Why the Bank of Japan’s “hike plus pause on QT” is less a hawkish thunderbolt than

a careful step on a very narrow bridge

Report Date: June 16, 2026 | Source: Bloomberg, YCC Capital

YCC Capital Perspective: Japan has crossed a psychological line. A 1.0% policy rate still looks modest by U.S. or European standards, but for Japan it is the end of an era. For a generation, households, banks, insurers, exporters, and global macro investors learned to treat yen funding as financial oxygen: almost free, always available, and rarely questioned. The Bank of Japan is now trying to normalize that oxygen supply without suffocating the patient. That is the central tension of this cycle.

EXECUTIVE SUMMARY

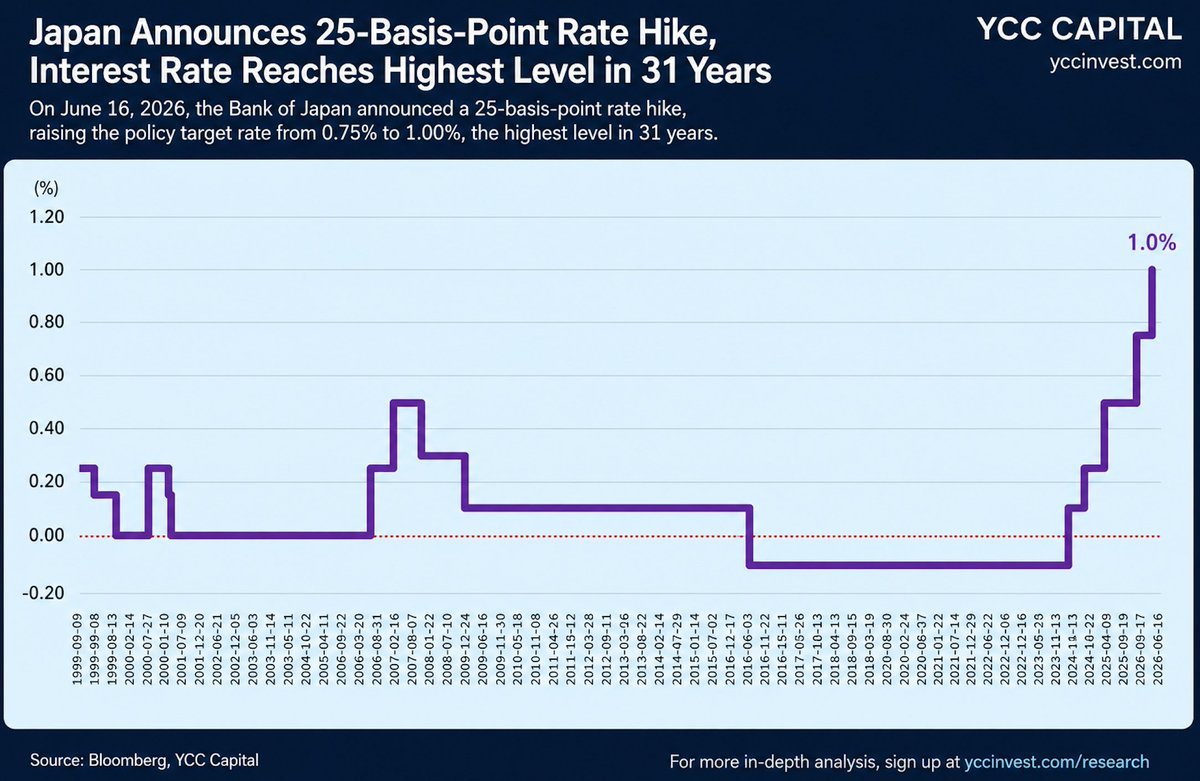

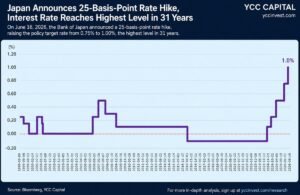

- The Bank of Japan raised its policy target rate by 25 basis points to 1.0%, the highest level in roughly 31 years. Yet the simultaneous decision to slow, and eventually pause, the reduction of JGB purchases softened the tightening message.

- This was a “rate hike with shock absorbers.” The BOJ tightened the price of money but reassured the bond market that it would not abruptly remove the liquidity backstop.

- The immediate drivers were imported inflation, energy vulnerability, and yen weakness. Japan remains heavily exposed to Middle East crude flows, while a weak yen magnifies the domestic cost of imported fuel, food, and raw materials.

- The market reaction shows the ambiguity. The yen remained under pressure while equities rallied, suggesting investors read the BOJ’s move as normalization without a full liquidity withdrawal.

