YCC CAPITAL

U.S. Themes & Strategy

June 21, 2026

Executive Perspective

When a major sporting event arrives, the economic narrative often follows a familiar script: packed hotels, crowded airports, booming restaurants, and a wave of new jobs. The story is intuitive and compelling. Yet history suggests reality is often more nuanced.

The 2026 FIFA World Cup, jointly hosted by the United States, Canada, and Mexico, will be the largest World Cup ever staged. With 48 teams, 104 matches, and an estimated 6.5 million spectators, it will undoubtedly create a visible surge in activity across host cities. The key question for investors, policymakers, and Federal Reserve officials is whether this surge translates into a meaningful and lasting improvement in U.S. employment.

Our analysis suggests the answer is: yes, but only modestly.

The World Cup is likely to create a measurable temporary boost to employment, particularly in hospitality, transportation, security, logistics, local government, and business services. However, historical evidence from the 1994 U.S. World Cup suggests that headline job-creation estimates are frequently overstated. The economic impact tends to be concentrated in specific regions and sectors, while substitution and crowding-out effects dilute gains elsewhere.

At YCC Capital, we view the World Cup as a useful case study in distinguishing between visible economic activity and lasting macroeconomic impact. A city can feel dramatically busier for six weeks without materially altering the trajectory of national employment growth.

Sources: Bloomberg, YCC Capital.

Based on analysis of the underlying research report.

Key Conclusions

Our Core Findings

- Recent U.S. labor-market strength reflects both cyclical economic improvement and World Cup-related temporary hiring.

- Historical evidence from the 1994 World Cup indicates employment gains were significantly smaller than promotional forecasts.

- The 2026 tournament may add approximately 72,000 jobs on a quarterly basis through GDP-related effects.

- FIFA estimates approximately 185,000 full-time-equivalent jobs will be supported in the United States.

- Actual realized employment effects are likely substantially lower than headline projections.

- The Federal Reserve will likely treat any World Cup-related labor strength as temporary noise rather than structural labor-market tightening.

Recent U.S. Labor Market Strength Has Surprised Expectations

The U.S. labor market has recently delivered a series of upside surprises, challenging the consensus view that labor demand was steadily cooling.

Several developments stand out:

