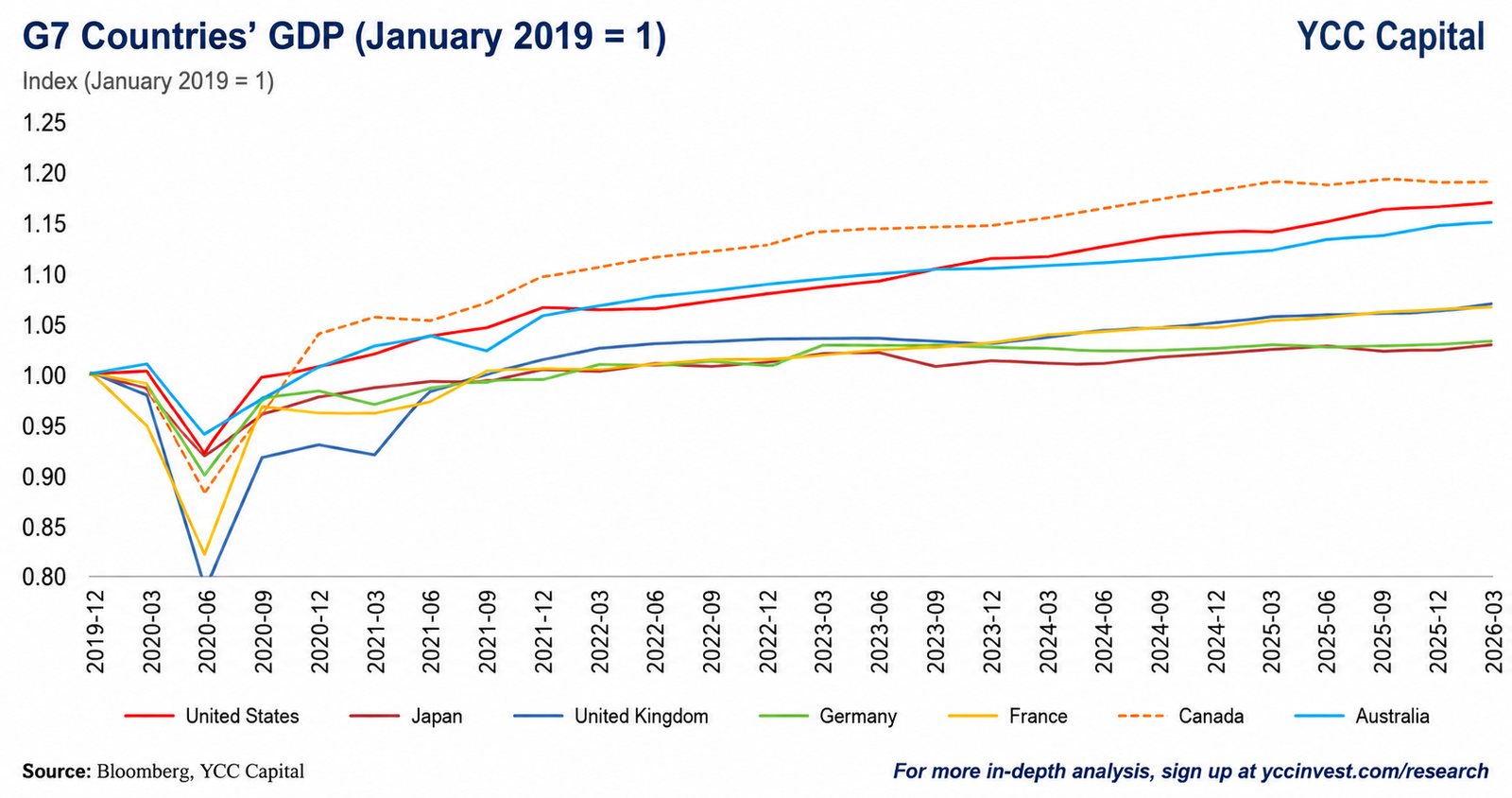

The Real Economy: Growth Continues, But Momentum Is Uneven

Across the G7 economies, first-quarter growth remained positive but subdued.