- The strategic risk lies in the policy contradiction: fiscal expansion meets monetary tightening. Higher rates increase debt-service pressure just as the government leans on stimulus and defense spending.

The Policy Decision: A Hike That Came Wrapped in Cushioning

After a two-day policy meeting on June 15-16, 2026, the Bank of Japan announced that it would raise its policy target rate from 0.75% to 1.0%. At the same time, it signaled that the reduction in Japanese government bond purchases would not continue indefinitely at the same pace. From June 2026 through the January-March 2027 quarter, monthly JGB purchases are scheduled to decline by roughly JPY 200 billion per calendar quarter. From April 2027, the BOJ plans to pause further reductions and stabilize monthly JGB purchases at around JPY 2 trillion.

That combination matters. A pure rate hike says: “conditions are too hot.” A rate hike paired with a pledge to preserve bond-market flexibility says: “conditions are too hot, but the plumbing is fragile.” In practical market language, this was not a Volcker-style hammer. It was a surgeon’s scalpel used while the patient is still moving.

The BOJ also retained the option to respond flexibly if long-term yields rise too quickly. That includes increasing JGB purchases beyond the scheduled plan, conducting fixed-rate purchase operations, and providing funds against pooled collateral. The message to the market was therefore deliberately mixed: policy normalization is proceeding, but the central bank will not allow the bond market to seize up if term yields jump too far, too fast.

Figure 1. Japan policy target rate reaches 1.0%. Source: Bloomberg, YCC Capital.

The Normalization Path Since 2024

Japan’s monetary normalization has unfolded gradually. In 2024, the BOJ raised rates twice, lifting the policy target from the zero-rate zone to 0.25%. In January 2025, it raised rates by another 25 basis points to 0.50%, the largest single increase since 2007. In December 2025, it raised rates again to 0.75%, the highest level since 1995. The June 2026 hike to 1.0% brings the policy rate back to a level not seen for roughly three decades.

This is why the headline looks small but the regime change is large. A one-percentage-point policy rate is ordinary in many countries. In Japan, it is like hearing a quiet house suddenly creak at night: the sound itself is modest, but it tells you the structure is moving.

Why the BOJ Moved: Imported Inflation Meets a Weak Currency

The direct catalyst for the rate hike was the combination of rising imported inflation and renewed energy-price pressure linked to Middle East geopolitical tension. Japan is one of the world’s most energy-import-dependent major economies. As of February 2026, Japan’s dependence on Middle East crude imports exceeded 94%, and imports from Saudi Arabia, the United Arab Emirates, Kuwait, and Qatar alone accounted for more than 90% of total crude oil imports. More than 90% of Japan’s Middle East crude shipments pass through the Strait of Hormuz, leaving the energy supply chain exposed to regional conflict and maritime disruption.

The report’s underlying logic is simple: Japan imports energy, Japan imports inflation, and a weaker yen multiplies both. When oil prices rise in dollars and the yen weakens at the same time, Japanese consumers experience a double hit. It is the macro version of buying the same daily convenience-store coffee and suddenly noticing that the price tag has quietly jumped. The CPI debate becomes real when it shows up in routine purchases.

Following the outbreak of U.S.-Israel conflict with Iran, shipping through the Strait of Hormuz was effectively disrupted, with many Japan-related vessels stuck inside the Persian Gulf. Although the Japanese government announced an emergency energy diversification strategy and stated that July crude imports would fully avoid the Strait of Hormuz, near-term supply gaps and higher transport costs had already delivered a sharp shock to prices.

Producer-price pressure confirms the transmission. Japan’s PPI rose 5.3% year over year in April 2026 and 6.3% in May 2026, the largest increase since March 2023. The rise in raw-material and energy costs has begun to move from corporate transaction prices into broader consumer-price categories.

The recent pullback in oil prices after tentative ceasefire arrangements does not remove the macro risk. The agreement is still politically fragile, navigation through the Strait of Hormuz may require a 30- to 45-day observation period before normal operations are fully restored, and core issues such as sanctions, maritime management, and regional military posture remain unresolved. In YCC’s view, oil’s short-term decline is relief, not resolution.

The Yen Is the Other Pressure Point

The yen’s persistent weakness is another major reason the BOJ tightened. Since the start of 2026, the yen has remained under pressure. Dollar-yen broke through the 160 level at the end of April, prompting Japan’s Ministry of Finance and the BOJ to spend approximately JPY 11.73 trillion from April 30 through the end of May buying yen in the foreign-exchange market, the largest monthly intervention on record. Yet the effect was limited. The yen briefly rebounded, only for dollar-yen to move back above 160 on June 5.