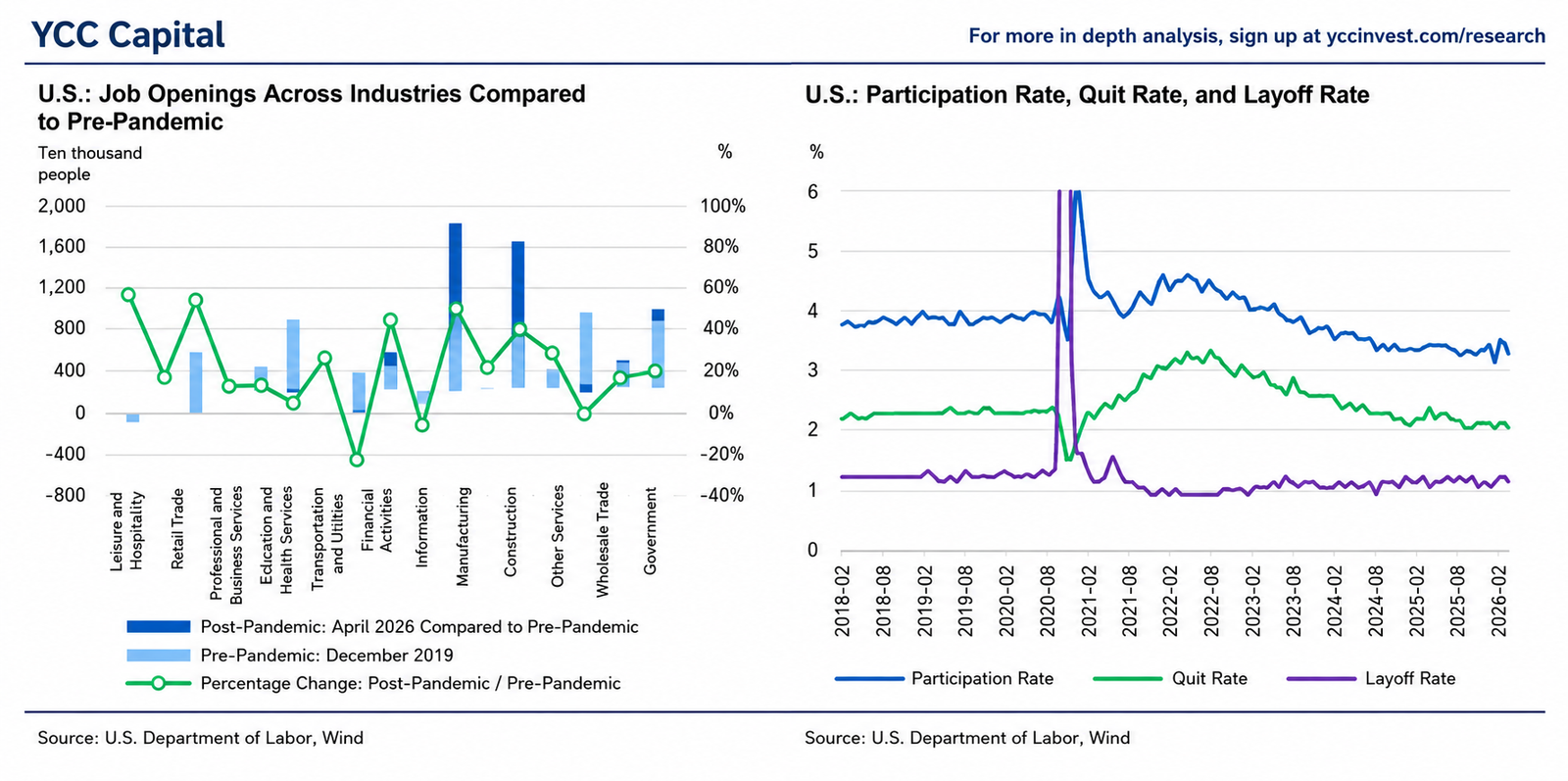

Job Openings Rebounded Sharply

April JOLTS data showed a significant increase in nonfarm job openings, rising to approximately 7.61 million positions. The job-opening rate climbed to 4.6%, significantly exceeding market expectations.

Importantly, labor demand once again exceeded labor supply after several months of relative slack.

The most notable increase occurred in Professional and Business Services, where openings surged by roughly 668,000 positions. This category often captures:

- Temporary staffing

- Event management

- Security services

- Media support

- Logistics outsourcing

These are precisely the types of positions that tend to expand ahead of mega-events such as the World Cup.

Payroll Growth Accelerated

May nonfarm payrolls increased by approximately 172,000 jobs, more than double consensus expectations. Previous months were also revised upward.

A closer examination reveals that government employment played a significant role.

Local governments added workers at a pace consistent with:

- Event preparation

- Public safety coordination

- Transportation management

- Temporary administrative staffing

Meanwhile, construction and manufacturing also contributed positively amid continued investment spending and defense-related production growth.

Unemployment Remains Stable

The unemployment rate edged down to approximately 4.3%.

At the same time:

- Labor-force participation remains historically subdued.

- Temporary unemployment declined.

- Wage growth moderated year-over-year but accelerated on a monthly basis.

These dynamics suggest labor-market resilience without signaling a broad overheating cycle.

Why the Labor Market Is Stronger Than Expected

We identify two primary drivers.

1. Temporary World Cup-Related Hiring

Evidence points toward pre-event staffing activity in:

- Local governments

- Hospitality

- Professional services

- Transportation

- Security

- Event operations

This hiring is real, but much of it is temporary.

Think of the World Cup labor surge as a temporary bridge rather than a new highway. Workers are added to support a concentrated burst of demand, but many positions disappear once the event concludes.

2. An Investment-Led Economic Expansion

The second factor is more important.

The U.S. economy continues to exhibit characteristics of an investment-driven cycle:

- AI infrastructure spending remains exceptionally strong.

- Data-center construction continues at record levels.

- Manufacturing orders have improved.

- Inventory rebuilding is underway.

- Defense-related spending remains elevated.

Unlike temporary event hiring, these trends possess the potential to sustain employment growth over a longer horizon.

Lessons from History: The 1994 World Cup

One of the most important studies on this subject is:

Baumann, Engelhardt, and Matheson (2011)

Labor Market Effects of the World Cup: A Sectoral Analysis

The paper examined employment outcomes in host cities during the 1994 FIFA World Cup in the United States and compared them with non-host cities.

The conclusions were striking.

What Researchers Expected

Before the tournament, promotional forecasts suggested that each host city could gain:

5,000–8,000 new jobs.

The economic narrative sounded familiar:

- More tourists

- More spending

- More hiring

- Stronger local growth

What Actually Happened

The statistical evidence showed that the employment impact was either insignificant or substantially smaller than advertised.

Using the authors’ preferred methodology, hosting the World Cup increased employment by only:

0.112% per month

Equivalent to roughly:

1,900 jobs per host city per month

This was dramatically below the headline projections.

The Most Surprising Result

Retail employment actually declined in some host cities.

This finding challenges conventional assumptions.

Rather than generating entirely new spending, the tournament often redirected existing spending.

A family that buys World Cup tickets may postpone other purchases.

A visitor spending heavily on hotels and restaurants may spend less on retail shopping.

Economic activity shifts rather than expands.

Why Didn’t the 1994 World Cup Create More Jobs?

The study identified three major explanations.