Germany finally surpassed its previous post-pandemic output peak, driven primarily by stronger exports rather than domestic demand. France experienced similarly modest expansion, although consumer spending remained restrained. Britain benefited from a mild improvement in household demand, while Japan continued to outperform expectations thanks to robust AI-related exports and resilient domestic consumption.

Canada presents a more concerning picture. Economic output has effectively stagnated over the past year as restrictive monetary policy continues weighing on investment and housing activity. Australia likewise experienced slowing growth following multiple policy rate increases, illustrating how monetary tightening continues to filter through developed economies with considerable lags.

One important takeaway emerges from this divergence.

The global economy is no longer moving in synchrony. Export-oriented economies integrated into the AI supply chain are outperforming economies driven primarily by domestic consumption. That distinction is likely to become even more important over the coming year.

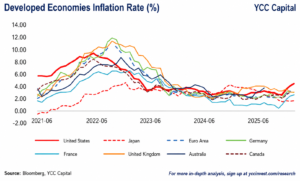

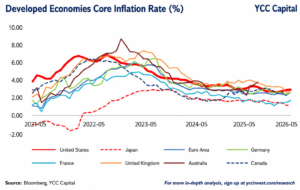

Inflation Is Cooling Where It Matters

The most important development in global inflation is not that headline prices have become stable—it is that inflation is increasingly failing to spread beyond energy.

During the first half of 2026, renewed geopolitical tensions surrounding the Middle East pushed crude oil prices materially higher, prompting fears that the global economy was entering another inflationary cycle reminiscent of 2022. Yet the data tell a different story. Across the United States, Europe, Canada, Australia, and Japan, core inflation has remained comparatively resilient to the energy shock.

This distinction is critical.

Headline inflation often dominates financial headlines because consumers experience higher fuel prices immediately. Central banks, however, are far more concerned with whether temporary price increases become embedded in wages, rents, and services. Thus far, that transmission mechanism has remained surprisingly weak.

Several factors explain this outcome. Household demand has moderated under the weight of higher interest rates, supply chains have largely normalized, and businesses have become considerably more cautious about passing temporary input-cost increases onto consumers. The inflation psychology that characterized the immediate post-pandemic period has faded.

Regional differences nevertheless remain significant.

Japan and the United Kingdom have experienced relatively softer inflation outcomes thanks partly to domestic energy policies and government support measures. Germany’s inflation has stabilized despite lingering industrial cost pressures, while France has experienced somewhat greater sensitivity to higher energy prices because of differences in consumer energy exposure.

Canada presents perhaps the clearest example of policy restraint working through the economy. Slowing growth, weaker housing activity, and cooling labor-market conditions have collectively reduced underlying inflation pressure compared with last year.

Taken together, the evidence suggests that developed economies are confronting an energy price shock rather than a generalized inflation regime. That distinction substantially reduces the probability that central banks will be forced into another aggressive tightening cycle.

Markets should therefore become increasingly selective when interpreting inflation surprises. Not every increase in headline CPI represents a fundamental shift in monetary policy.

Central Banks Have Pressed Pause—Not Reverse

Financial markets frequently confuse temporary policy hesitation with structural policy reversal.

The recent actions of major central banks illustrate precisely this distinction.

Several monetary authorities have chosen to delay additional easing while evaluating the implications of geopolitical risks. Australia paused after a sequence of tightening measures. The European Central Bank and the Bank of Japan adopted more cautious policy settings amid renewed uncertainty surrounding energy markets. Meanwhile, the Federal Reserve, Bank of England, and Bank of Canada have maintained a patient stance while emphasizing their willingness to respond should inflation expectations become unanchored.

None of these decisions necessarily imply that policymakers have abandoned the broader transition toward easier financial conditions.

Instead, they reflect an environment in which central banks face two competing objectives. On one side lies the need to preserve inflation credibility. On the other stands the growing reality that economic momentum is slowing across much of the developed world.

History suggests that policymakers rarely move in straight lines. Monetary cycles often contain lengthy pauses during which officials collect additional evidence before proceeding. Investors who interpret every pause as the beginning of a new tightening cycle frequently underestimate the longer-term direction of policy.

