YCC CAPITAL

Global Strategy

June 21, 2026

Executive Summary

Financial markets have largely celebrated the announcement of a temporary U.S.–Iran agreement, a 60-day ceasefire framework, and the gradual reopening of the Strait of Hormuz. Asset prices have responded as if a major geopolitical risk has been removed. Yet the real economy operates on a different timetable.

The central message from our analysis is straightforward: markets are pricing peace, while households, corporations, and governments are still paying the bill for war. The economic transmission of the energy shock has not yet fully passed through inflation, wages, consumption, and corporate earnings. The relief is real, but it is neither immediate nor guaranteed.

Much like a household whose utility bill arrives weeks after a heatwave has ended, economies often experience the most painful consequences of an energy shock after the headlines disappear. That lag now matters enormously for investors.

YCC Perspective

The ceasefire represents a meaningful de-escalation rather than a durable geopolitical settlement. Investors should resist the temptation to treat the reopening of Hormuz as an “all clear” signal.

The next phase of the cycle is likely to be defined less by military developments and more by three questions:

- How quickly can global energy flows normalize?

- How persistent will inflation prove to be?

- Will central banks tighten policy into weakening economies?

Those questions—not the ceasefire announcement itself—will determine asset returns over the next 12–18 months.

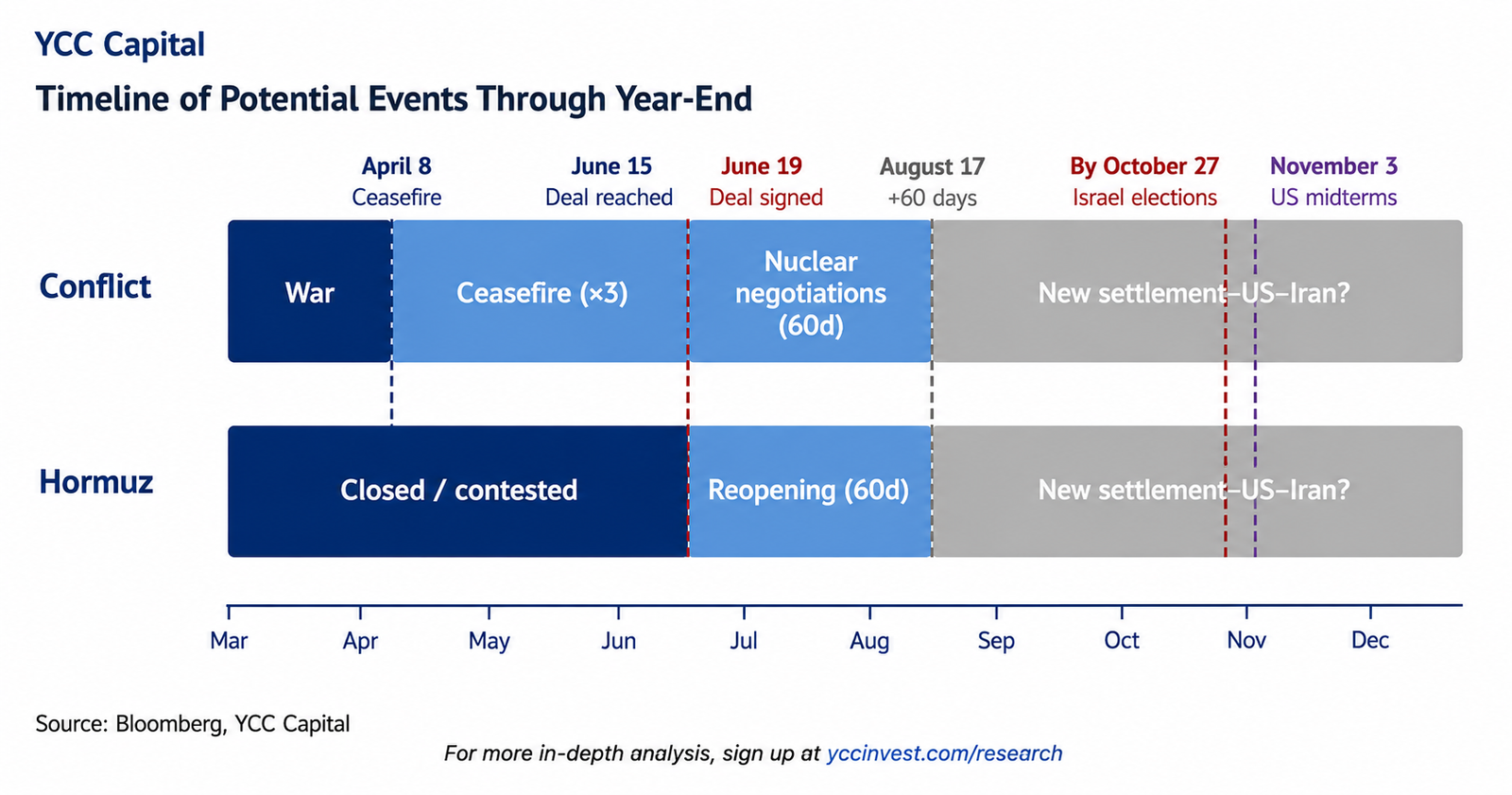

The Deal: A Framework for De-escalation, Not a Final Settlement

The U.S.–Iran understanding establishes a 60-day ceasefire period, opens a pathway toward renewed nuclear negotiations, and creates conditions for the gradual reopening of the Strait of Hormuz.

The agreement also provides Iran temporary flexibility to increase oil exports while broader sanctions discussions continue. However, permanent sanctions relief remains conditional upon progress in nuclear negotiations and compliance with broader geopolitical commitments.

This distinction is critical.

The market has interpreted the agreement as a solution. In reality, it is closer to a probation period.

The durability of the arrangement depends on:

- Successful mine-clearing operations in the Strait of Hormuz.

- Restoration of commercial shipping confidence.

- Stability in war-risk insurance pricing.

- Continued progress in nuclear negotiations.

- Maintenance of ceasefires across other regional fronts, particularly Lebanon.

History suggests that confidence recovers more slowly than physical infrastructure. Even after the Iran-Iraq War ceasefire in 1988, commercial shipping required months—not weeks—to normalize despite naval protection.

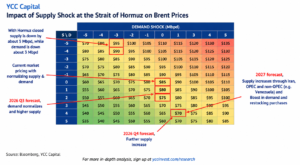

Energy Markets: Relief Arrives Slowly

The market’s first reaction has focused on oil.

