YCC CAPITAL

Emerging Markets & China Strategy

June 28, 2026

Executive Summary

There is a familiar temptation whenever property markets weaken: investors instinctively assume that sustainable economic recovery cannot begin until housing prices stabilize. International evidence suggests the opposite is often true.

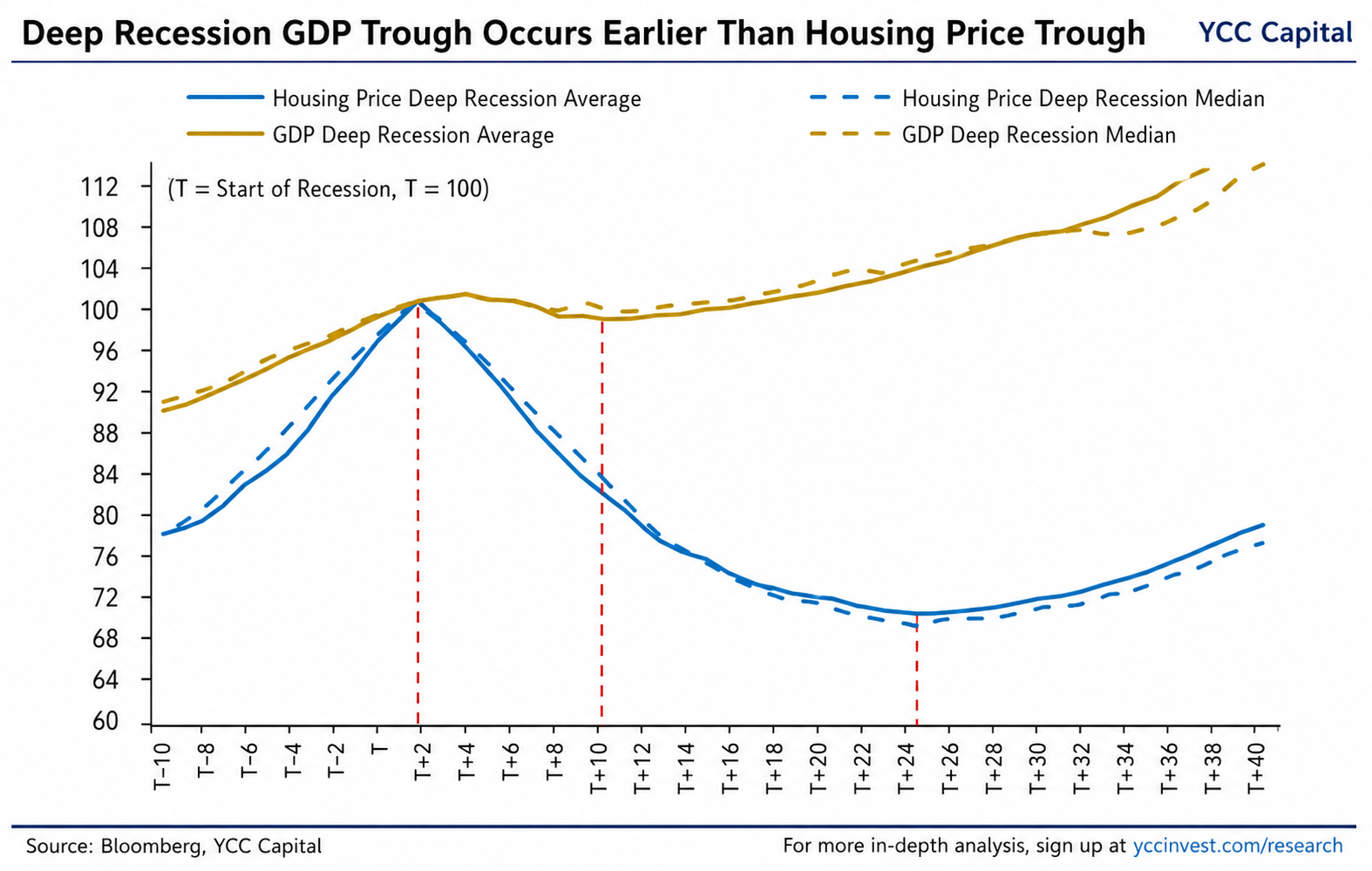

Drawing on nearly six decades of data across 57 economies and 190 housing downturns, our analysis indicates that economies frequently recover well before real estate markets do. GDP typically reaches its trough approximately two years after housing prices begin falling, while residential property prices often continue declining for another three to four years. In other words, economic expansion and property recovery become partially decoupled.

This phenomenon—which we describe as “de-real-estate growth”—marks one of the most important structural transitions modern economies undergo after a property boom ends. Growth no longer relies primarily on expanding mortgage credit, residential construction, or housing-related consumption. Instead, new drivers gradually emerge: stronger exports, resilient service-sector demand, manufacturing investment, infrastructure spending, and productivity-enhancing capital expenditure.

History repeatedly demonstrates that economies do not simply replace one growth engine with another overnight. The adjustment resembles changing engines on an aircraft already in flight. The process is uncomfortable, uneven, and politically difficult, yet entirely possible.