Our baseline expectation remains that policy rates have already reached or are approaching cyclical peaks across most developed economies. Future monetary accommodation may unfold more gradually than markets anticipated at the beginning of the year, but the strategic direction continues to favor easing rather than renewed restriction.

Manufacturing Finds an Unexpected Engine: Artificial Intelligence

One of the more striking features of the current expansion is the widening divergence between manufacturing sectors.

Traditional manufacturing tied to housing, consumer durables, and cyclical spending remains subdued across many advanced economies. Services activity has likewise softened as households become increasingly cautious with discretionary spending.

Yet a different segment of manufacturing has entered a remarkably powerful investment cycle.

The rapid build-out of artificial intelligence infrastructure continues to generate substantial demand for semiconductors, advanced machinery, networking equipment, industrial automation, and power systems. This investment boom has become an important stabilizing force for global industrial production.

The United States remains the principal beneficiary.

Large-scale capital expenditures by hyperscale cloud providers, semiconductor manufacturers, and digital infrastructure firms have supported manufacturing output even as broader economic growth moderates. American purchasing manager surveys continue to signal expansion, reflecting the resilience of investment-driven demand rather than broad-based consumer strength.

Japan and South Korea occupy particularly favorable positions within this ecosystem.

Both economies have benefited from accelerating exports of advanced components, semiconductor equipment, precision manufacturing technologies, and industrial machinery. Export growth has surprised consistently to the upside, reinforcing the view that AI represents not merely another technology cycle but a significant industrial investment cycle with global implications.

Europe’s manufacturing outlook remains comparatively mixed. While selected capital-goods exporters continue benefiting from AI-related demand, broader industrial activity remains constrained by weaker domestic demand, elevated energy costs, and cautious corporate investment.

The divergence illustrates a broader structural theme increasingly shaping global markets.

Not all manufacturing is cyclical.

Manufacturing linked to digital infrastructure, computing power, automation, and artificial intelligence increasingly behaves more like long-duration capital investment than traditional industrial production. Investors who fail to distinguish between these segments risk drawing misleading conclusions about the health of the global economy.

Europe Faces the Greatest Policy Trade-Off

Among major developed economies, Europe arguably confronts the most difficult macroeconomic balancing act.

Economic growth remains subdued, consumer confidence has yet to recover fully, and labor-market conditions have softened in several key member states. Germany continues to struggle with sluggish domestic demand despite an improvement in exports, while France faces persistent pressure from slower employment growth and higher energy sensitivity.

Against this backdrop, policymakers have had little room for error.

Maintaining restrictive monetary policy for too long risks further weakening already fragile domestic activity. Relaxing policy prematurely, however, could undermine inflation credibility if energy prices remain volatile.

This dilemma helps explain why European markets have exhibited greater sensitivity to geopolitical developments than their American counterparts.

Unlike the United States, Europe remains more directly exposed to imported energy shocks and possesses less fiscal flexibility to cushion households from sustained price increases. Consequently, relatively small changes in global energy markets can produce disproportionately large shifts in investor sentiment toward European assets.

Our assessment remains that Europe is unlikely to experience a severe recession under the base case. Nevertheless, the region appears positioned for a slower and more uneven recovery than either the United States or Japan, particularly if business investment remains subdued.

For global investors, European equities may continue to generate selective opportunities in globally competitive industrial exporters, but broad index-level outperformance is likely to remain constrained until domestic demand strengthens more meaningfully.

The United States: Slower Growth, Stronger Foundations

The American economy continues to confound both pessimists and optimists.

Growth has unquestionably moderated from the extraordinary pace that followed the pandemic reopening. Consumers have become more selective, interest-rate-sensitive sectors remain under pressure, and business surveys periodically reflect softer sentiment. Yet beneath these cyclical fluctuations, the structural foundations of the U.S. economy remain remarkably resilient.

This resilience stems from three mutually reinforcing forces.

The first is productivity. Artificial intelligence is no longer simply a source of market enthusiasm; it is becoming a measurable driver of corporate investment and operational efficiency. Capital expenditure on data centers, cloud infrastructure, power generation, semiconductor fabrication, and industrial automation continues to expand at rates rarely observed outside major technological revolutions.

The second is corporate profitability.