That reaction is understandable but incomplete.

Our base case assumes:

- Approximately 65% of disrupted oil supply returns within three months.

- Around 80% returns within four months.

- Full normalization occurs near year-end.

Under this scenario:

| Period | Brent Oil Forecast |

|---|---|

| Q3 2026 | ~$80/bbl |

| Q4 2026 | ~$75/bbl |

| 2027 Average | ~$70/bbl |

The decline in prices reflects normalization rather than oversupply.

Additional barrels are expected from:

- Iran

- OPEC production normalization

- U.S. output

- Venezuela

- Other non-OPEC producers

At the same time, global demand is expected to recover as Asian industrial activity improves and strategic inventories are replenished.

The result is not a collapse in oil prices but rather a transition toward a more balanced market.

Inflation: The Peak Is Still Ahead

One of the most important market misconceptions today is that lower oil prices immediately mean lower inflation.

That is not how inflation transmission works.

Energy shocks move through the economy in stages:

- Energy and transport costs rise.

- Producer prices increase.

- Businesses pass costs to consumers.

- Wage negotiations adjust.

- Core inflation rises with a lag.

As a result, inflation may actually worsen before it improves.

Our expectations:

United States

- 2026 CPI: approximately 3.3%

- Core CPI exceeds 3% during Q4 2026

Eurozone

- Inflation peaks near 3.4%

- Average 2026 inflation around 3.1%

Real wage growth is unlikely to turn meaningfully positive until early 2027.

Markets are therefore discounting inflation improvement several quarters before official data will confirm it.

Central Banks Face Their Biggest Policy Risk Since 2022

The Federal Reserve and the ECB now face an uncomfortable dilemma.

By the time inflation data peaks, underlying economic momentum may already be weakening.

Yet policymakers remain heavily dependent on backward-looking indicators.

Our base case expects:

- One additional Federal Reserve rate hike.

- One additional ECB rate hike.

The risk is clear:

Central banks may tighten policy precisely as inflation pressures begin fading and growth slows.

This risk is particularly acute in Europe, where growth is already fragile.

The United States enjoys stronger structural growth drivers and therefore has greater capacity to absorb further tightening.

Europe does not.

Why Europe Remains the Most Vulnerable Region

The U.S.–Iran agreement does not affect all economies equally.

America enters this period with several advantages:

- Net energy exporter status.

- Strong AI-driven capital expenditure cycle.

- Supportive fiscal policy.

- Wealth effects from elevated equity valuations.

Europe enjoys none of these offsets.

The Eurozone remains vulnerable because:

- Energy intensity is higher.

- Trade dependence is greater.

- Consumer confidence remains weak.

- Fiscal flexibility has been largely exhausted.