China today increasingly exhibits many of these characteristics. While its housing correction has not yet reached the severity observed in historical “deep contraction” episodes internationally, the composition of growth has already shifted meaningfully. Exports, manufacturing investment, infrastructure, and service consumption have become progressively larger contributors to economic activity, while the property sector’s influence continues to diminish.

This transition should not be mistaken for a return to the old investment cycle. Rather, it represents a fundamental restructuring of China’s economic model. The economy may continue expanding, but not because real estate has recovered. Instead, it is learning—perhaps reluctantly—to grow without it.

The Historical Pattern: GDP Recovers Before Housing

One of the most consistent findings across international property cycles is the surprisingly large gap between macroeconomic stabilization and housing market stabilization.

Across 48 episodes classified as severe real estate contractions, GDP generally bottoms around eight quarters after house prices begin declining. Property prices, however, do not typically reach their trough until approximately 22 quarters, or roughly five and a half years, into the downturn.

The implication is profound.

Economic recovery does not require housing prices to recover first.

Instead, fiscal stimulus, monetary easing, export competitiveness and private-sector adaptation allow broader economic activity to stabilize while real estate continues working through excess supply, leverage and balance-sheet repair.

This distinction matters enormously because investors frequently anchor their outlooks on housing indicators while overlooking improvements elsewhere in the economy. The data suggest this approach systematically underestimates the resilience of broader economic systems.

One might compare it to recovering from an injury. A patient may begin walking long before the broken bone appears fully healed on an X-ray. The visible wound lingers even as underlying functionality steadily improves.

The same principle frequently applies to national economies.

Three Stages of De-Real-Estate Growth

International experience suggests that post-property adjustments evolve through three distinct phases.

Stage One: The Initial Shock

The first two years are dominated by deteriorating housing activity.

Falling home prices suppress residential construction, reduce household wealth, weaken confidence and slow consumption. Housing investment contracts first before weakness gradually spreads through the broader economy.

During this period GDP growth typically deteriorates rapidly.

Policy responses remain relatively limited initially as authorities assess whether the slowdown represents a temporary correction or a broader structural adjustment.

Stage Two: Policy-Led Stabilization

Around the second year, the economy generally reaches its cyclical low.

Recovery begins—but it is largely policy-driven.

Governments expand fiscal deficits aggressively while central banks lower interest rates to cushion private-sector deleveraging.

Across international cases, fiscal deficits increased from an average of only 0.4% of GDP at the onset of housing weakness to nearly 5% of GDP roughly four years later.

Meanwhile policy interest rates declined dramatically, falling from approximately 11.1% to 6.3% over the same period.

This combination of easier monetary policy and expansionary fiscal support creates sufficient demand to stabilize employment and prevent deeper recessions.

Yet growth during this phase remains fragile because it depends heavily on government intervention rather than private-sector momentum.

Stage Three: Self-Sustaining Expansion

The final stage begins roughly five years into the housing downturn.

Interestingly, governments often begin reducing policy support just as economic momentum strengthens.

Fiscal deficits gradually narrow.

Interest-rate cuts slow or stop altogether.

Despite less policy assistance, GDP continues improving.

This represents the most encouraging phase because private demand increasingly replaces public stimulus. Businesses begin investing again, consumers regain confidence, exports strengthen, and the economy develops new engines of expansion independent of housing.

The transition from policy dependence to market-led growth marks the true completion of de-real-estate growth.

Why Housing Rarely Regains Its Former Dominance

One of the most misunderstood aspects of housing cycles is what happens after recovery.

Property prices may eventually stabilize.

Housing construction may partially recover.

Yet housing almost never regains its previous share of national output.

International evidence shows residential investment averaged roughly 6.7% of GDP at its historical peak before severe contractions.

Even ten years after housing prices began falling, residential investment typically recovered only to approximately 4.2% of GDP.

The pattern is remarkably persistent.

Consumer behavior follows a similar trajectory.

Durable goods consumption—closely linked to home purchases, renovations and furnishing—also recovers only partially. Even after property markets stabilize, consumers rarely resume the same level of housing-related spending seen during previous booms.

This reflects more than cyclical weakness.

It reflects structural change.

Once economies diversify toward services, technology, manufacturing and exports, they seldom return to relying primarily on residential property as their principal growth engine.

History therefore argues against expecting China to recreate the property-driven expansion model that characterized the previous two decades.

Three Engines That Replace Property

If housing no longer leads growth, what does?

International experience consistently identifies three major replacement engines.

Export Rebalancing

The first engine is external demand.

During housing booms, domestic consumption and imports typically surge, compressing net exports.

As housing weakens, imports moderate while export competitiveness gradually improves.

Across historical episodes, net exports shifted from deficits equivalent to roughly 4.7% of GDP near housing peaks to meaningful surpluses several years later.

This external adjustment becomes one of the earliest contributors to GDP recovery.

In effect, economies replace internally financed expansion with externally generated demand.