Despite elevated financing costs, large U.S. corporations continue to generate robust cash flows and maintain healthy balance sheets. Unlike previous tightening cycles, many companies entered this period having refinanced debt at historically low interest rates, reducing the immediate impact of higher borrowing costs.

The third is financial flexibility.

American capital markets remain the deepest and most liquid in the world. Even during periods of policy uncertainty, companies retain comparatively strong access to financing, venture capital, and equity issuance. This structural advantage allows investment cycles to continue even when economic growth temporarily slows.

The result is an economy that appears capable of sustaining moderate expansion without generating excessive inflation.

We therefore continue to view the United States as the global economy’s primary engine of innovation-led growth. While valuation discipline remains essential, long-term investors should avoid confusing cyclical moderation with structural deterioration.

China: Cyclical Stabilization Does Not Resolve Structural Headwinds

China’s economy continues to face a more complicated adjustment than many headline indicators suggest.

Incremental policy support may succeed in preventing a sharp contraction in activity, but stabilization should not be mistaken for a return to the high-growth model that defined previous decades.

The underlying challenges remain substantial.

The property sector continues to experience prolonged balance-sheet repair, limiting household wealth creation and suppressing private consumption. Local governments face persistent fiscal constraints following years of infrastructure-driven expansion. Private-sector confidence has yet to recover meaningfully, reflecting ongoing regulatory uncertainty and weaker entrepreneurial sentiment.

Demographic trends add another layer of complexity. A shrinking working-age population, slower labor-force growth, and declining productivity gains reduce the economy’s long-term potential growth rate relative to the past two decades.

Meanwhile, external conditions have become increasingly challenging.

Trade frictions, supply-chain diversification, and geopolitical competition continue encouraging multinational corporations to reduce concentration risk. While China remains an indispensable manufacturing base in numerous industries, the direction of global capital allocation increasingly favors geographic diversification rather than further concentration.

Policy measures are therefore likely to remain reactive rather than transformative.

Additional fiscal support, monetary easing, and selective industrial policies may cushion cyclical weakness, but they are unlikely to reverse deeper structural forces involving demographics, debt accumulation, and declining returns on investment.

For global investors, this argues for a highly selective approach rather than broad-based optimism. Opportunities continue to exist in globally competitive exporters and technologically advanced manufacturers, yet the broader macro backdrop remains significantly less favorable than in previous cycles.

Japan: Quiet Structural Progress Continues

Japan’s investment case has become increasingly misunderstood.

Much of the global discussion continues to focus on short-term questions surrounding monetary normalization and exchange-rate volatility. While these issues deserve attention, they risk overshadowing a more important long-term transformation taking place beneath the surface.

Corporate governance reforms continue improving capital allocation.

Shareholder returns have strengthened through higher dividends and share repurchases. Companies are becoming increasingly willing to deploy excess cash toward productive investment rather than maintaining excessively conservative balance sheets.

At the same time, Japan occupies an increasingly strategic position within the global technology supply chain.

Demand for semiconductor equipment, advanced materials, industrial robotics, precision manufacturing, and AI-related hardware has provided meaningful support for exports. Japanese companies continue to hold globally competitive positions in several critical technologies that are becoming increasingly valuable as investment in artificial intelligence accelerates worldwide.

Domestic demand has also shown encouraging signs of gradual improvement.

Although higher interest rates represent an adjustment after decades of extraordinarily accommodative monetary policy, normalization itself should not be interpreted as a negative development. Rather, it reflects growing confidence that Japan is finally moving beyond the deflationary environment that constrained economic performance for much of the past generation.

Short-term volatility is inevitable as financial markets adapt to a changing policy framework. Nevertheless, we remain constructive on Japan’s medium- and long-term outlook, viewing recent normalization as evidence of economic healing rather than deterioration.

Markets Are Transitioning from an Inflation Cycle to a Liquidity Cycle

Every macroeconomic cycle has a dominant variable.

During 2022 and 2023, inflation determined virtually every asset price. Bond yields, equity valuations, currencies, and commodities all moved primarily in response to changing inflation expectations.

That environment is beginning to evolve.

As inflation gradually becomes less synchronized across developed economies and core price pressures continue easing, financial markets are likely to redirect their attention toward liquidity conditions.