Germany benefits from defense and infrastructure spending.

Elsewhere conditions remain far more challenging.

France, for example, continues to show deteriorating business sentiment and weak growth momentum.

For European households, the squeeze is likely to persist through most of 2026.

Energy bills absorb a larger share of disposable income than in the United States, while mortgage repricing remains especially painful in markets such as the United Kingdom and the Netherlands.

China: Stable Growth, Persistent Export Strength

China remains one of the more resilient major economies.

Growth continues to be driven by:

- High-tech manufacturing.

- Export competitiveness.

- AI-related hardware demand.

- Clean-energy supply chains.

Our expectations:

| Year | GDP Growth |

|---|---|

| 2026 | 4.7% |

| 2027 | 4.4% |

Inflation remains subdued:

| Year | CPI |

|---|---|

| 2026 | 1.0% |

| 2027 | 1.2% |

The People’s Bank of China therefore retains flexibility to maintain accommodative policy.

The primary risk remains trade policy, particularly potential U.S. tariff escalation.

Corporate Impact: Pricing Power Becomes Everything

Lower energy prices help businesses, but not equally.

The key dividing line is pricing power.

Likely Beneficiaries

- Airlines

- Branded pharmaceuticals

- Specialty chemicals

- Fertilizer producers

- Semiconductor companies benefiting from AI demand

More Vulnerable Industries

- Automotive OEMs

- Generic pharmaceuticals

- Consumer hardware manufacturers

- Commodity producers without pricing leverage

Transportation and petrochemical firms benefit most directly because fuel often represents 25–40% of operating costs.

Yet even here, relief is partial.

Input costs may fall, but labor expenses remain elevated through 2027.

In many sectors, margins improve more slowly than investors expect.

Capital Markets: Rotation, Not Repricing

One of the most important investment conclusions is that markets never treated the conflict as a systemic crisis.

Performance since the conflict began:

- MSCI USA: approximately +8%

- MSCI Europe: approximately +5%

- MSCI Emerging Markets: approximately +6.5%

Because markets already looked through the conflict, the upside from peace is limited.

Meanwhile:

- Valuations sit near the 85th percentile of historical ranges.

- Earnings expectations are near the 92nd percentile.

That asymmetry matters.

Good news offers modest upside.

Bad news offers substantial downside.

Our expectation is not for a broad equity re-rating but rather:

- European cyclicals outperforming.

- Transportation sectors improving.

- Energy-sensitive industries recovering.

- Continued AI leadership globally.

A 5–10% correction remains plausible if growth disappoints or inflation proves more persistent than expected.

Fixed Income Strategy

Europe

The most attractive opportunities appear in the front and intermediate portions of the European curve.

If energy prices continue declining and inflation moderates, ECB tightening expectations may prove excessive.

United States

The story is more complex.

While geopolitical risks fade, structural inflation and fiscal supply dynamics continue pressuring long-end yields.

We continue to favor inflation-linked exposure over long-duration nominal bonds.

The likely outcome is:

Curve steepening rather than a parallel rally.

Credit Markets

Credit spreads already reflect considerable optimism.

Current levels remain near historic tights:

- EUR Investment Grade: ~77bps

- U.S. Investment Grade: ~72bps

The ceasefire protects carry trades.

It does not create a compelling new compression story.

We continue to favor:

- High-quality carry opportunities.

- Selective investment-grade exposure.

- Careful underwriting in lower-rated credit.

At current spread levels, investors have little margin for error.

Private Markets

The biggest impact of de-escalation is likely to be increased activity rather than higher valuations.

Benefits include:

- Stronger exit markets.

- Easier refinancing conditions.

- Greater transaction confidence.

- Improved liquidity.

Infrastructure, logistics, energy transition assets, and data-center ecosystems remain structural winners.

The story is operational, not valuation-driven.

Strategic Conclusion

The U.S.–Iran agreement meaningfully reduces one of the most important geopolitical risks facing markets.

Yet investors should avoid confusing reduced risk with resolved risk.

The economic consequences of the energy shock are still moving through:

- Inflation

- Wages

- Consumer spending

- Corporate margins

- Central-bank decision making

Markets have largely priced in peace.

The economy has not.

As a result, the most important investment principle today is patience.

The cost of reacting too slowly to renewed geopolitical stress remains significantly larger than the cost of maintaining prudent risk management.

Editorial Board

Ken Cao – Chief Strategist, Global Investment Strategy

Le Gao – Managing Analyst

Yui Nabeshima – Strategist

Mai Ikeda – Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

Investor Relations: ir@yccinvest.com

For free daily market insights, macro research, and investment commentary, visit:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com