1. Existing Infrastructure Reduced Construction Demand

Unlike Olympic Games or large-scale infrastructure programs, the 1994 World Cup required virtually no new stadium construction.

Existing NFL and college football facilities were utilized instead.

As a result:

- Construction employment gains remained limited.

- Infrastructure multipliers were weak.

2. Substitution Effects

Local residents often redirected discretionary spending toward World Cup-related activities.

Money spent on:

- Tickets

- Merchandise

- Match-day entertainment

replaced spending that otherwise would have occurred elsewhere.

3. Crowding-Out Effects

Regular tourists frequently avoid destinations during major events because of:

- Higher prices

- Congestion

- Reduced availability

As a result, some traditional tourism demand disappears precisely when event tourism arrives.

The net gain is therefore smaller than headline visitor numbers imply.

Why 2026 Is Different

Although historical lessons matter, the 2026 tournament is considerably larger.

| Category | 1994 World Cup | 2026 World Cup |

|---|---|---|

| Teams | 24 | 48 |

| Matches | 52 | 104 |

| U.S. Matches | 52 | 78 |

| Host U.S. Cities | 9 | 11 |

| Attendance | 3.6 million | ~6.5 million expected |

The United States alone will host 78 matches, making it the primary economic beneficiary of the tournament.

Economic Impact Assessment

Consumer Spending

Research from organizing committees and economic consultants suggests:

Direct Spending

Approximately:

$5–6 billion

Including:

- Tickets

- Hotels

- Restaurants

- Transportation

- Merchandise

Total Impact Including Multipliers

Approximately:

$10–15 billion

Equivalent to roughly:

0.033%–0.050% of U.S. GDP.

Infrastructure and Event Investment

Host-city budgets suggest spending of approximately:

$2–3 billion

Covering:

- Stadium upgrades

- Transportation management

- Security operations

- Urban improvements

This adds another:

0.006%–0.009% of GDP.

GDP Impact

Combining spending and investment effects, we estimate:

GDP Contribution

Approximately:

0.039%–0.059% of annual GDP

This translates into roughly:

0.1 percentage point of annualized GDP growth in both Q2 and Q3 2026.

Employment Impact

Using an employment elasticity of approximately 0.45:

GDP-Based Estimate

Approximately:

72,000 incremental jobs on a quarterly basis.

FIFA Estimate

A FIFA-supported socioeconomic study projects:

185,000 full-time-equivalent jobs in the United States.

These positions include:

- Hotel workers

- Restaurant staff

- Stadium operations

- Security personnel

- Transportation services

- Temporary technical support

- Venue renovation crews

Our Adjustment

Using the historical relationship observed after the 1994 tournament, actual employment outcomes may be substantially lower than promotional estimates.

Applying historical scaling factors suggests:

- Roughly 4,900 jobs per city per month

- Approximately 54,000 incremental jobs per month across 11 U.S. host cities

However, confidence intervals remain extremely wide.

Investment Implications

For Investors

The World Cup should be viewed as a tactical rather than structural macroeconomic catalyst.

Potential beneficiaries include:

- Hotels

- Restaurants

- Airlines

- Ride-sharing services

- Event staffing firms

- Security providers

- Selected regional real estate assets

However, investors should avoid extrapolating temporary demand spikes into long-term earnings assumptions.

For the Federal Reserve

The Fed is likely to recognize that:

- Event-driven employment gains are temporary.

- Labor-market tightness may be overstated during June and July.

- Post-event normalization is probable.

Consequently, World Cup hiring alone is unlikely to materially alter the policy trajectory.

YCC Capital Strategic View

Major sporting events are often described as economic engines. In reality, they are closer to economic magnifying glasses.

They concentrate spending, attention, and activity into a short period, making growth highly visible. Yet visibility should not be confused with permanence.

The 2026 World Cup will undoubtedly create jobs, stimulate spending, and generate memorable moments across the United States. A bartender in Miami, a hotel manager in Dallas, and a rideshare driver in Los Angeles will likely feel the impact directly. But at the national level, the event remains too small relative to a $30 trillion economy to fundamentally alter the direction of U.S. growth.

For markets, the more important story remains the investment cycle driven by artificial intelligence, infrastructure spending, and capital expenditure growth. The World Cup may add a temporary tailwind, but it is unlikely to become the primary engine of the U.S. labor market.

Sources: Bloomberg, YCC Capital.

Editorial Board

Ken Cao

Chief Strategist, Global Investment Strategy

Le Gao

Managing Analyst

Yui Nabeshima

Strategist

Mai Ikeda

Research Analyst

IMPORTANT DISCLAIMER

“This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report is intended solely for the use of the intended recipient(s) and may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.”

Contact Us

YCC Capital Research

Email: ir@yccinvest.com

Sign up for free daily market insights and macro research updates at:

YCC Capital Research | Sign up for free daily market insight at www.yccinvest.com