This shift carries profound implications.

Policy rates remain important, but they no longer tell the entire story. Investors should instead monitor the interaction between central-bank balance sheets, government borrowing requirements, banking-sector liquidity, credit availability, and private-sector financial conditions.

Liquidity often influences asset prices long before it materially affects economic statistics.

Like changing ocean tides beneath the surface, shifts in liquidity are frequently invisible to casual observers until markets have already begun moving. Investors who focus exclusively on headline inflation risk overlooking the next major driver of financial conditions.

Our expectation is that quantitative tightening will gradually become more flexible as policymakers seek to balance inflation credibility with financial stability. This adjustment is unlikely to resemble the aggressive monetary expansion experienced during the pandemic, but even modest improvements in liquidity could provide meaningful support for risk assets.

Consequently, the second half of 2026 may become increasingly defined not by fears of renewed inflation, but by the gradual return of financial liquidity as the dominant macroeconomic force.

Strategic Asset Allocation

Against this backdrop, YCC Capital favors a disciplined but constructive allocation strategy.

We remain selectively overweight U.S. equities, particularly businesses benefiting from artificial intelligence infrastructure, digital transformation, industrial automation, and power investment. These structural themes continue to enjoy durable capital expenditure support that extends well beyond the current business cycle.

We also maintain a positive medium-term outlook on Japanese equities, where improving corporate governance, stronger shareholder returns, and technology exports provide a compelling combination of cyclical and structural support.

Within fixed income, duration should gradually become more attractive as inflation risks continue moderating and policy rates approach their cyclical peaks. High-quality sovereign bonds may once again provide portfolio diversification following several years during which both equities and bonds declined simultaneously.

Commodity markets warrant a more selective approach. While geopolitical risks may continue generating episodic price spikes, we believe sustained structural shortages are becoming less likely as supply uncertainties gradually ease.

By contrast, we remain cautious toward broad Chinese risk assets until stronger evidence emerges that structural challenges—including weak private-sector confidence, prolonged property adjustment, and slowing productivity—are being addressed rather than temporarily offset by policy stimulus.

The defining investment opportunity of the coming year is unlikely to arise from accurately predicting the next inflation print. Instead, it will come from recognizing that global markets are quietly entering a new phase in which liquidity, productivity, and capital allocation increasingly outweigh the inflation narrative that has dominated the past several years.

Conclusion: The Cycle Is Changing Faster Than the Consensus

Investing is often less about forecasting the future with perfect precision than about recognizing when yesterday’s narrative has begun to lose explanatory power.

For nearly four years, global markets have revolved around one dominant variable: inflation. Every employment report, every CPI release, every central bank speech was interpreted through the lens of whether prices would continue climbing or finally begin to normalize.

That framework is becoming increasingly outdated.

Inflation has not disappeared, nor should investors become complacent. Geopolitical tensions remain elevated, fiscal deficits across major economies continue to expand, and energy markets will remain susceptible to unexpected disruptions. These risks warrant continued monitoring.

However, the balance of probabilities is shifting.

The evidence increasingly suggests that developed economies are moving toward a regime characterized by slower but positive growth, moderating underlying inflation, and a gradual improvement in financial conditions. Rather than entering another inflation supercycle, markets appear to be transitioning toward a period in which liquidity management, productivity gains, and capital investment once again become the dominant drivers of asset prices.

This distinction is subtle, but enormously important.

The strongest investment opportunities rarely emerge when macroeconomic uncertainty disappears. They emerge when uncertainty begins changing direction before consensus recognizes the shift.

Today’s environment bears many of those characteristics.

Manufacturing linked to artificial intelligence continues attracting unprecedented levels of investment. Corporate balance sheets, particularly in the United States, remain considerably healthier than in previous tightening cycles. Japan is quietly benefiting from structural corporate reforms while strengthening its position within global technology supply chains. Even Europe, despite its cyclical headwinds, possesses globally competitive industrial champions capable of benefiting from renewed investment spending.

At the same time, investors should remain disciplined in distinguishing between economies undergoing temporary cyclical weakness and those confronting deeper structural adjustments. Not every market will participate equally in the next phase of the global expansion, and regional dispersion is likely to remain unusually wide.