The root problem is the interest-rate gap between Japan and the United States. As expectations for higher rates abroad strengthened – helped by the European Central Bank’s earlier tightening and stronger-than-expected U.S. nonfarm payrolls – the yen remained under external pressure. For the BOJ, the choice is uncomfortable: raise rates and risk damaging the bond market, or stay patient and risk importing more inflation through the currency channel.

Market Reaction: Yen Pressure, Equity Strength, and the Meaning of “Not Hawkish Enough”

The market reaction captured the ambiguity of the policy mix. After the announcement, dollar-yen moved higher intraday and approached the 160 level that many investors view as a psychological intervention line for Japanese authorities. The yen failed to reverse its weak trend. In equities, the picture was different. Because the 25-basis-point hike was already expected, the removal of uncertainty helped the Nikkei 225 rally, with the index breaking through the 70,000 mark intraday for the first time.

This divergence is important. Currency markets wanted a stronger hawkish signal. Equity markets saw a normalization narrative plus continued liquidity support. The yen heard “rates are still not high enough.” Stocks heard “Japan is no longer in deflation, but the BOJ will not pull the liquidity rug overnight.” Both interpretations can be true at the same time.

This is why the policy package partially offset the tightening effect of the rate hike. The BOJ raised the policy rate, but by announcing a future pause in purchase reductions and promising flexibility if long-term rates spike, it reassured markets that bond-market stability remains a central priority.

Market Channel | Immediate Interpretation | Strategic Implication |

Yen | Still under pressure as the BOJ did not deliver an unmistakably hawkish shock. | Currency weakness keeps imported inflation risk alive. |

Equities | Relief rally as rate hike was priced in and liquidity backstop remains visible. | Japan normalization can support nominal earnings, but valuation risk rises if yields climb. |

JGBs | Short-end repricing contained; long-end supply pressure remains. | Debt sustainability and term-premium risk become more central. |

Global Carry | No immediate forced unwind, but funding costs are rising. | A faster yen reversal could stress leveraged global positions. |

Table 1. Cross-asset interpretation of the BOJ policy mix. Source: Bloomberg, YCC Capital.

The Medium-Term Challenge: Japan’s Narrow Bridge

The BOJ’s medium-term challenge is enormous because it must manage three tensions at once. First, the government’s fiscal expansion conflicts with monetary tightening. Prime Minister Sanae Takaichi’s administration continues to treat fiscal stimulus as a central tool for supporting domestic demand and economic recovery, approving the largest economic package since the pandemic, valued at JPY 21.3 trillion. The package includes subsidies to reduce household electricity, gas, and fuel-tax burdens; targeted support for firms affected by U.S. tariff pressure; and expanded defense spending designed to accelerate the goal of lifting defense outlays toward 2% of GDP.

Second, yen weakness intensifies imported inflation and squeezes consumers. A weak currency makes the policy debate less academic. It turns central-bank language into grocery bills, utility bills, and commuting costs. Once households begin to expect prices to keep rising, the BOJ cannot rely only on patience.

Third, faster BOJ tightening could trigger a carry-trade unwind. For decades, the yen has served as one of the world’s most important funding currencies. If the U.S.-Japan rate gap narrows faster than expected, leveraged investors may rush to close yen shorts, creating a sharp currency rally, asset-price volatility, and potentially a renewed deflationary impulse. Japan is trying to leave emergency policy, but the exit door is crowded.

The Fiscal-Monetary Paradox: Loose Fiscal Policy, Tighter Money

The government’s fiscal expansion and the BOJ’s rate hikes create a classic policy paradox: loose fiscal policy plus tighter monetary policy. Fiscal expansion supports demand and may dilute the demand-cooling effect of higher rates. At the same time, increased government bond supply can lift term premiums, making it harder for the BOJ to control long-term yields without returning to heavier intervention.

Japan’s debt metrics make the trade-off more serious. The fiscal deficit is expected to widen to around 2.0% in 2026, while government debt may rise toward 240% of GDP, among the highest in the world. Higher policy rates directly increase the interest-payment burden. Japanese government interest expense reached JPY 2.5 trillion in 2025, the highest since 2022, and is likely to increase further as policy rates rise.

Investor concern over debt sustainability has already shown up in the long end of the JGB curve. In January 2026, Takaichi’s pledge to suspend Japan’s 8% food consumption tax ahead of the lower-house election heightened concerns about unfunded fiscal expansion and future bond issuance. The 40-year JGB yield broke above 4% for the first time since 1995, while the 30-year yield surged to a record 3.85%.