More Resilient Consumer Spending

Consumption also evolves rather than simply collapsing.

Overall household spending declines modestly.

However, not all categories behave equally.

Durable goods—furniture, appliances, automobiles and housing-related purchases—experience the largest declines.

By contrast, non-durable goods and services prove remarkably resilient.

Food, healthcare, education, travel, restaurants and personal services continue expanding because they satisfy recurring rather than investment-driven needs.

The distinction is crucial.

Consumers postpone buying another apartment.

They rarely postpone eating dinner.

Non-Property Investment

The third pillar involves investment outside residential construction.

Although housing investment often continues falling for years, total fixed investment frequently bottoms much earlier.

Lower interest rates reduce financing costs.

Businesses increasingly invest in manufacturing, logistics, technology, digital infrastructure and industrial modernization.

Returns on productive capital gradually exceed financing costs once again.

This dynamic allows manufacturing investment and infrastructure spending to offset continuing weakness in residential construction.

China’s Structural Transition

China increasingly exhibits many of these international characteristics.

The country’s housing downturn remains significant, although not yet comparable to the deepest international property collapses examined in our historical dataset.

Nevertheless, the composition of growth has clearly shifted.

Exports Become the Primary Stabilizer

Net exports have become one of China’s strongest macroeconomic supports.

Between 2021 and 2025, net exports of goods and services contributed approximately 17% of overall GDP growth—by far the strongest five-year contribution recorded over the past quarter century.

Even more important is the changing composition of exports.

China has steadily migrated away from lower-value labor-intensive manufacturing toward higher-value industrial products including electric vehicles, batteries, renewable energy equipment, semiconductors, industrial machinery and increasingly AI-related hardware.

Recent export growth in integrated circuits and automatic data-processing equipment has been particularly notable, reflecting global investment in artificial intelligence infrastructure.

That said, this strength should not be viewed as unassailable. Rising geopolitical tensions, expanding industrial policy in advanced economies, reshoring initiatives, tariff risks, and increasing trade restrictions all represent meaningful headwinds over the medium term. Export-led growth provides valuable support, but it cannot fully compensate for persistent weakness in domestic demand indefinitely.

Consumption Is Changing Rather Than Disappearing

Property once generated multiple layers of consumer demand.

Buying a home led to renovations.

Renovations created demand for furniture.

Furniture purchases supported appliance sales.

The entire consumption ecosystem revolved around residential investment.

That chain has weakened substantially.

Instead, China’s consumers increasingly allocate spending toward experiences and everyday necessities.

Restaurant spending, leisure services and non-durable consumption have demonstrated considerably greater resilience than traditional housing-linked purchases.

This represents an important structural evolution.

Consumers are spending differently—not necessarily spending less.

Manufacturing and Infrastructure Carry More Weight

Since 2022, manufacturing investment and infrastructure have become increasingly important pillars of Chinese growth.

Industrial upgrading remains a major policy priority, while public infrastructure continues receiving substantial fiscal support.

These sectors have helped offset much of the drag generated by declining residential investment.

However, important challenges remain.

Manufacturing profitability has come under increasing pressure amid excess capacity in several industries. Local government finances remain strained, limiting the long-term effectiveness of infrastructure-led stimulus. At the same time, demographic aging, slower productivity growth, and elevated private-sector caution continue to constrain domestic investment appetite.

Consequently, China’s transition toward de-real-estate growth is likely to remain uneven rather than linear.

YCC Capital Strategic View

The broader lesson extends well beyond China.

Property cycles shape economies for decades, but they rarely define their ultimate trajectory.

The countries that emerge strongest are not those that successfully reignite housing booms.

They are the ones that successfully discover new engines of productivity.

China has clearly entered that transition.

Its property sector is unlikely to reclaim the outsized role it once occupied, and investors expecting a return to the leverage-fueled expansion of the 2010s may be disappointed.

Instead, the investment landscape is shifting toward globally competitive manufacturing, advanced technology, selective export champions, service-sector resilience and productivity-enhancing capital investment.

From our perspective, this transition will likely prove slower than official expectations suggest. Structural headwinds—including demographics, local government debt, declining housing wealth and persistent private-sector confidence challenges—remain significant constraints on medium-term growth.

Nevertheless, history suggests that economies need not wait for housing to recover before broader economic stabilization begins.

The future belongs not to the economies that rebuild yesterday’s growth model, but to those willing to construct an entirely new one.

Editorial Board

Ken Cao — Chief Strategist, Global Investment Strategy

Le Gao — Managing Analyst

Yui Nabeshima — Strategist

Mai Ikeda — Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S. and structured as a Rule 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

For institutional inquiries or comments regarding this research, please contact:

Sign up for YCC Capital’s free daily market insights at www.yccinvest.com.

Sources: Bloomberg, YCC Capital. Based on analysis of international housing cycles and macroeconomic data synthesized from the uploaded research report.

For more related research:

China’s Recovery Is Losing Altitude: Exports Mask a Deepening Domestic Slowdown