The coming investment cycle will reward selectivity rather than indiscriminate risk-taking.

Asset allocation should increasingly favor structural winners—businesses and economies positioned to benefit from digital infrastructure, automation, electrification, defense modernization, energy resilience, and productivity-enhancing technologies. These themes are supported not merely by cyclical demand but by multi-year capital expenditure programs that are reshaping the global economy.

YCC Capital Strategic View

Our central scenario remains constructive.

We expect global growth to soften modestly before reaccelerating into 2027 as energy-related uncertainty fades, financial conditions gradually improve, and private-sector investment continues expanding around artificial intelligence and next-generation infrastructure.

For investors, this is unlikely to resemble the synchronized global boom that characterized earlier recoveries. Instead, it should be viewed as a differentiated expansion in which capital increasingly flows toward economies demonstrating superior productivity, institutional stability, technological leadership, and policy credibility.

Within this framework:

- We remain cautiously optimistic on the United States, supported by resilient corporate earnings, innovation-led investment, and deep capital markets.

- We maintain a constructive medium-term outlook on Japan as corporate reform, shareholder-friendly governance, and technology exports continue strengthening the country’s long-term investment case.

- We expect Europe to recover gradually but believe returns will remain highly selective across sectors and countries.

- We remain cautious toward China’s broader macro outlook. Structural headwinds—including prolonged property-sector adjustment, demographic deterioration, local government debt burdens, and weaker private-sector confidence—are likely to constrain medium-term growth despite intermittent policy support.

Ultimately, the investment landscape is becoming less about avoiding recession and more about identifying where the next wave of global capital expenditure will be deployed.

The world’s economic center of gravity is not standing still. Capital is migrating toward innovation, productivity, energy security, and strategic infrastructure. Investors who position portfolios around these enduring themes—rather than yesterday’s inflation fears—are likely to be better positioned for the next chapter of the global market cycle.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, forecasts, and projections expressed herein represent the opinions of YCC Capital Management as of the publication date and are subject to change without notice as market conditions evolve.

Past performance is not indicative of future results. Investing in financial markets involves substantial risks, including the potential loss of principal. No investment strategy can guarantee profits or protect against losses under all market conditions.

This report has been prepared using publicly available information believed to be reliable, including economic releases, market data, corporate disclosures, and information obtained from Bloomberg and other publicly available sources. While every reasonable effort has been made to ensure accuracy, YCC Capital Management makes no representation or warranty, express or implied, regarding the completeness, accuracy, or timeliness of the information contained herein.

Forward-looking statements involve known and unknown risks and uncertainties. Actual economic developments, market performance, policy decisions, geopolitical events, and investment outcomes may differ materially from those discussed in this report.

YCC Capital Management, its affiliates, principals, employees, and related investment vehicles may hold long or short positions in securities, currencies, commodities, derivatives, or other financial instruments discussed in this publication and may effect transactions that differ from the views expressed herein.

Nothing contained in this report should be interpreted as personalized investment advice or a recommendation tailored to the investment objectives or financial circumstances of any specific investor. Readers should conduct their own independent research and consult qualified legal, tax, accounting, and financial advisors before making investment decisions.

No part of this publication may be reproduced, redistributed, or transmitted in any form for commercial purposes without the prior written permission of YCC Capital Management.

© 2026 YCC Capital Management. All rights reserved.

YCC Capital’s flagship investment vehicle, the YCC International Value Fund, LP, is a Delaware-domiciled Rule 506(c) private investment fund pursuing a concentrated global macro value strategy focused on capital-flow-driven market dislocations, asymmetric risk-reward opportunities, and long-term capital appreciation. Performance information, where referenced, has been independently verified by third-party fund administrators, including NAV Consulting, although individual investor results may vary.

Contact Us

For institutional inquiries, media requests, or investment research questions, please contact:

YCC Capital Research

Email: ir@yccinvest.com

To receive our complimentary daily macro and market intelligence, register at:

Stay informed with YCC Capital Research’s daily insights covering global macroeconomics, asset allocation, geopolitics, equity strategy, fixed income, currencies, commodities, and long-term investment themes.

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com