Because the June rate hike was largely priced in, the immediate bond-market shock was contained. The 10-year JGB yield rose only about 5 basis points to 2.625% after the decision. But pausing the reduction of purchases does not eliminate the long-term supply problem. The government issues nearly JPY 30 trillion of long-term bonds each year. As central-bank holdings gradually decline, the market must absorb more ultra-long-duration paper.

The 30-year JGB yield’s move toward 3.815% illustrates the pressure. Long-duration bonds are not just lines on a screen; they sit inside bank balance sheets, insurer portfolios, pension strategies, and global relative-value books. If yields keep climbing, valuation losses can spread from the bond market into the financial system.

Carry-Trade Risk: The Risk That Was Delayed, Not Defeated

The BOJ did not deliver a forceful enough hawkish signal to flush out speculative yen shorts. Speculative short-yen contracts remained around 115,000, the highest level in nearly nine years. This means the carry trade has not been forced into a major unwind. The risk has been postponed, not removed.

From a global asset-allocation perspective, that distinction matters. Japan has been the low-cost funding basement of global markets. When the basement rent rises, every levered strategy upstairs has to recalculate. A disorderly yen rally could tighten global financial conditions, pressure risk assets, and trigger capital repatriation into Japan. In calm markets, this process is gradual. In stressed markets, it can feel like someone pulled the emergency brake on a moving train.

YCC Strategic View: Normalization Is Positive, but the Price of Fragility Is Rising

YCC Capital views Japan’s normalization as structurally important and broadly positive over the long run. A country that spent two decades fighting deflation is finally operating in a world where nominal growth, wage dynamics, and corporate pricing power matter again. This can support Japanese equities, especially companies with domestic pricing power, global revenue exposure, and disciplined capital returns.

But the path will not be linear. Japan is normalizing from an abnormal starting point: a huge public-debt stock, an aging demographic base, a banking system accustomed to ultra-low rates, and a global investor community that has used the yen as cheap funding. The BOJ cannot simply import the Federal Reserve’s playbook. Japan’s policy machine is more like a suspension bridge than a highway: it can carry enormous weight, but sudden movements matter.

For investors, the strategic implications are clear:

- Japanese equities remain attractive selectively, but the market will increasingly differentiate between firms that benefit from reflation and firms hurt by rising discount rates.

- The yen is no longer a one-way funding currency. Weakness can persist, but intervention risk and carry-unwind risk are now structurally higher.

- Long-duration JGB risk deserves more attention. The key variable is not just the policy rate; it is the market’s willingness to absorb ultra-long supply without demanding a much higher term premium.

- Imported inflation remains the swing factor. Energy disruptions, the yen, and oil-price volatility will shape the BOJ’s reaction function more than domestic demand alone.

- Global investors should watch Japan as a source of volatility, not just an opportunity. A country that once exported cheap money may now export repricing shocks.

The June 2026 decision should therefore be read as a regime marker, not a destination. The BOJ has stepped away from crisis-era policy, but it is still walking across a bridge built during that era. The next stage of Japan’s market story will be determined by whether normalization can proceed without cracking the bond market foundation beneath it.

Editorial Board

Ken Cao | Chief Strategist, Global Investment Strategy |

Akiko Ikezawa | Managing Analyst |

Yui Nabeshima | Strategist |

Mai Ikeda | Research Analyst |

IMPORTANT DISCLAIMER

This research report is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities, financial instruments, or investment products. It is not intended as investment, legal, accounting, or tax advice and should not be relied upon as such. The views, opinions, and projections expressed herein are those of YCC Capital Management and its research personnel as of the date of publication and are subject to change without notice. Past performance is not indicative of future results.

YCC Capital Management, its affiliates, principals, and employees may hold long or short positions in securities or instruments discussed in this report and may trade for their own accounts or for client accounts in a manner inconsistent with the recommendations herein. This report is based on publicly available information and data believed to be reliable, but YCC Capital makes no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of such information. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected.

Recipients of this report should conduct their own independent due diligence and consult with their own financial, legal, and tax advisors before making any investment decisions. YCC Capital accepts no liability for any loss or damage arising from the use of or reliance on this report or its contents.

This report may not be reproduced or redistributed for commercial purposes without the prior written consent of YCC Capital. © 2026 YCC Capital. All rights reserved. YCC Capital’s flagship vehicle, the YCC International Value Fund, LP, maintains a concentrated global macro value strategy with a focus on capital-flow-driven mispricings and asymmetric hedging opportunities. The Fund is registered in the State of Delaware, U.S. and structured as a 506(c) fund. Performance data, where referenced, has been verified by independent third parties including NAV Consulting; however, individual investor results may vary.

Contact Us

For inquiries, contact ir@yccinvest.com. Sign up for the free daily newsletter at yccinvest.com for regular market insight from YCC Capital Research.